By: Russ Kamp, Managing Director, Ryan ALM, Inc.

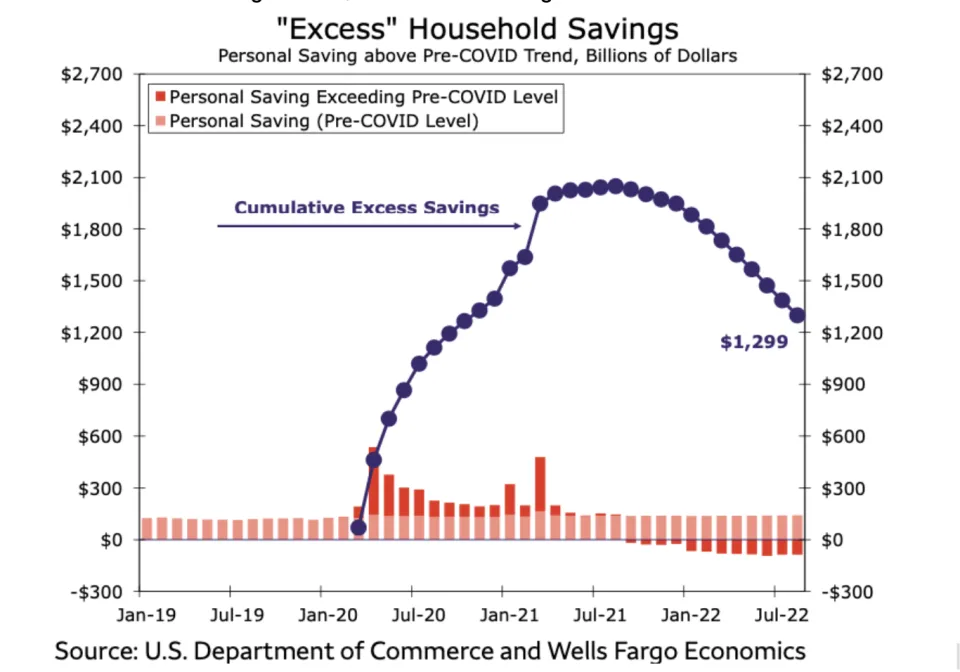

Despite the recent equity and bond market rally, we believe that the Fed still has its work cut out for them. We published a post last week titled, The Fed’s Headwind? in which I wrote about strong employment and rising sentiment combining to create a substantial headwind for the Fed in trying to combat excessive inflation. Here is a wonderful chart that further supports our contention that demand for goods and services will not be thwarted at this level of interest rates given that the American consumer is still flush.

Nearly $1.3 trillion in excess savings are available to consumers. The Covid windfall peaked at nearly $2.1 trillion in July 2021. Consumption since then has eaten into this windfall but much is left to allocate to further economic activity. Given these surplus savings, strong employment, and rising wages, albeit less than inflation, the Fed will likely have to continue to aggressively elevate interest rates. A late-day rally has US equities rising once more, but bonds are off quite a bit today as yields once again rise. The ADP National Employment Report came in at 208,000 today when forecasters were looking for 200,000. We truly haven’t seen a chink in the employment armor at this time. Perhaps Friday’s US Employment Report will begin to show some weakness. I wouldn’t be surprised if it doesn’t.

Pingback: There is NO Pivot on the Horizon! – Ryan ALM Blog