By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Yesterday, Ryan ALM was invited to participate in a “Lunch and Learn” event with a major asset/liability consulting firm. Our agenda was to provide education related to Cash Flow Matching (CFM), which this leading firm wasn’t actively using. It was a great opportunity for us, while hopefully opening some eyes as to the significant benefits of CFM. We received a lot of terrific questions from those in attendance, both in-person and virtually. One of the more important questions had to do with interest rate risk and the impact on CFM strategies in a rising rate environment. It was the perfect set-up question for our team and strategy.

Total return-focused fixed-income strategies are highly interest rate sensitive. These strategies have been beaten down significantly (BB Agg. -15.7% YTD through 10/31/22) in this current rising rate environment. Fortunately, CFM strategies are not interest rate sensitive. How’s that? The matching of asset cash flows (interest and principal) against liability cash flows focuses on their future values. A $5 million monthly benefit payment 10 years out is still $5 million no matter which way rates move. It is this characteristic, among other positive attributes, that makes this strategy so critically important to the success of managing a defined benefit pension plan.

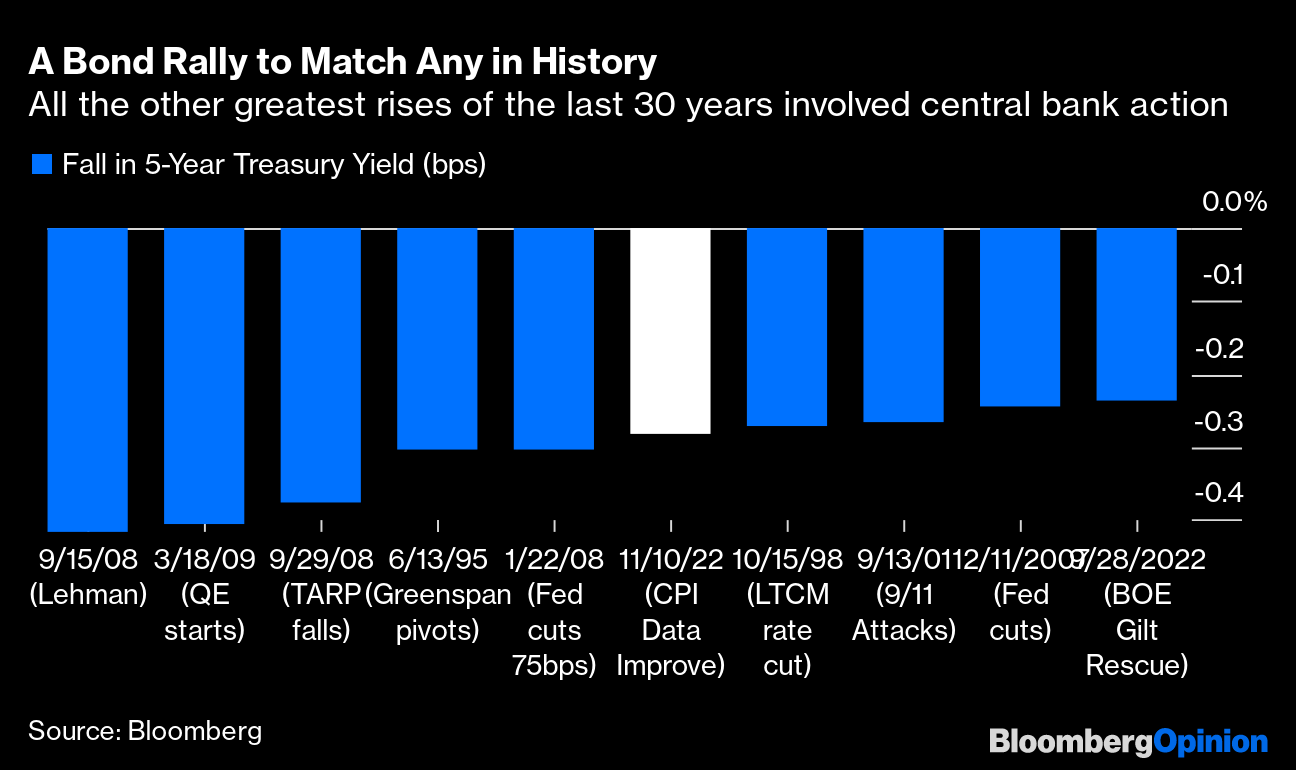

It has been 40 years since we last had a prolonged bear market in bonds driven by changing monetary policy. In 2022, rates have risen dramatically across the Treasury yield curve and credit spreads have widened in the process. Both of these actions have been driven by Fed policy. Does anyone really know where future rates are going? Based on today’s market action you’d come to the conclusion that the US Federal Reserve has accomplished its objective. Have they? Core inflation remains elevated at 6.3% annually. The CPI is still at decades-high levels at 7.7%. Sure, the trend may be indicating some downward action on inflation, but with a Fed Fund’s rate at 4%, have they elevated rates significantly enough to tamp inflation to the Fed’s 2% target and a market with real rates?

Wouldn’t you want to use a strategy that doesn’t care where interest rates go? Wouldn’t it be comforting to know that asset cash flows are matched almost precisely with liability cash flows for some defined period of time? That this relationship doesn’t change if rates rise or fall? Wouldn’t it also be incredibly helpful to have bought time (considerable time?) for your plan’s growth/alpha assets to grow unencumbered? Oh, and by the way, CFM portfolios that utilize investment-grade corporate bonds are producing yields in the 6% range.

CFM strategies are the perfect “sleep well at night” offering, especially at the current level of rates. Unfortunately, duration-matching LDI strategies that used leverage were the impetus behind the near collapse of the UK’s pension system. Those strategies engaged in SWAPs are highly interest rate sensitive. That risk may have been acceptable during the last 40 years of accommodative Fed policy, but we are in a different ball game at this time.

Don’t create an asset allocation structure that is highly dependent on the direction of rates. Bifurcate the plan’s assets into two buckets – liquidity and growth. Use CFM for the liquidity bucket and build a robust growth portfolio that is no longer a source of liquidity. Let a CFM strategy fund Benefits and Expenses which will allow the alpha assets to grow unencumbered. There is absolutely no need for a cash sweep of income from the growth assets to fund B+E. Let that income be reinvested in potentially higher-returning strategies.

Being able to sleep better at night shouldn’t be discounted!