We, at Ryan ALM, are pleased to share with you the Ryan ALM Q3’21 Newsletter. In keeping with past newsletters, we provide the reader with a unique perspective on pension liabilities and how they have performed relative to pension assets. As a reminder, the primary objective in managing a defined benefit plan is to secure the promised benefits at low cost and with prudent risk. Having a frequent understanding of a plan’s liabilities is the ONLY way to accomplish the securing of benefits. In addition to several exhibits focused on liability performance during the quarter, we provide the reader with links to both recent research and pension-related blog posts. We hope that you find our thoughts insightful.

It’s Happened Before!

Are you thinking that another major equity market decline isn’t possible? That we are once again entering into a new paradigm (remember 1999) casting all previous ideas on market fundamentals out the window? If yes, I implore you to think again! Market fundamentals still matter. Sure, value is always in the eye of the beholder, but eventually value does in fact matter. It is difficult to identify today any asset class exhibiting cheapness or fair value when looking at the landscape of potential investments for pension plan sponsors and their advisors. Please don’t forget the significant damage that was inflicted on pension plans and E&F’s during the Tech Bubble bear and the Great Financial Crisis when the bull markets went poof! Market declines of roughly -48% and -52%, respectively, were generated.

We recently pointed out the fact that in both of those bear markets the S&P 500 registered a low at the bottom of the bear markets near 760. Given the S&P 500s current value, a -50% decline would bring the S&P 500 to a price of 2,265. Should a retest of the lows of the last 20-years be in the cards, the return would be roughly -83.1%. Come on, Russ, when have we seen declines of that magnitude? Well, students of the markets don’t have to go back too far to remember that the NASDAQ declined -76% when the tech bubble burst. Also, as the chart below highlights, the S&P 500 fell nearly -85% in 1932. I can just hear the roar from the crowd chanting the mantra once again that “it is different this time”. Maybe, but maybe this will prove once again to be another chapter in the normal cycles of equity market performance.

I bring this concern to your attention because pension America – private, public, and multiemployer – have benefited tremendously from the equity market rally since the bottom achieved on March 9, 2009. Please don’t continue to subject this wonderful improvement in funding to the whims of the markets. I have no clue when the next correction will come, but I do know that one will come. Based on the market’s current valuations, I don’t think that the impact will be tamer than the usual bear market experience, which has produced an average -37% correction in the previous 20 bear markets! Ouch! Take risk off the table, ensure that you have the proper liquidity necessary to meet benefits/expenses during the downdraft by building a cash flow matching portfolio to meet those projected outflows, as traditional bonds will not preserve capital in a potentially rising interest rate environment. This strategy will allow your equities and other risk assets the time necessary to work through any turbulent market environment.

Potentially Exciting News for our Seniors

House Ways and Means Social Security Subcommittee Chairman John Larson, D-Conn., plans to introduce Wednesday a new bill called Social Security 2100: A Sacred Trust. Importantly, the bill will include a change in the inflation rate index from the CPI-W to the CPI-E. As a reminder to our regular readers, I’ve been encouraging our legislators to make this change for years (7 blog posts, including the most recent on 6/14/21). This inflation rate has a greater weight assigned to healthcare related spending, which continues to be one of the most critical expenditures for our Senior population. In addition, the bill would tax incomes >$400,000. The Social Security payroll tax is not presently applied to wages greater than $142,800. The new payroll tax will be applied to those wages up to the current maximum and for wages earned over $400,000, which presently impacts about 0.4% of our workforce. 2021 could be very exciting for our SS recipients given the nearly historic COLA announced recently and a possible shift in the inflation index.

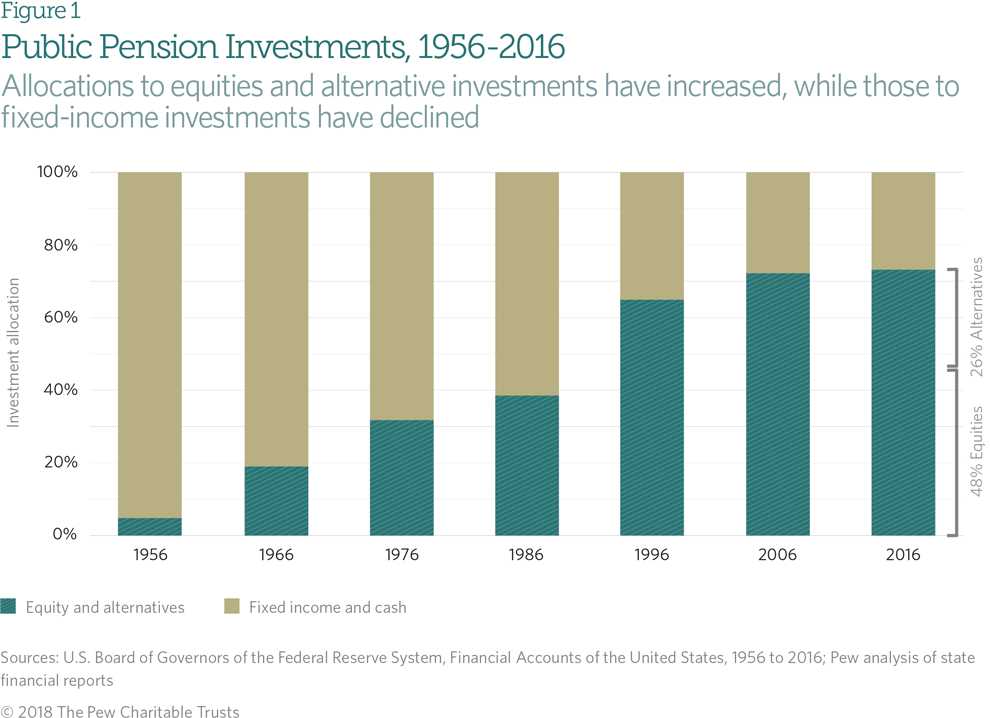

Massive shift to Risk Assets – Are DB Plans Better Off?

As the chart below depicts, there has been a massive shift in the asset allocation of DB plans since the mid-50s from mostly fixed income allocations to significant exposure to risk assets.I suspect that most of the motivation has been driven by the plan sponsors desire/need to achieve a target return or hurdle rate (ROA). The idea is if the ROA is achieved then contribution costs remain as projected…but has this goal been achieved?

Actuaries do a wonderful job (very difficult task) of forecasting the plan’s liabilities despite ever changing inputs, such as life expectancy, which fortunately has expanded leaps and bounds since the 1950s. I often say that my crystal ball is no better than anyone else’s if not worse. Actuaries can’t afford to have a crystal ball that is foggy. Their forecasts of future benefit costs are amazingly accurate despite the many inputs that drive their calculations. Given the reliability of their data and the importance of meeting those future expenditures, why aren’t plan sponsors and their consultants using these insights to drive asset allocation and investment structure decisions?

Most DB plans were well overfunded in 1999. They had the opportunity to remove substantial risk from their portfolios by defeasing the plan’s Retired Lives Liabilities and securing the funded status. To achieve the ROA, asset allocation models did the opposite! As a result, their increased equity exposure got crushed when significant market corrections occurred in 2000-02 and again in 2007-09. Did we learn anything? It doesn’t appear that we did, as equity exposures continue to ratchet higher despite the appearance of dramatic overvaluation. Could it be that fixed income, after an historic 39-year bull market, scares plan sponsors and their consultants to a greater extent? Could be. However, as we’ve stated on several occasions, bonds should not be viewed as performance or Alpha assets in this environment. They should be used exclusively for the certainty of cash flows that they generate as liquidity assets or Beta assets.

We believe that a cash flow matching implementation that defeases a plan’s net benefit payments chronologically from next month’s needs to as far out as the allocation will permit will provide many benefits, including: 1) improved liquidity, 2) elimination of interest rate risk on the bonds that are used to defease liabilities, 3) buys time for all of the equity exposure now in DB plans, and 4) allow the alpha assets (non-bonds) to grow unencumbered, as the re-investment of dividends is critical to the long-term success of investments, such as the S&P 500.

Increasing equity exposure in the hope that a greater return will reduce the need for future contributions hasn’t yet proven to be true. It has ensured that total expenses (management fees) have gone up, as well as the overall volatility of the funded status, but success hasn’t been guaranteed. Given where valuations currently reside, either dramatically reduce the equity exposure or reconfigure your fixed income exposure from a total return seeking mandate to a cash flow matching implementation that now allows time for the alpha assets to recover after the next equity market correction. There will be one.

Ryan ALM Pension Monitor for 3Q’21

Each quarter, Ryan ALM produces the “Pension Monitor” to reflect how pension liabilities are behaving versus plan assets. We believe that pension plan liabilities need to be measured and monitored regularly. Without knowledge of plan liabilities, the allocation of plan assets cannot be done appropriately.

The funded ratio/status of pension plans are present value calculations. Each type of plan is governed by accounting rules and actuarial practices, which determine the discount rate used to calculate the present value of liabilities. Single employer corporate plans are under ASC 715 (FASB) discount rates (AA corporate zero-coupon yield curve); multiemployer plans and public plans use the ROA (return on asset assumption) as the liability discount rate. The difference in liability growth between these plans can be quite significant, which will affect funded status and contribution levels.

Although the third quarter of 2021 saw funded ratios decline marginally, the strong rebound in markets following the onset of Covid-19, has enabled a plan’s total assets to outperform liabilities during the last 18 months. Whether the plan is a public, corporate, or multiemployer plan, assets have been aided by strong global equity markets and liability growth has been tempered by rising interest rates. This combination has been great for pensions that have witnessed strengthening funded ratios and improved funded status, especially for corporate plans that utilize a discount rate more reflective of the current market environment. We believe that the time is right for plan sponsors to take some risk out of their pension plans.

Please don’t hesitate to reach out to us if we can answer any questions related to asset/liability management.

Biggest Increase in 40-years

The Social Security Administration has just announced that SS recipients would see the greatest annual increase in 40 years. As we reported back in June, the COLA is based on the inflation rate during the three Summer months. It was just announce that the increase will be 5.9% for 2022. The average recipient will see a monthly increase of $92 for a total of $1,657 per month or $19,884 per year. Let’s hope that inflation does prove transitory providing our senior citizens and those receiving disability benefits the opportunity to get ahead just a little bit.

ASOP 4 – Third draft of the standard was approved in June

The Actuarial Standards Board (ASB) is responsible for setting standards for actuarial practice in the United States and they accomplish that objective through the development of Actuarial Standards of Practice (ASOPs). One such standard, ASOP No. 4 addresses “measuring pension obligations and determining pension plan costs or contributions”. This guideline is not specific to either FASB or GASB, so this standard should be applied by all actuaries when performing the following tasks:

Measurement of pension obligations, funded status, solvency risk, and the pricing of benefits. There are several other areas of focus, but the assessment of a Low-Default-Risk Obligation Measure was the one that grabbed our attention. Section 3.11 of ASOP No. 4 states that “when performing a funding valuation, the actuary should calculate and disclose a low-default-risk obligation measure of the benefits earned or costs accrued as of the measurement date”. When calculating this measure, the actuary should select a discount rate derived from low-default-risk fixed income securities whose cash flows are reasonably consistent with the pattern of benefits to be paid in the future. Sounds like cash flow matching to us. Examples of permitted discount rates include, US Treasury yields, rates implicit in the settlement of pension obligations, yields on corporate bonds of the two highest ratings given by recognized rating agencies, multiemployer current liability rates, and non-stabilized ERISA funding rates for a single employer plan. Notice that the return on asset assumption (ROA) is not one of the approved rates.

The actuary should provide commentary to help plan sponsors AND participants understand the significance of the low-default-risk obligation measure with respect to the funded status of the plan, future contributions, and importantly, the security of participant benefits. It is up to the actuary to use their professional judgement when producing the commentary. This measurement is not intended to highlight one discount rate as being the most appropriate. It is intended to provide a more transparent view of the current financial condition of the plan with respect to its future commitments. Final comments on this third draft are due by October 15th.

Ryan ALM is one of the few vendors that provide U.S. Treasury STRIPS and AA corporate zero-coupon (ASC 715 requirement) discount rates. We also created and provide a Custom Liability Index (CLI) as a monthly report that calculates: Future Value (grows and net of contributions), Present Value, Growth Rate, Interest Rate Sensitivity, and Statistical Summary (average YTM, duration, etc.) of the plan’s liabilities.

Credit Ratings Migration Downward

Most participants in the US pension industry know that the credit rating downgrade trend has been occurring for quite some time, but they may not necessarily appreciate the magnitude. The US bond market has shifted heavily toward BBB from AA and A rated bonds as nearly 70% of new issuance has been BBB (see chart below).

At the conclusion of 1990 roughly 11% of the corporate bond market was rated AAA. Today, there are exactly 2 corporate bonds – Microsoft and Johnson & Johnson – that maintain a AAA rating. Incidentally, this rating remains one notch higher than the US government, which has had a AA+ rating from S&P since 2011. The BBB segment of the US bond market was roughly 25% of the investment grade (IG) universe in 1990. Today, more than 50% of the IG universe is BBB and there doesn’t seem to be any let up at this time, as cheap financing has led to this borrowing craze.

Fortunately, default rates have remained incredibly low since the Great Financial Crisis for all credit ratings within the IG universe. We, at Ryan ALM, have taken full advantage of the growing BBB segment within our cash flow matching portfolios providing our clients with a terrific yield advantage relative to the pricing of their plan’s liabilities (ASC 715 AA corporate bond yield curve discount rates). Also, it should be pointed out that credit spreads for AA bonds have tightened significantly relative to BBB bonds elevating credit spread duration risk for that segment of the IG universe.

Highly unlikely!

According to the Department of Labor, the median wage in the US in 2002 was $38,655 (adjusted for inflation). In 2019, the median wage had “rocketed” all the way to $39,101! Amazingly, we have ONLY seen inflation adjusted wages grow by $546 since 2002. Oh, my! During that nearly two decades we’ve witnessed further deterioration in the use of defined benefit plans (DB) and the greater emphasis on defined contribution plans (DC) that require individuals to fund, manage, and then disburse a retirement benefit. Do you really think that this is feasible given the modest growth in wages? Furthermore, we have seen housing costs (both purchase and rent), educational costs (look at student loan debt), healthcare, and health insurance premiums explode with each outpacing the CPI. This experiment will end in catastrophe.

Regrettably, many Americans don’t have access to an employer sponsored retirement benefit of any kind. We know from studies that most Americans don’t save outside of their employer-sponsored plan. For those that do have an employer capable of providing their employees with a plan, only about 70% of the employees take advantage of the savings vehicle. Furthermore, most aren’t coming close to maximizing their full deduction, and who can blame them given the meager wages. It costs a certain amount to provide for oneself and many Americans aren’t earning enough to meet that threshold. Why do we think that saving for a future retirement is even possible – it isn’t!

Why have we allowed this development to occur? Why have we determined that it is okay for DB plans to be frozen and terminated in favor of DC offerings that don’t come close to providing individuals with the necessary assets to enjoy a retirement, let alone one that is dignified. This social experiment will be a failure! I don’t think that we really need more time to see that insignificant DC balances will be adequate to keep Americans from falling onto the social safety net of our federal government. It is time to embrace the use of state-sponsored defined benefit plans. If corporate America doesn’t want to own the pension liability – fine! But they should at least be mandated to make a contribution on behalf of an employee into a state run defined benefit plan that is professionally managed, low cost, and one that provides a monthly annuity upon retirement.

Like A Bridge Over Troubled Water

As a young man growing up in Palisades Park, NJ, I loved the folk duo Simon and Garfunkel, and one of my absolute favorite songs was “Bridge Over Troubled Water” (released in January 1970). Much to the chagrin of my family, I will still belt out that song when I hear it. However, until yesterday I would not have thought that I’d use this song as a metaphor for potential issues in the pension/investment industry, but Ryan ALM’s Head Trader, Steve DeVito, provided us with the following chart and title that is just perfect for what we try to do for DB pension plans.

As the graph highlights, the decade of the ’00s was tragic for pension America. As we recently reported, the decade of the ’90s ended with most pension plans fully-funded if not in surplus funded status. But those funded ratios soon plummeted as the result of two incredible drawdowns in the S&P 500 (8/20 – 9/02 and 10/07 – 2/09). Had pension America engaged in a de-risking strategy when pension plans were fully funded in the 1990s, such as cash flow matching that would have protected what had been earned, the impact of those two major market declines would have been somewhat muted. First, DB plans would have maintained a greater allocation to fixed income, which performed superbly during that decade when equities truly suffered, while importantly matching the growth rate of the plan’s liabilities. Second, a cash flow matching bond strategy buys time for the alpha assets (non-fixed income) to grow unencumbered. Why is that important? The graph below highlights the fact that it took thirteen years for the S&P 500 to recover it’s $ value as of 1999.

By permitting the assets to grow without being a source of liquidity, equities benefit from the reinvestment of dividends. Studies have shown that more than 50% of the S&P 500’s return over 20+ rolling year periods is from dividend reinvestment. Furthermore, by establishing a cash flow matching program that provides for the payment of benefits and expenses, a plan is not forced to raise liquidity from equities when valuations have already been driven lower. Lastly, it also protects plans from making improper asset allocation decisions during periods of distress.

Pension America has benefited from an amazing period of performance since the Great Financial Crisis ended in early 2009. Funded ratios have improved for all DB plan types. It would be sinful to see this improved funding wasted as a result of inaction. It is time to secure the plan’s cash flow needs, funded ratio, and contribution expenses. A pension plan should covert the current fixed income allocation from a return seeking instrument to one that focuses on a bond’s cash flows. In a rising interest-rate environment such as the one that we might be experiencing, traditional fixed income strategies will likely generate negative total returns with as little as a 30 basis point move upward in rates. That could happen very easily. However, in a cash flow matching strategy, where we carefully match maturing principal and income cash flows with benefits and expenses, we are ensuring that the plan’s liquidity needs are being met and that interest rate risk is being eliminated, as future values are NOT interest rate sensitive.

Defined benefit plans need to be protected and preserved for the millions of plan participants who are counting on that promised benefit. Let’s not give those supporting these plans ammunition to seek their destruction. Risk reduction and the securing of benefits should be at the top of every plan’s working agenda. I’m not smart enough to know when the equity markets (perhaps bonds, too) will crater. I just know that history DOES repeat itself in the pension industry.