By: Russ Kamp, Managing Director, Ryan ALM, Inc.

There appears in today’s WSJ an article by James Mackintosh titled, “The Markets Don’t Believe the Fed”. It is incomprehensible to me that this continues to be the mindset of the average investor given the fact that the Fed controls short-term US interest rates. Whether you believe that the economic fundamentals exist to support aggressive interest rate policy, the Fed is in control. I began posting blogs about “believing” the Fed in March 2022. My first post, “You Should Believe The Fed” stated that “we (Ryan ALM) are NOT in the habit of forecasting rates, but after a 39-year bull market for bonds that produced historically low absolute and real interest rates, we felt pretty comfortable in our expectation” that US interest rates would rise.

I further wrote, “if you don’t believe us, I highly recommend that you listen to the US Federal Reserve, as they came out very aggressively yesterday (March 16th) and indicated that the 25 basis point move in the Fed Funds rate (first increase since 2018) would be followed by 25 bps increases at each of the remaining six meeting in 2022. Incredibly, those 25 bps increases didn’t occur, because they were superseded by a 50 bps increase, four 75 bps increases, and finally earlier this week another 50 bps elevation in the Fed Funds Rate (FFR)!

I went on to ask “is your portfolio structured to withstand this aggressive move upward in rates? What have you done to secure the promised benefits? If nothing has been done, are you prepared for deterioration in the plan’s funded status and increased contribution expenses? This is the reality that our pension industry is facing.” Regrettably, most sponsors and their consultants have done little to nothing to protect and secure the promised benefits. Expectations now exist that the Fed will raise the FFR to a level that exceeds 5% given the stickiness of “core, core” inflation and concerns that an easing in its restrictive policy might just result in a similar and painful outcome to what was experienced during the late ’70s and early ’80s.

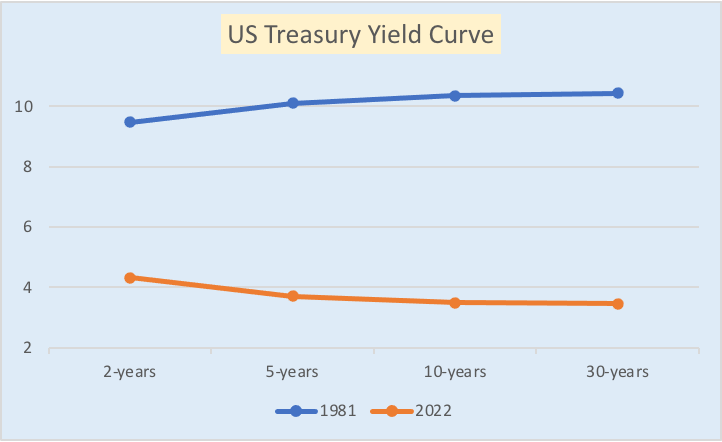

Given the reluctance on the part of market participants to believe the Fed, long-term interest rates have fallen significantly during the last couple of months creating an environment of easier money conditions similar to what we witnessed earlier this year. 30-year mortgage rates are once again below 6.5% having peaked at 7.1% during this rate cycle. With long rates in the mid-3% range, just how much economic activity will be thwarted? The US labor market remains strong and wage growth remains well above the level desired by the Fed. Initial jobless claims, which had recently been elevating, came in 20,000 below forecast to a low level of 211,000.

I believe that it is fair to ask, “what has the Fed accomplished to date”? Their policy actions certainly haven’t driven inflation anywhere close to the desired 2% target. It appears to me that the Fed has much more work to do. Will market participants finally believe them? As we witnessed in 2022, you ignore the Fed at your own peril.