In a recent article in the WSJ, titled “Why Trump Won”, a letter to shareholders of M&T Bank was referenced because of the economic picture that it painted for the “typical” American household. The note was penned by M&T CEO, Robert Wilmers. There are many shocking statistics in his note that clearly highlight the economic struggles of middle America.

The economic divide in this country continues to grow, and its long-term implications may be profound. At a time when we are asking American families to do much more with each $ earned – healthcare, education, insurance, retirement, etc. – there isn’t nearly as much to go around as some of our economists might have you believe.

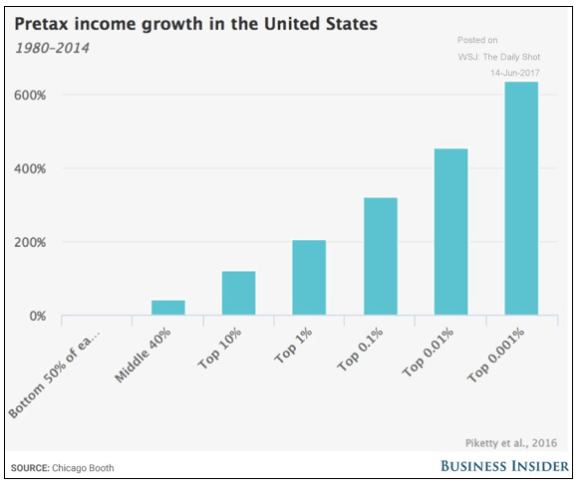

For instance, since 1973, total median household income from all sources, including wages, which comprise more than 80% of income for middle-class families has increased only 13%. That seems incredible to me, but over the last 44 years median household income has only increased by this little, and in fact, earnings for the typical family peaked in 1999.

Furthermore, the precipitous decline in interest rates, which initially had a positive impact on families as they were able to reduce mortgage payments, has crippled their ability to save for retirement or the initial down payment on a home for first-time buyers, among other savings needs. In fact, interest income has declined by $44 billion or 68% for families earning <$100,000. Given that a significant percentage of these households collect little in dividend income, their take of a growing dividend income pie has been only $9 billion.

For those families earning more than $100,000, they have seen 95% of the $162 billion growth in dividend income since 2005 enure to their benefit. As mentioned earlier, the great income divide is growing rapidly.

Regrettably, most American families are still feeling the negative effect from the 2001 and 2008 recessions, as the impact of lost earnings is still being felt. This has lead to only 51% of American households currently feeling as if they are a part of the middle class when back in 2001 63% felt that they were there.

Given the lack of household earnings growth, it is no wonder why the “average” family finds it difficult to fund a defined contribution plan, let alone manage it. It truly bothers me that low DC balances are looked upon as a sign of American consumerism run amuck, as opposed to truly what it represents, which is the lack of financial resources in the first place.