By: Ron Ryan, CEO, Ryan ALM, Inc. and Russ Kamp, Managing Director, Ryan ALM, Inc.

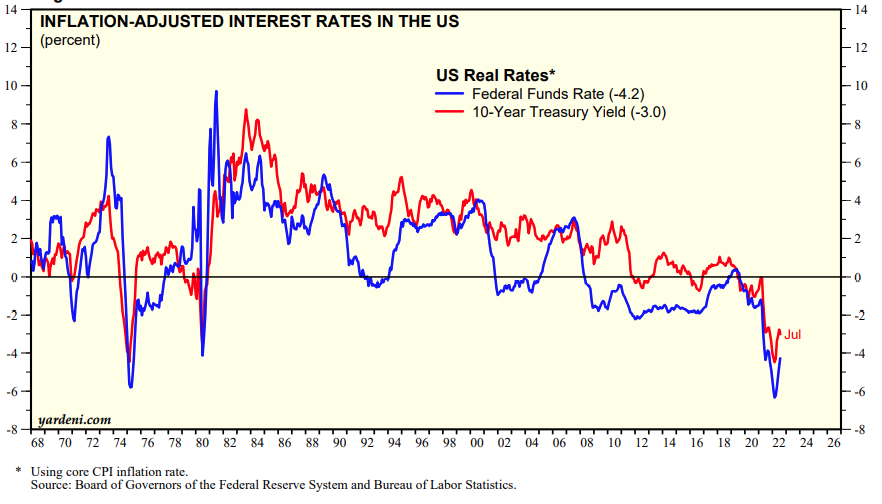

America’s investment community has enjoyed a history of real interest rates or an inflation premium on the 10-year Treasury nominal rates. As the chart below indicates, whenever real rates went negative (1975 and 1981, primarily), it proved temporary as it was followed by an increase in nominal yields until a real yield was achieved. The US Federal Reserve has indicated that they want a return to positive real rates with an inflation premium. We are shocked that “investors” aren’t demanding a real yield advantage in this environment given all of the uncertainty related to the significantly elevated inflation rate which has been brought about by a number of factors, including government stimulus, enhanced wages, full employment, war, Covid-19, production, and shipping delays, etc. Why?

At the current level of inflation (July’s CPI-U # was 8.5%), one would expect the 10-year Treasury yield to be roughly 9.5%-10.5% given its long history of providing a real yield of 1-2%. However, the 10-year Treasury note currently has a yield of ONLY 2.78%! This yield provides the investors with a negative real yield of nearly 6%!

As everyone knows, the Fed has begun raising the Fed Funds Rate, which currently sits at 2.25%. They’ve indicated that further rate increases are necessary to help tame inflation. That said, even if these recent increases in the Fed Funds Rate somehow tamp down economic growth to the point that inflation falls to 3%, history suggests that the 10-year Treasury yield should be somewhere around 4% to 5%, which is a far cry from where we are today. Again, we ask, why are investors so complacent? Are they anchored in the idea of low-interest rates forever and always? Don’t they understand what transpired in the 1970s into the early 1980s?

For anyone who needs a history lesson, here is a conversation between Paul Volcker and Ray Dalio that was posted by Ray on his LinkedIn.com page. It is a wonderful reminder that true leadership is needed during periods of great uncertainty, even if it results in personal harm to one’s reputation. Increasing the Fed Funds Rate to only 2.25% is likely to do very little to reduce inflation, especially as we are at full employment with rising wages. The Fed is going to have to GET REAL if we as investors are to enjoy real yields.

Thanks Ron

Hereâs my version

Ron Surz

(949)488-8339

900 Calle Venezia, San Clemente, CA 92672

Hi Ron – I don’t see a link to your article. Please repost or email to rkamp@ryanalm.com – thanks, Russ

Pingback: Bostic on Inflation in today’s WSJ – Ryan ALM Blog