By: Russ Kamp, Managing Director, Ryan ALM, Inc.

The following was a headline for a MarketWatch.com article, “The 401(k)’s success has been overlooked and will help even more Americans”, which I saw on a LinkedIn.com post earlier today. Sure, some American workers have benefited from their ability to fund a DC account, but the vast majority of Americans are struggling.

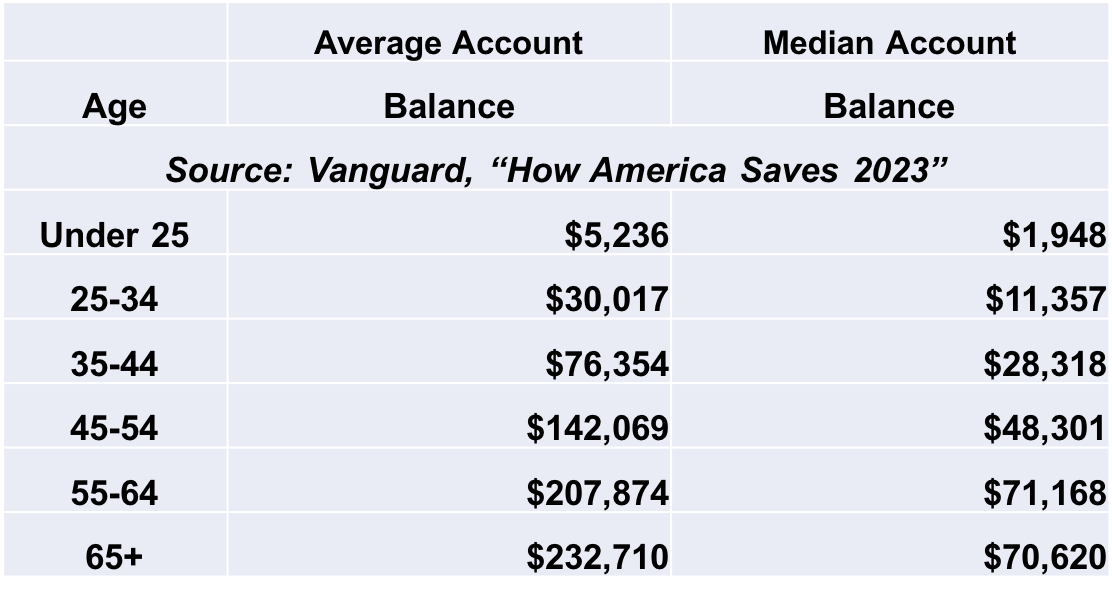

Does This look like success?

Perhaps the level of savings would be okay if DC plans were actually supplemental retirement vehicles, but since they have morphed into the primary retirement program for most workers, this is a disaster. I’m tired of the fact that we only ever see “average” balances reported. Of course, a few well-funded balances will drive the average up. Let’s focus on the MEDIAN account balances. Does a $70,620 account balance for a 65+ year-old participant look like a successful outcome? How much would that balance provide on a monthly basis for a roughly 20-year retirement?

If I were fortunate to have a defined benefit plan that provided $2,000/month (which isn’t a lot) for 20-years, I would receive $480K in retirement which is 6.8Xs what the 65+ year-old with the median account balance has today. It is a far cry when compared to the view that $1.4 million is the balance needed to have a dignified retirement today. It is silly to believe that the average American has the disposable income, investment acumen, and predictive ability to gauge how long they will live in order to allocate this meager balance to ensure that the recipient doesn’t outlive their savings.

The investment industry can celebrate all they want as it relates to the total accumulated wealth in defined contribution plans, but for the “median” American, it just isn’t close to being enough. Defined benefit plans should be the backbone of our retirement system, while DC plans occupy the supplemental role for which they were designed. As someone in that LinkedIn.com post stated, “the numbers don’t lie”. I would certainly agree, but that doesn’t mean that the #s are revealing success!