By: Russ Kamp, Managing Director, Ryan ALM, Inc.

US Treasury Yields mostly peaked during the fourth quarter of 2022. However, they did stage a brief rally in February, but in no case did they reach the peak yield established during this recent interest rate regime change. Following the collapse of SVB and Signature Bank and the take-over of CS by UBS, US Treasury yields plummeted, as the fear of a broad-based banking crisis drove investors to the safety of US Treasuries. Fortunately, the feared banking contagion didn’t materialize and as a result, Treasury yields are once again reflecting the economic environment. Rates have been rising modestly during the last couple of weeks.

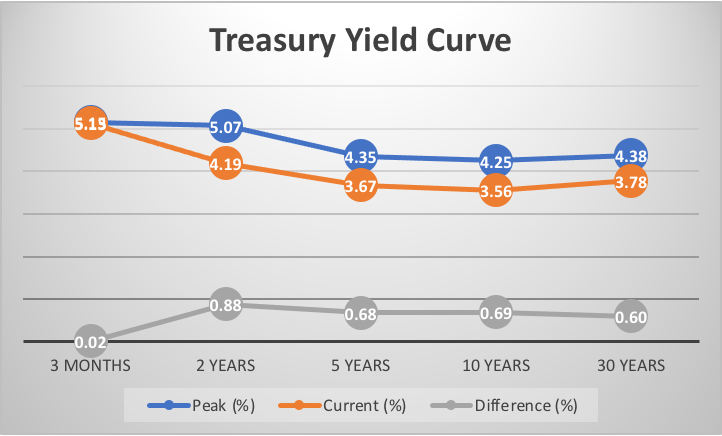

As my chart above highlights, Treasury yields are still below the peak yields of last year, but they are closing the gap as uncertainty persists as to the interest rate path that the FOMC will take in May and beyond. Has inflation been contained? Do we have enough weakness in the US labor force to no longer be concerned about wage growth/pressures? The manufacturing sector activity seems to be collapsing. What about the US service sector since it is by far the largest contributor to US GDP growth?

Despite those many questions, members of the Fed still seem to feel that inflation is too high. In recent days, Federal Reserve Governor Christopher Waller commented that he favored more monetary tightening. “Because financial conditions have not significantly tightened, the labor market continues to be strong and quite tight, and inflation is far above target, so monetary policy needs to be tightened further,” Waller said Friday in a speech in San Antonio, Texas.

We, at Ryan ALM, Inc. have felt that US investors were too focused on the Fed easing, and as a result, artificially drove Treasury yields to unsustainably low levels. The Fed has been very consistent in its communications. Waller is no different, as he “would welcome signs of moderating demand, but until they appear and I see inflation moving meaningfully and persistently down toward our 2% target, I believe there is still work to do.” No ambiguity there!

Bond investors have been willing to hold US Treasuries with yields at significant negative real rates. That isn’t a good long-term strategy. Rates are likely to continue rising. At the very least, it doesn’t appear that the Fed has any appetite to begin easing. Will rates achieve a level across the curve that exceeds the previous peak in this interest rate cycle? In MHO, I think that they will. That result would not be good for total-return-focused fixed-income products, but higher rates and more interest income are great for Cash Flow Matching (CFM) strategies.