By: Russ Kamp, Managing Director, Ryan ALM, Inc.

The recent banking “crisis” has once again highlighted the willingness on the part of fixed-income “investors” to buy and hold bonds that are losing value to inflation every day. It makes little sense. During my tenure in asset consulting roles (about 20 years), we always talked about US core fixed income as having a roughly 2% inflation premium return whereas cash would command about a 1% inflation premium. But, in fact, the real return premium has averaged just over 3% per year since 1960. Those days seem long gone! Why the change in the investor’s mindset and approach? Why the willingness to use one’s resources in such a fashion? The Fed certainly has been guiding the investment community that rates would rise and rise they did, as we’ve witnessed nine consecutive FOMC meetings in which rates have been increased. Furthermore, they have indicated that there will be no cut in 2023. Yet, the Treasury yield curve has collapsed relative to where rates were just two weeks ago.

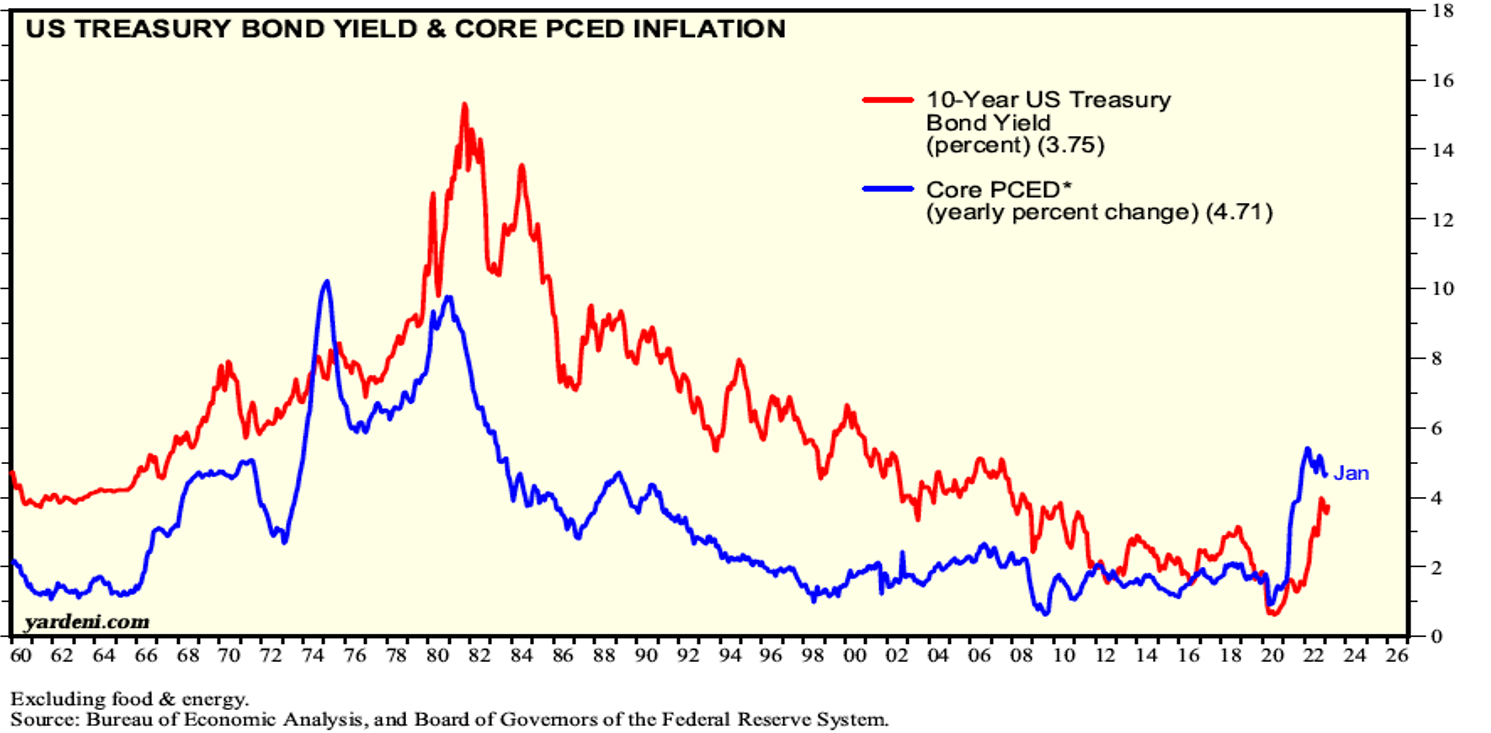

As the chart above highlights, we are in an extremely rare environment when it comes to fixed-income investing. One has to go way, way back to the mid-’70s when we last witnessed a sustained period of negative real rates. I was in high school at that time, and I suspect that many of our investors today weren’t even born – ouch! As you may recall from reading market history, there seemed to be an expectation that the Fed had accomplished its objectives by the mid-’70s (sound familiar), and as a result, bond investors were willing to jump into the market with both feet anticipating that inflation would soon fall. Well, that didn’t happen as we know, and the Fed had to keep raising US interest rates. They didn’t stop for a long time, eventually elevating the Fed Funds Rate to 20%!!

We are still in an inflationary environment with both the CPI and PCED well above the Fed’s desired level of 2%. Services inflation has remained sticky. Employment has remained firm. Despite some of our large tech companies announcing significant layoffs, initial unemployment claims remain below pre-covid-19 levels. This all seems to support the idea that the Fed must raise rates higher for longer, yet as previously stated, the Treasury yield curve has dramatically adjusted.

Do we have a banking crisis that will lead to a recession that will help the Fed achieve its objectives – the market certainly thinks so – or will the liquidity crisis be contained and banks will once again resume normal activity? We, at Ryan ALM, have been stating for 18 months that we thought that inflation would be more challenging to control as it wasn’t transitory. As a result, we’ve been writing a lot about not fighting the Fed and the upward trajectory of rates. We still believe that inflation is sticky. A premature easing of financial conditions may not result in a ’70’s-early ’80s shock, but it could nonetheless create a painful environment for both bond and equity investments.

I’ve mentioned on several occasions that most investment practitioners had never witnessed high inflation, high rates, and the onerous impact of both. A nearly 40-year bull market for bonds will do that to you. The Fed has an incredibly difficult task remaining. Fighting inflation and providing necessary liquidity for the banking system seem like incompatible objectives. Which one will they choose as their Alamo?