Private pension plans operate under different accounting standards than those in the public sector (FASB versus GASB). As a consequence, private plans are “forced” to use market discount rates (ASC 715 = AA corporate yield curve), as opposed to a static discount rate (the ROA) permitted under GASB. Why is this important? Well, for one, using a static (non-market rate) masks the plan’s true liability. Unfortunately, in this environment of near-historically low-interest rates, that means that the plan’s liabilities are likely severely understated and the funded ratio overstated. as opposed to a static discount rate (the ROA) permitted under GASB. Why is this important? Well, for one, using a static (non-market rate) masks the plan’s true liability. Unfortunately, in this environment of near-historically low-interest rates, that means that the plan’s liabilities are likely severely understated and the funded ratio overstated.

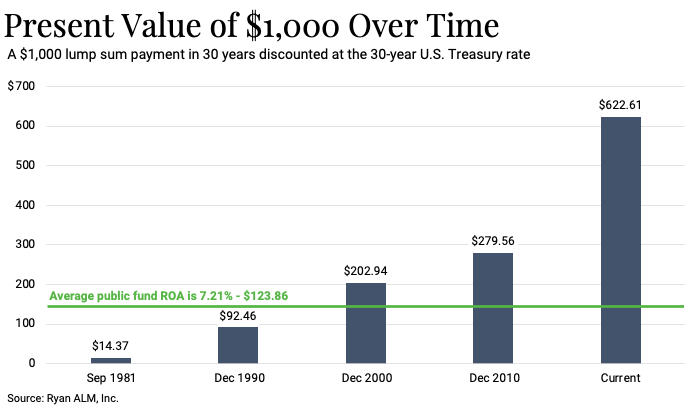

I entered the pension industry in 1981, and interest rates have basically been falling ever since. This has created a huge headwind for defined benefit pension plans, as lower rates not only make it difficult for plans to achieve their return objectives, but it makes it much more expensive to try and defease pension liabilities. As the following chart depicts, it would have cost a plan sponsor only $14.37 to defease a $1,000 30-year liability in September 1981. Today, that same liability costs a plan more than $622! Oh, my!

Oh, how we wish for the days of double-digit interest rates (at least if you are a retiree or a pension plan sponsor) where winning the retirement game would consist of nothing more than understanding your liability and managing to it (i.e. defeasance or dedication)! So simple. But, again, when forced to operate under accounting rules that provide for static measurement of a plan’s liabilities (GASB), changes in interest rates are not understood to have any impact on pension liabilities. Yet, they do, and it can be significant. Despite the decades of falling rates, there is some good news to share. U.S. interest rates have moved steadily higher since touching all-time lows last year. This provides some relief for pension funds that have been crushed by falling rates. Given the current inflationary environment (transitory or not?) one should expect that US interest rates will move higher. As a reminder, the US bond market has provided a “real return” from bonds that is >2% longer-term but currently provides investors a negative return when adjusting for inflation. This situation is not sustainable.

Unfortunately, investing in a traditional return-oriented bond program will likely generate negative returns for the foreseeable future, as the 39-year bull market in bonds likely comes to a close. How high US rates go is anyone’s guess, but it would only take about a 30 basis point move upward in rates to create a negative annual return for a portfolio with a 7-year duration. A move of that magnitude could happen in a blink of an eye. Instead of using a core fixed income manager as a performance generator, use bonds for the certainty of their cash flows to match assets versus liability cash flows. You’ll be happy that you did!

Lastly, get a more frequent view of your plan’s liabilities. We, at Ryan ALM, produce a Custom Liability Index (CLI) that uses your plan’s unique actuarially projected benefits, expenses, and contributions that are produced by your actuary to monitor monthly your plan’s liabilities using multiple discount rates. Managing pension assets to pension liabilities ensures that asset allocation decisions are being done with all of the information necessary to be successful. Not only is it okay to peek at the promises (liabilities) that have been made to your participants… it is absolutely imperative!