The Natixis 2021 Investment Management survey has been released. In one segment of the review 166 investment professionals across North America, who collectively represent $3.9 trillion in client assets under management and are responsible for selecting the products and strategies, were asked to assess the current environment and potential risks. Here are the results:

- 86% of those surveyed believe high valuations are distorted by super-low rates and those valuations don’t reflect company fundamentals (66%)

- 71% think the stock market has grown at a rate that isn’t sustainable (YTD 2022 performance certainly supports that notion)

- Their top portfolio risk concerns are now inflation (76%), interest rates (76%), and volatility (51%)

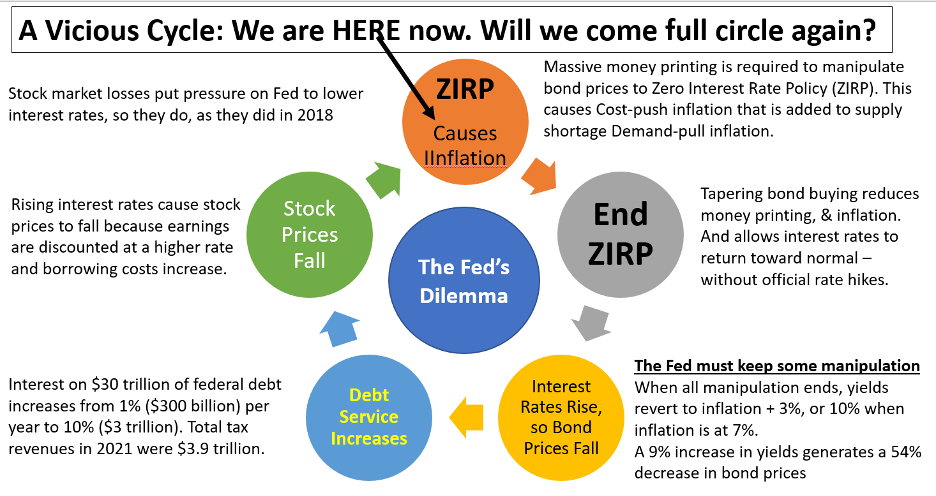

We certainly agree that the uncertainty surrounding rising US interest rates could profoundly impact US stocks. Higher inflation readings than those seen in the last several decades will likely lead to a meaningful seachange in direction for the US Federal Reserve and their dovish policy. If the historically low rates have distorted valuations, it won’t take much of a rise in rates to see equities begin to reflect their “true” valuations. Couple the concerns raised above with the possibility of war between Russia and Ukraine and you have a formula for significantly more volatility.

As a plan sponsor, what are you doing to address these concerns? Are you looking to take risks off the table following a sustained period of improved funded status? If not, why not? If your goal is to SECURE the promised benefits at a reasonable cost and with prudent risk, doing nothing is not acceptable. Not only are you likely to witness underperformance from equities, but from traditional fixed income products, too. As we’ve discussed in several previous blog posts, a modest rise in rates (30 bps) will create enough of a price loss on a 7-year duration bond to produce a negative return for the year. That isn’t much of an interest rate move given the current level of inflation.

Once again, we recommend that pension plans separate the asset allocation decision into liquidity or beta (bonds) and growth or alpha buckets (non-bonds). Convert your current fixed income assets from a total return orientation to one that uses bonds for the certainty of their cash flows to match the plan’s liability cash flows. This conversion will improve the plan’s liquidity allowing the remainder of the assets (alpha assets) to grow unencumbered. The buying of time (extending the investment horizon) is an incredibly important investment tenet. Not sure how to begin? We’ve been doing this for many decades, and we’d be happy to guide you through this process. Call us!