By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Anyone of us can quote statistics from various surveys highlighting the fact that retirement is getting out of reach for many Americans. The Mind over Money survey by Capital One and The Decision Lab is the most recent one that I read. Their findings are pretty dire with 77% of Americans feeling anxious about their finances, with 68% worried about saving enough for retirement. I can’t say that I blame them! In an environment of spiraling inflation and deteriorating market performance for traditional asset classes, why would we think that individuals would be feeling anything other than uneasy?

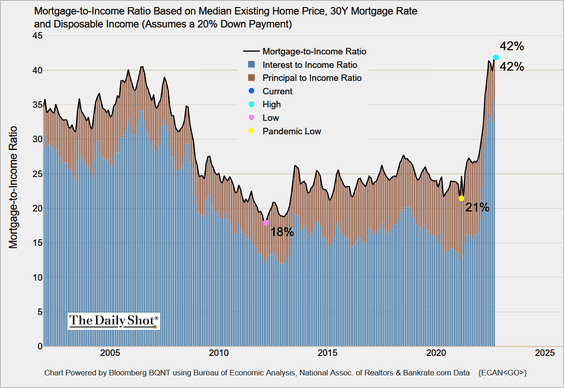

Despite the fact that the US labor market continues to show incredible strength, decades of low real earnings growth have crushed the average American worker. We are witnessing some nominal growth in earnings at this point, but real wage growth continues to evade us by about 3%. If Americans aren’t saving in this environment, where is their income being spent? Look no further than housing costs. As the chart below reflects, being able to buy or finance a home has gotten incredibly challenging if not nearly impossible!

The Mortgage-to-income level has more than doubled since roughly 2013 and it is twice what it was at the Pandemic low. Furthermore, this study used a 20% down payment in the calculations. How realistic is a down payment of this magnitude for young couples who in many cases are still (and will be for the foreseeable future) burdened with student loan debt? According to the National Association of Realtors (NAR), the average down payment in 2022 is 13%. For those aged 23-41, the down payment drops to between 8-10%. Given that we are looking at a down payment that is roughly half of what was used in this analysis, we can quickly determine that the financial burden to buy a home is far worse than what is being reported at 42% of one’s median disposable income.

Asking untrained individuals to fund, manage, and then disburse a retirement benefit through a defined contribution plan is poor policy. Expecting those same individuals to have any “discretionary” income after paying for housing, education, food, energy, and healthcare is unrealistic! We have a broken retirement industry. Let’s hope that rising US interest rates will encourage corporate plan sponsors to once again provide a true retirement benefit to their financially anxious and struggling employees.