By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Members of the PBGC have their work cut out for them, as last week was particularly robust in terms of new applications for Special Financial Assistance (SFA) under ARPA. There were nine applications submitted last week, with six of those being initial applications (all Priority Group 1 or 2 members), two were supplemental applications, and the ninth was a revised supplemental submission.

The plans filing applications included the United Furniture Workers Pension Fund A, Plasterers Local 82 Pension Fund, Bakery Drivers Local 550 and Industry Pension Fund, Retirement Benefit Plan of GCIU Detroit Newspaper Union 13N with Detroit Area Newspaper Publishers, Ironworkers Local Union No. 16 Pension Plan, Graphic Communications Union Local 2-C Retirement Benefit Plan, Plasterers and Cement Masons Local No. 94 Pension Fund, Alaska Ironworkers Pension Plan, and the Local Union No. 466 Painters, Decorators and Paperhangers Pension Plan. The supplemental filings are in italics, while the plan submitting a revised supplemental application is highlighted in bold. The total amount of SFA sought is $518 million. The PBGC has 120 days to act on these submissions.

There was only one plan, Local Union No. 466 Painters, Decorators and Paperhangers Pension Plan, that withdrew an application (9/28), but they quickly resubmitted a revised application on 9/30/22. There were no applications approved or denied during the last week. With regard to plans being denied SFA under ARPA, there haven’t been any to date since applications were first filed in July 2021.

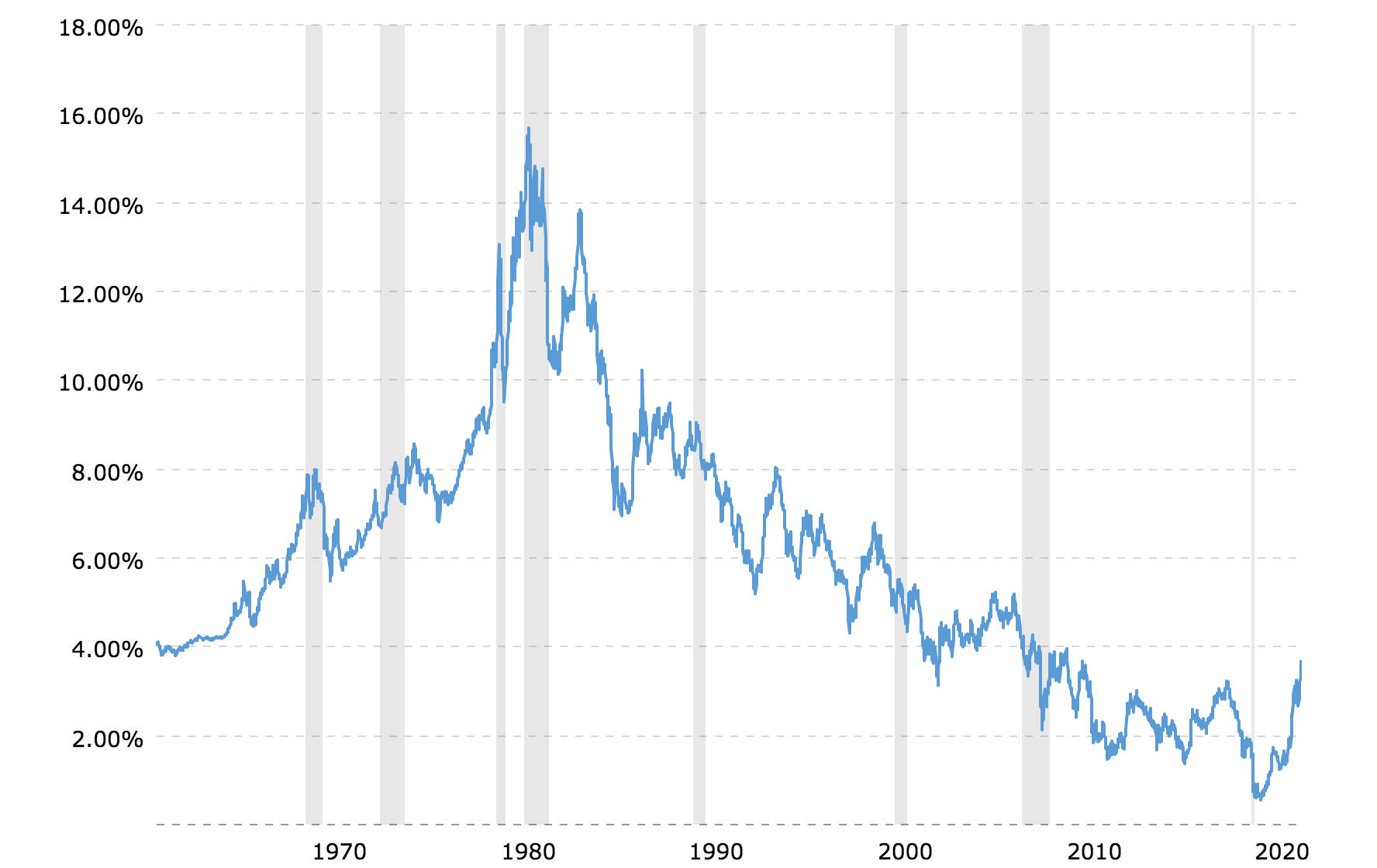

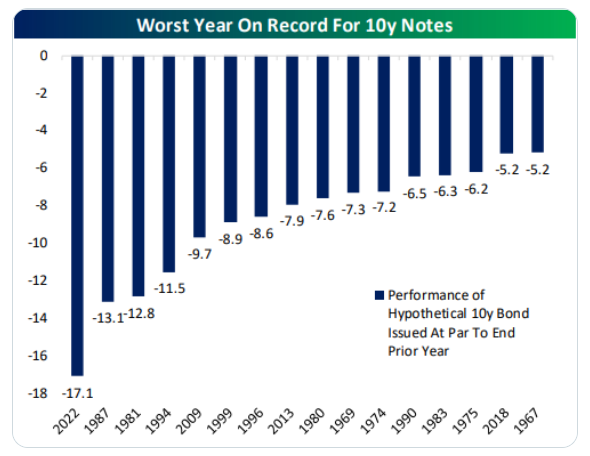

I remain concerned that there is a misunderstanding regarding the term return-seeking assets (RSA) for investments within the SFA bucket. As I’ve stated before, investments in investment grade (IG) bonds are return-seeking if they are not used to cash flow match (defease) the pension plans Retired Lives Liability chronologically from the first month’s payment as far out as the allocation lasts. Given the uncertainty in the bond markets because of high inflation, rising rates, and the Fed’s commitment to higher for longer, this misunderstanding could be quite costly. I’ve reached out once again to the PBGC encouraging them to provide clarification.

We are supportive of the PBGC’s desire to minimize exposure to RSA (33% of the SFA), but given its current interpretation of IG bonds, we remain quite concerned. Generic bond indexes are producing significant negative year-to-date returns. The SFA bucket is a sinking fund and the sequencing of returns is critical to the success of this program. Witness steep drawdowns in the initial years and the SFA could be substantially and negatively impacted. As a reminder, the goal of the legislation is to FUND the promised benefits as far out into the future as possible. Putting all of the SFA into risky strategies does nothing to secure those promises. I’ll keep you informed as to whether or not I hear back from the PBGC.