By: Russ Kamp, Managing Director, Ryan ALM, Inc.

For multiemployer plans that have filed applications with the PBGC to receive Special Financial Assistance (SFA) through the ARPA legislation, investing that grant money comes with restrictions. Effective with the release of the Final Final Rules (7/6/22), the PBGC “allows plans to invest up to 33% of their SFA funds in return-seeking investments (e.g., publicly traded common stock and equity funds that invest primarily in public shares); with the remaining 67% restricted to high-quality fixed income investments.” Based on this language from the PBGC’s website one would assume that high-quality fixed income isn’t “return-seeking”. But if the bonds aren’t used to defease pension liabilities these financial instruments are absolutely return seeking!

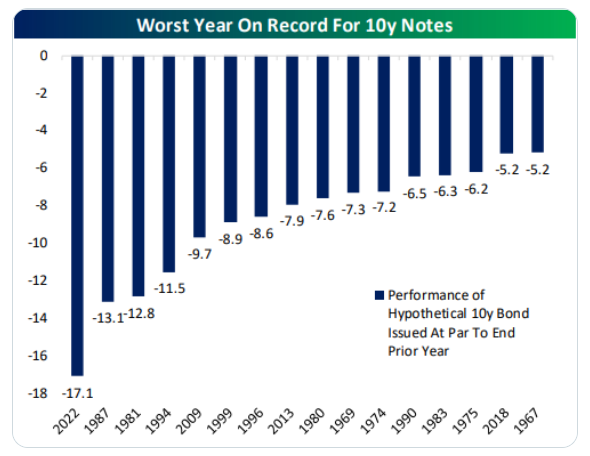

As the chart above reflects, 2022 is shaping up to be the worst year on record for the US 10-year Treasury Note and we aren’t even through the third quarter with the Federal Reserve likely providing more rate hikes before this calendar year concludes. Plan sponsors that received the SFA early in 2022 were forced to invest 100% of the proceeds in investment grade (IG) bonds. If they elected to seek exposure that would mirror a generic index such as the Bloomberg Barclays Aggregate Index, those funds have lost more than 12% YTD. For those plans that invested in fixed income and then diversified into equities following the PBGC’s release of the FFR, those equity assets have also been hit by a significant market correction that has erased all of the gains achieved from mid-June to early August. It has been a lose-lose proposition!

Regrettably, this market action has diminished the value of the SFA separate account. It didn’t have to be that way. This incredible grant (SFA) to struggling multiemployer plans should have been used to defease (SECURE) the promised benefits just as the legislation desired. Matching the bonds’ cash flows (principal and interest) with liability cash flows (benefits payments) would have protected your SFA from the significantly negative impact of rising interest rates because it is cash flow matching future values (benefit payments) which are not interest rate sensitive. Bonds are absolutely return-seeking instruments when not used to defease pension liabilities. The PBGC may have thought that they restricted the SFA bucket to having no more than 33% in RSA, but they made a terrible mistake when they didn’t instruct the plan sponsor community and their consultants to defease liabilities with the remaining 67% of the SFA bucket. As it is, 100% of the SFA can now be in RSA.

There is good news, we at Ryan ALM are aware that a couple of plan sponsors (and their consultants/actuaries) have used the fixed income exposure within the SFA to defease pension promises. In one case, 100% of the SFA is being used, and in the other, the strategy is to use 67% of the SFA to defease pension liabilities through a cash flow matching strategy. Great job!

We believe that the Federal Reserve will continue to raise the Fed Funds Rate until real interest rates are achieved. It is only at that point that inflation will be tamed. Given that the 10-year Treasury Note is currently providing a negative -4.6% real yield, we likely will witness more pain for both fixed income and equity markets. Don’t use the SFA assets in pursuit of some growth strategy. Use the SFA assets to secure as many years of benefit payments as possible as the ARPA legislation clearly states as the purpose of the grant. Use the plan’s legacy assets to pursue a growth strategy. Bifurcating your asset allocation into liquidity (SFA bucket) and growth (legacy portfolio) will provide a great structure for these challenging times.