By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Ron Ryan and I have been saying for a while that we believed that the likely next move in US interest rates was up. We are NOT in the habit of forecasting rates, but after a 39-year bull market for bonds that produced historically low absolute and real interest rates, we felt pretty comfortable in our expectation. We’ve also been saying whenever given the chance that an upward trajectory in US rates would be BAD for total return-oriented fixed income portfolios. We’ve highlighted the fact that given the low rates, it wouldn’t take much of an upward movement in rates (roughly 30 bps) to produce a negative annual return for a 7-year duration portfolio. OUCH!

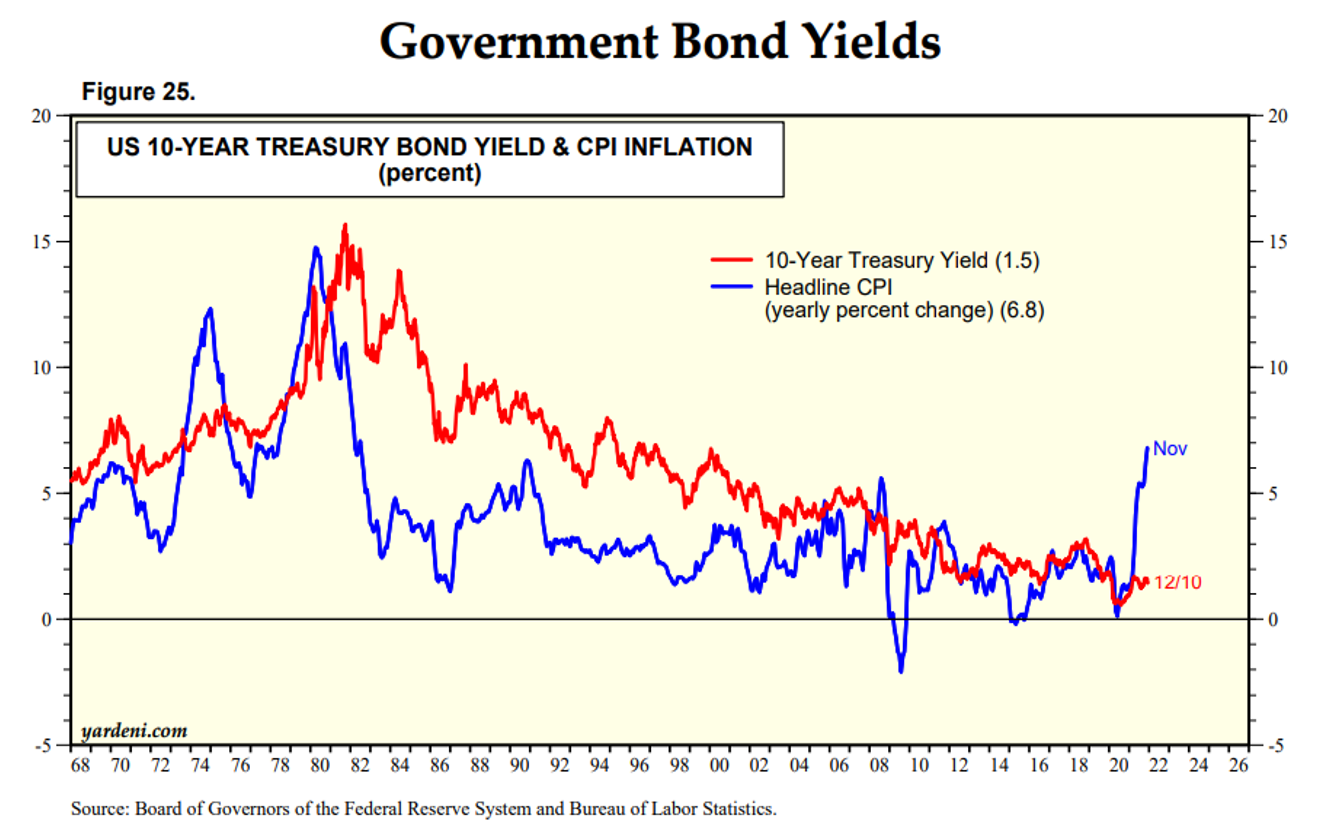

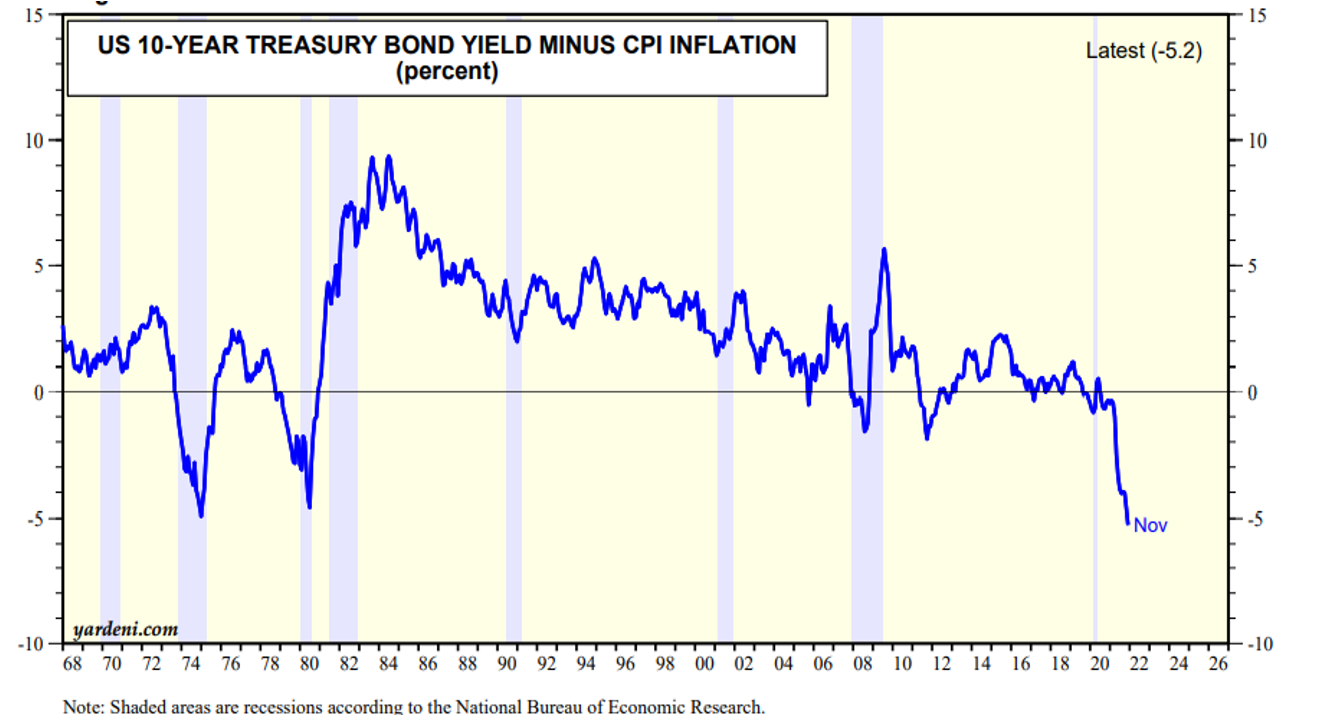

The chart above has become one of my favorites to discuss. After a 30-year bear market in US rates that ended basically as I got into the business (October 1981), we’ve enjoyed and benefited tremendously (as have equity markets) this unprecedented move down in rates. Is the party over? Given the current inflationary environment and the expectations that this is not as transitory as first contemplated, we believe that a return focused bond portfolio is going to weigh heavily on the performance of pension plans. Given this reality, we are recommending that bonds be used exclusively for their cash flows, as they are the only asset class with a known future value and consistent income generation. Don’t take interest rate risk with bonds. Match bond cash flows with liability cash flows (benefits and expenses). By doing so, you are ensuring that the assets and liabilities move in lock-step with each other and you eliminate interest rate risk since future values will be defeased. It is a phenomenal strategy.

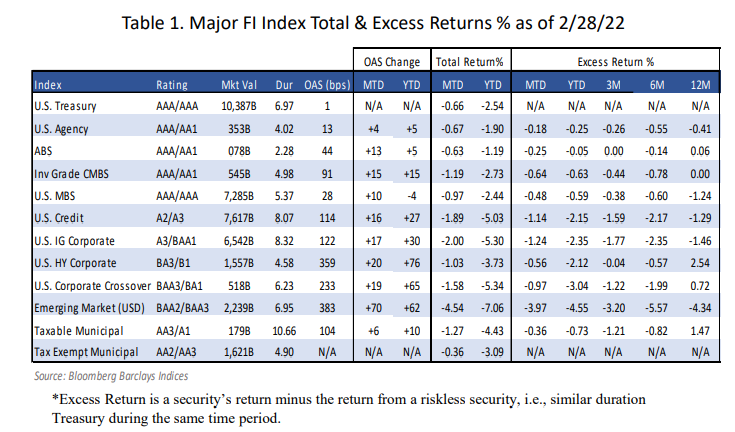

I know that we sound like a broken record. If you don’t believe us, I highly recommend that you listen to the US Federal Reserve, as they came out very aggressively yesterday and indicated that the 25 basis point move in the Fed Funds rate (first increase since 2018) would be followed by 25 bps increases at each of the remaining six meeting in 2022. Only three months ago, no FOMC member thought that rates could go beyond 2.25% by the end of next year. Now, almost all of them think that rates will go at least that far, and a couple believe rates will go as high as 3.75%. An interest rate at that level will certainly impact markets – bonds, equities, and real estate.

Is your portfolio structured to withstand this aggressive move upward in rates? What have you done to secure the promised benefits? If nothing has been done, are you prepared for deterioration in the plan’s funded status and increased contribution expenses? This is the reality that our pension industry is facing. We have solutions. Let’s talk.