By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Let’s give a big thanks to the WSJ for today’s interview with Federal Reserve Bank of Atlanta President Raphael Bostic. It was a great conversation covering a number of important issues related to inflation and monetary policy while incorporating his views on where we are likely to go. As regular readers of our blog know, we’ve been addressing on a fairly regular basis inflation and the impact that it has on fixed income (bonds) and pension funding. There were two specific points raised during the WSJ conversation that echo our thoughts on the subject (confirmation bias in all its glory).

Bostic stated “but what I would say is I try to remind myself that for most people in our society, they don’t have any memories of living in a higher inflation environment, and so there really aren’t anchors of baselines for people to make—to focus on to have a sense of what a reasonable expectation of response will be over the longer run. So I just think there’s just a tremendous amount of uncertainty. People know there is going to be a response, but they don’t have any models in history to suggest that they know what that contour is going to look like. And so there’s just an unease that’s out there as we move forward.” He also said, “we have an imbalance between demand and supply. And as long as that persists, we’re going to have a higher inflation environment. So we’ve got to get that under control, and that’s going to involve some reduction in demand.”

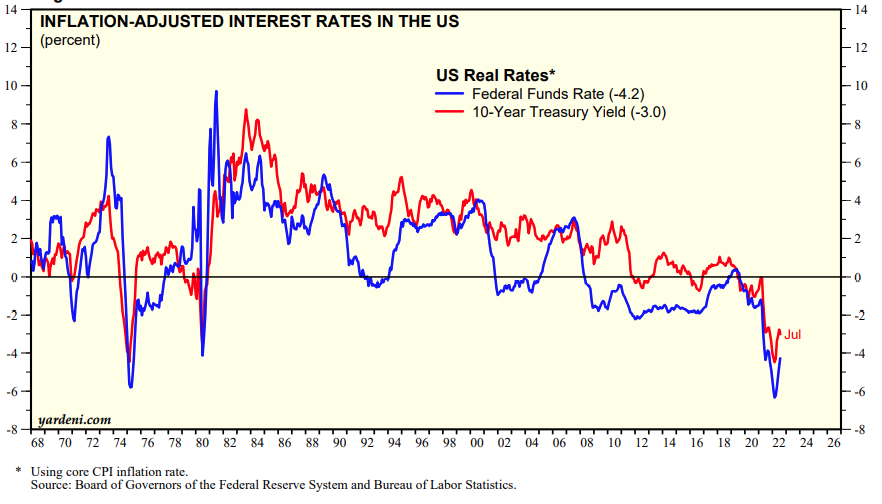

What continues to surprise us, and we recently published a post on this subject, is the expectation that the Fed will have to ease in the near term. That they’ve somehow accomplished its objective. We remain resolute in expecting the Fed to raise rates until they get to a level of positive real rates relative to inflation (an inflation premium). Bostic also cited the current strength of the labor market. He mentioned “the tremendous job growth. We’re averaging, what, more than 450,000 jobs a month per month for 2022? That’s a really big number, and you know, it gave me comfort that we weren’t—that those—we could look through those GDP numbers.” As we’ve stated, you don’t get recessions in an environment of labor strength such as the one that we are experiencing today.

The concept of anchoring at a number that feels comfortable based on one’s prior experience is critically important to understand. Unless you are a 40-year veteran in this industry, you’ve not experienced the negative effects of outsized inflation and interest rates. It is quite amusing to read about the negative impact on demand of a Fed Fund’s Rate at 2.25% when it was >14% the last time we experienced an inflation rate above 8%, which was 4 months into my career. Has housing demand appeared to stall at this time? Yes. But for how long? People need a residence. Rental inflation continues to persist at untenable levels. The demand for housing will adjust to the current environment at some point just as it did for my family and friends who bought their first homes at interest rates that exceeded 11% in the early to mid-’80s.

Lastly, Bostic sees the Fed eventually getting to a Fed Funds Rate above 3.5%. Personally, I don’t see that level diminishing demand and tamping down inflation to a great extent, especially given the strength of the US labor market. In any case, the Fed is far from done, and getting to an inflation level of around 2% will take much longer than most market participants are currently believing.