By: Russ Kamp, Managing Director, Ryan ALM, Inc.

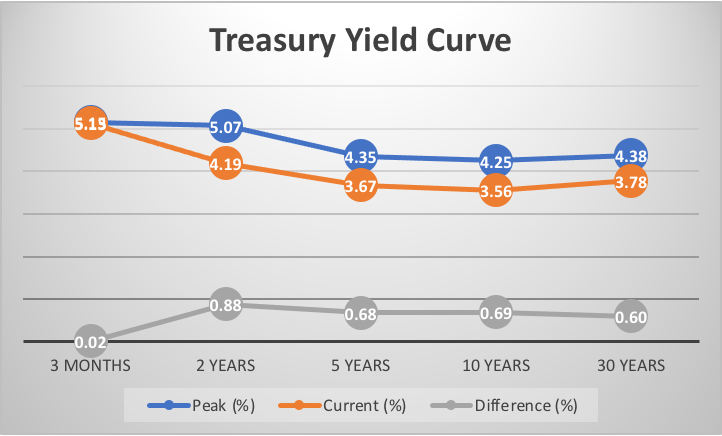

It is time for market participants to be real! I’m not referring to the social media app BeReal that has captured the attention of both young and old. I’m talking about the investment community that is lamenting the rise in US rates as if they are approaching historic levels. Be Real! The current yield on the US 10-year Treasury Note is ONLY 3.40% (10:57 am EST). This yield is certainly up from the historic depths experienced during the onset of Covid-19, but it is certainly nowhere near levels that would be economically crushing!

A bit of history is needed. Following the inflationary decade of the 1970s, the US Federal Reserve drove the FFR target to an unprecedented 22.36% on January 19, 1981. As a result, the 10-year Treasury reached a peak yield in excess of 15%. As I’ve mentioned previously, the yield was 14.9% on 10/13/81 which was the day I entered this industry. 14.90%!!! Now, that was economically crushing, and those higher rates led to a recession that ran through 1982.

For the nearly next four decades, US interest rates plummeted to historically low and unsustainable levels. The Fed’s “aggressive” action during the last 9 FOMC meetings has elevated the FFR all the way back to… 4.75%-5% as the target, or less than 25% of the peak yield reached in 1981. While the FFR sits at roughly 5%, the 10-year Treasury note’s yield has only moved up by 57 bps. That doesn’t seem like it would be significant enough to crush much economic activity. Yet, the hand-wringing by the investment community is incessant. It certainly appears to me that most of the market participants, who haven’t been in the industry for 40+ years or who haven’t experienced significantly higher rates are anchored on the idea that our economy can only function if real rates are around zero.

Again, a little history may be needed. The average nominal yield on the US 10-year treasury note since 1941 is 5.1% or 1.7% higher than what the 10-year is trading at today. During that roughly 70-year period of “higher” average yields, the US GDP annual growth rate was 3.1%! Higher rates and relatively strong growth. You would think that wasn’t possible given all of the whining.

US interest rates remain low relative to history. Employment remains full despite the announced layoffs. Economic activity continues to defy forecasts. Are we really going to see a Federal Reserve cave in a similar fashion to what they did in 1975? Hardly. Our economy is just fine at the present time. For plan sponsors of defined benefit plans, use this period of higher (not high) yielding bonds to improve your liquidity management while securing your promises to participants. Bonds are back and it is a wonderful thing!