No new Special Financial Assistance (SFA) grants have been approved this week, as we continue to sit with five pension plan applications that have been approved by the PBGC to date. However, the House Committee on Education and Labor that is Chaired by Congressman Bobby Scott (D., VA) has released a Multiemployer Pension Rescue Tracker to highlight the pensions “saved” and businesses protected under the American Rescue Plan Act (ARPA). To date, the ARPA legislation has supported through the SFA grants the pensions for 8,088 participants and roughly 170 businesses (contributing employers). The number of businesses may be inflated as some of these contributors may participate in more than one of the approved plans. It is a good start, but much more needs to be done as the five plans represent a very small subset of those plans that remain eligible to file and receive grant money.

More To Come?

Every once in a while you come across an article that just strikes a chord with you. I’m pleased to know Ron Surz, who is as passionate about trying to help our retirement industry as I am. The following article has been produced by Ron who has been elevating his concerns for years regarding traditional target-date funds. Given the fact that most of us only have access to a DC plan, coupled with current market levels, there is an urgency in his message that should be heeded. I hope that you find Ron’s insights compelling.

Most assets suffered losses at the start of the year 2022. Only commodities were spared as inflation, and inflation fears drove up their prices. Consequently, your 401(k) investments lost value. Target date funds of all vintages declined but — no surprise — safer TDFs defended. The “TO – THROUGH” TDF label is a distinction without a difference. “SAFE or RISKY” is much more meaningful. Defined benefit plans also suffered losses like 2040 TDFs since these roughly match DB allocations.

Legend has it that January performance predicts the performance for the year. There’s reason to believe that there’s more to come in 2022.

There is more to come

We enter 2022 with a host of economic threats:

- COVID

- Inflation

- Stock market bubble

- Bond price manipulation (ZIRP)

- Unprecedented money printing

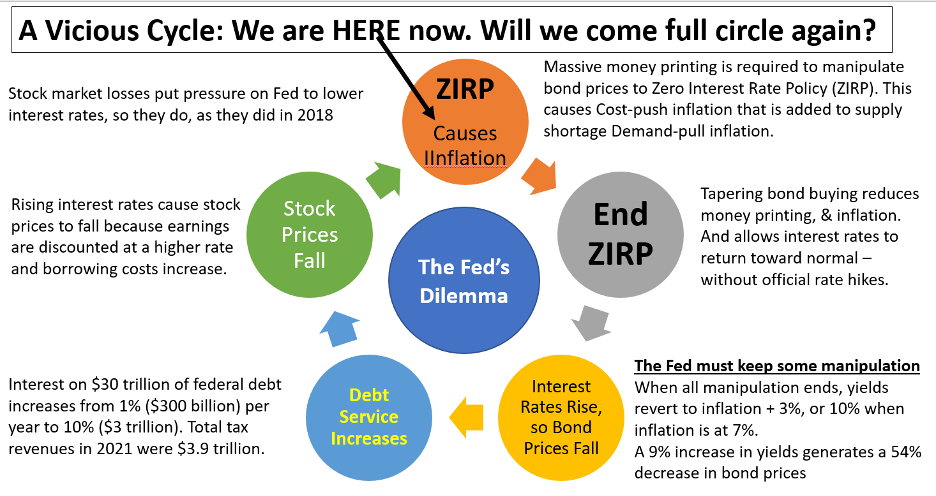

The Federal Reserve has tried to calm the investing public with a promise to control inflation, but this will not be easy. The Fed is caught in a cycle that will be hard to break. If it raises interest rates, stock and bond prices will fall. In a repeat of 2018, the Fed will be pressured to reverse course and try to jam interest rates back toward zero.

But 2022 is not like 2018 because we have serious inflation in 2022 at 7% and threatening to go higher. This time implementing a zero interest rate policy (ZIRP) will fuel the current inflation fire because it requires massive money printing. The Fed can’t have it both ways. It cannot control inflation and continue to buoy up stock and bond prices.

Current inflation is a combination of demand-pull due to supply shortages and cost-push due to $13 trillion in money printing, which is more than our 10 most expensive wars. It is not transitory.

A prediction

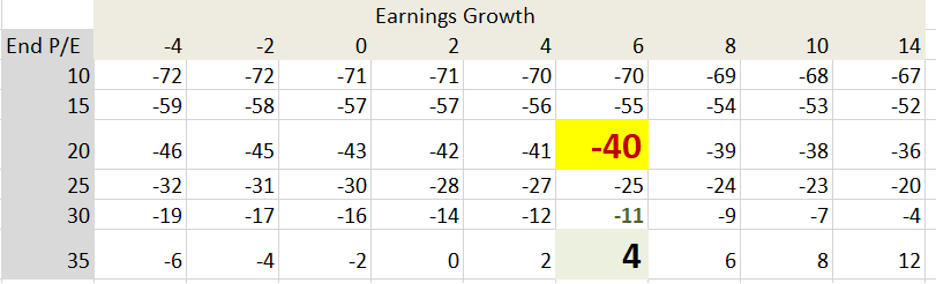

There’s a formula that explains stock returns

Return = Dividend Yield + (1 + Earnings Growth) X (1 + P/E expansion/contraction) – 1

The following table shows where we are now and highlights where we will be if P/Es revert to normal.

Stock return in 2022 mostly hinges on Price/Earnings (P/E) expansion or contraction. If multiples return to their historic average of 20, the stock market will decline by 40%. If multiples do not decline and remain at the current very elevated level of 35, the market will return 4%.

Investor psychology sets P/E. Investors are currently willing to pay a handsome premium for earnings. It’s a bubble., although it has not yet burst so it’s not yet official. Market swings of 2% up and down on a daily basis signal investor trepidation. Investors are scared, and they should be.

Protecting against losses

The usual move to defend is into cash, but current inflation threats change the game. The move to safety needs to be into inflation-protected assets like Treasury Inflation-Protected Securities (TIPs), commodities, real assets like real estate, and even cryptocurrencies. This unprecedented situation requires unprecedented reactions.

Defined benefit plan sponsors could match assets to liabilities so both would decline in tandem, maintaining funded status. Alternatively, sponsors could move to safety while the Fed is doing whatever it needs to, with the intention to match (diminished) liabilities when it’s all over. It’s complicated. Thanks, Ron!

A few Pension Facts

Fact 1: Managing a pension plan is NOT an easy endeavor. In fact, it is incredibly difficult. Forecasting the size of one’s future workforce, their longevity, salary and benefit increases, inflation, market returns, contributions, etc. can be as difficult an actuarial exercise as exists. The fact that we have so many Americans collecting a pension in retirement is a testament to a job well done – by most! But we can and should be doing better.

It is truly unfortunate that traditional private defined benefit pension (DB) plans have nearly disappeared. They are hanging on for dear life within the multiemployer and public pension arenas. Some of these systems are doing incredibly well, while others continue to struggle for a variety of reasons. As contribution expenses ratchet higher and higher, as we’ve witnessed for more than two decades, it is inevitable that these systems will begin to face a similar struggle as we’ve witnessed in the private sector.

Fact 2: The primary objective in managing a DB pension is to SECURE the promised benefits at both reasonable cost and with prudent risk. The primary objective is NOT achieving a return on asset assumption (ROA) that in many cases is nothing more than a Goldilocks # driven by what “feels good” from a contribution standpoint. Given the lack of consistency in our accounting standards, it is understandable why there is confusion. There should NOT be two ways to measure US pension plan liabilities, especially when one (under GASB) allows for the discount rate to be the ROA that doesn’t adjust with changes in the US interest rate environment. Incredibly, we’ve gone through a nearly 40-year bull market for bonds as interest rates have plummeted. Yet, this fact could easily have been lost on those valuing their plan’s liabilities based on GASB accounting. It was not lost on our private sector.

Fact 3: There exists a schism within our pension community that leads to the great disconnect between the primary pension objective and what we have today. The ability to actually manage pension assets to pension liabilities is made more challenging by the fact that most asset consultants don’t have any way to value a plan’s liabilities on a regular basis. I have been given an opportunity to participate in a program for the IFEBP in February. I will be presenting along with two very senior and more than capable asset consultants. I had raised a point with my co-presenters about needing to reflect on the very first page of a performance report on the relationship of plan assets to a plan’s specific liabilities. I wrote a post several years ago that asked that question. When I raised this concern with my co-presenters one of them asked a simple question: “Where am I supposed to get this information?” And, there lies the problem.

We have incredibly talented folks within the pension community, whether I’m speaking about the plan sponsor or the actuary, asset consultant(s), investment managers, legal counsel, etc. But there is a general lack of communication among all of these important constituents that are holding us back. We must find a way to bring all of the insights together on a more comprehensive and frequent basis. There should be no impediment for an asset consultant to have the proper insight into how that plan’s liabilities are performing. Furthermore, the development of the asset allocation should reflect the plan’s funded status, while also taking into consideration where we are likely to be going with regard to the capital markets than where we have been. Communication will be the key to pension funding success.

Most pension plans, thanks to their custodians, know the value of their public investments on a daily basis. They gain knowledge of their private investments with a bit of a delay, but they still have a general idea of what the total assets are. Unfortunately, most plan sponsors of multiemployer and public plans have little knowledge of the price movements of a plan’s liabilities, despite the fact that the “pension promise” is the only reason why a plan exists in the first place. The accounting rules certainly don’t help, but one can get around this issue by pricing liabilities using a FAS AA Corporate discount rate that would reflect a more accurate value for a liability stream and doing so on a much more frequent basis through the production of a Custom Liability Index (CLI).

Fact 4: Inappropriate decisions can and have been made based on the belief that pension liabilities and a plan’s funded status were X, when in fact they were very different, with liabilities being far larger and the funded status much weaker, as we’ve migrated through this unprecedented declining US interest rate environment. Having greater knowledge of the true economics of a pension system may have led to different conclusions. With greater transparency comes greater insight. We should all be working with the same information. Why is a market-based discount rate appropriate for private pensions, but not public? Please don’t tell me it is because public plans are “perpetual”. We’ve seen many examples of municipalities that have frozen and then terminated their DB pension plan – so much for perpetual!

Anyone who knows Ron Ryan and I understands that we are staunch supporters of defined benefit plans. Our mission is to secure the promises that have been made to plan participants. We want DB plans to remain the primary retirement vehicle for the masses. But the battle is far from won. Success will only happen if we all work together to manage these plans through a greater focus on the benefit promises (liabilities). Can you imagine playing a football game, but only knowing what your team has scored but not the opponent? How can you possibly adjust your offense and defense to reflect the current scoreboard situation? Regrettably, that is how many of us have been managing pension plans to date. A rising US interest rate environment could be very helpful to pension funding, as the present value of future liabilities will fall. Wouldn’t it be nice to know that fact? In an environment in which rates rise modestly the return on plan liabilities will likely be negative. You don’t need a 7.25% return to be successful. There is the fallacy! You need asset growth to match or exceed liability growth. You need asset cash flows to match and fund liability cash flows.

ARPA Update – Making Progress

It is the end of January 2022 and we still don’t have the PBGC’s Final Final Rules, but that doesn’t mean that we aren’t making some progress. According to the latest update from the PBGC’s website, there are now 24 pension plans that have filed applications to receive the Special Financial Assistance (SFA), including a second plan, Ironworkers Local 17 Pension Fund, that has been filed as an “MPRA eligibility suspension” claimant. In addition to the filing activity, we now know that five applications have been approved and two of those have actually received payment. Terrific!

I’ve expressed my concern that we have all this activity going on without final rules from the PBGC pertaining to implementation, but I’m told that there will be no changes to the law that necessitate a “clawback” of the SFA. That is great news. We can only hope that any amendments to the current interpretation leads to the ability of these plans to secure more of the promised benefits. With only 24 plans having filed to date, there is much more to come. We’ll keep you updated.

It’s The Opposite of Market Timing

No one’s crystal ball is any clearer than the next person’s. Sure, there are investors who are more disciplined, experienced, perhaps brighter, and luckier, but no one has a true knowledge of what awaits. Given this reality, market pros often, and correctly so, warn about trying to market time major moves within asset classes. Each of those decisions needs two right calls – the getting out and just as important, the getting back in – in order to capitalize. This ability is rare, and it can be expensive, as moving assets in the cash markets can have a high opportunity cost.

For years, we at Ryan ALM have encouraged plans to adopt an alpha/beta approach to managing pension assets for the reason that market timing is challenging, to say the least. Sure, we’ve been encouraging plan sponsors and their asset consultants a little more aggressively at this time to adopt our strategy but not because we have any greater clarity on the future direction of markets, but because we know from history that what goes up eventually goes back down. Pension plans are enjoying an improved funding position. As we’ve said, it would be sinful to see the great work/improvement wasted.

In proposing a new approach to asset allocation we are admitting that we have no idea about the future behavior of markets – bonds or equities. Using our Cash Flow Matching (CDI) approach creates an improved liquidity profile that will insulate the portfolio from having to liquidate alpha assets (non-bonds) during periods of turbulence. Furthermore, the alpha assets now have time to grow unencumbered while they potentially wade through rocky markets, such as the one we are in right now. Earlier this week we wrote about the 39-year bull market in bonds (began in 1982). Are we at the end of this extraordinary period of time? Who knows, but I like the bet that we are much more likely to see rates rise than fall further from these levels.

In a rising rate environment, total return-oriented bond products will likely suffer principal losses sufficient to produce a negative annual return. Given this possibility, use bonds for their cash flows and specifically to match asset cash flows with liability cash flows (benefit payments). In this case, assets and liabilities will be carefully matched (future values) producing a relationship that eliminates interest rate risk, which could be substantial during the next bear market.

Cash Flow Matching is a tried and true portfolio strategy that currently supports both lottery systems and insurance companies. It was once how pension plans were managed in the U.S. This “sleep well at night” strategy should be used at all times, as using bonds for liquidity purposes makes far greater sense than sweeping dividends from equity portfolios that could potentially reinvest those dividends at higher projected growth rates. You also don’t want to be searching for liquidity in an environment when everything correlates to 1 and liquidity disappears, such as that which we experienced in 2008. Don’t try to time the market. Adopt an all-weather strategy that will make your pension plan much more efficient to manage. Remember, the primary objective in managing a DB pension plan is to SECURE the promised benefits at both reasonable cost and with prudent risk.

Just over $1 billion

To date, the PBGC has approved the Special Financial Assistance (SFA) for 4 plans totaling just over $1 billion in grant money. The largest of these allocations was to Local 707 (1/19/22) which will receive $812.3 million. It remains the case that only Local 138 has received their payment. I guess that isn’t too problematic since we still haven’t been informed by the PBGC regarding their Final, Final Rules pertaining to the legislation’s implementation. As you may recall, we got the Interim Final Rules last July just before plans in Group 1 were permitted to file an application for the SFA.

Presently, any SFA grant money received must remain segregated from the plan’s legacy assets and they must be invested in investment-grade (IG) bonds. The intent of the legislation was to provide funds to SECURE the promised benefits (and expenses). Many industry practitioners have been prodding the PBGC to expand the investible universe to include other assets (and asset classes). We have cautioned that any movement away from a defeased portfolio using bond cash flows to match and fund pension liabilities opens the plan to greater volatility and potentially less security. Based on the current rules, most plans aren’t going to be able to secure more than 8-10 years of benefits. Why risk shortening this timeframe even more.

One need only look at the beginning of 2022 to be reminded that risk assets don’t only rise in value. The S&P 500 is off -9.2% YTD, while the R2000 is down -14%, while NASDAQ has fallen nearly -15%. The sequencing of returns is a critical element in a plan’s ability to meet its future obligations. It would have been a travesty had any one of these plans received their SFA only to have it decline by >-10% out of the gate after investing in assets other than IG bonds. Furthermore, who is to say that equity markets can’t correct more from these levels. We’ve certainly witnessed far greater declines in the past.

Oh, and by the way, I may be discussing the implementation of the SFA proceeds, but the same can be said about POB proceeds. This recent market action following the issuance of more POB $ since 2003 is why there are critics of POBs. We believe that both SFA and POB assets should be used to defease a plan’s liabilities chronologically as far out as the allocation will permit. No games! Secure the promises that have been made to your plan participants. Allow yourself and them to sleep well at night.

A New Day For Most!

I entered the pension/investment industry in October 1981. In fact, it was October 13, 1981, and the US 10-year Treasury was trading at a yield of 14.7% at that time. US interest rates have fallen steadily since then to the nearly historic levels at which they trade today. As the chart below reflects, rates trended higher for the 30-years prior to the 1981 peak and it has been mostly downhill since then. What a ride!

That said, you’d have to be in your early 60’s and at least a 40-year veteran to have experienced a bear market in bonds within the US. Sure, there have been brief periods when one’s mettle may have been tested, but the anguish and confusion brought on by a sustained bear market correction has been avoided by all but a few of us long-timers. It will be interesting to see how most market participants react.

For sponsors of pension plans, especially those in the public and multiemployer arenas, it will be challenging to see how they reconfigure the asset allocation to account for the likelihood of total return-oriented bond portfolios generating negative returns as rates rise. Achieving that ROA may become even more challenging. I specifically didn’t mention corporate plan sponsors because of two reasons: 1) they are exiting the pension game, and 2) they have their focus squarely on the plan’s liabilities to a far greater extent than those not swimming in the corporate pool – thanks to FASB. By adopting a greater focus on asset/liability management, corporate sponsors appreciate the fact that a cash flow matching bond portfolio’s interest-rate sensitivity is mitigated because assets and liabilities will move in lock-step with one another.

How much would rates have to back up to generate a negative total return? NOT MUCH! As the information below highlights, rates only have to back up by 25 bps, which could happen in a week, for bond programs as short as a 5-year duration strategy to have a negative annual return.

Price Return is determined by the duration of the bond

| Duration | YTM | +25 bps | +50 bps | |

| 5-Yr Treasury | 4.8 years | 1.19% | -1.20% | -2.40% |

| 5-yr A Corporate | 4.1 years | 1.63% | -1.03% | -2.05% |

| 10-Yr Treasury | 9.2 years | 1.40% | -2.30% | -4.60% |

| 10-yr A Corporate | 8.3 years | 2.26% | -2.08% | -4.15% |

| 30-Yr Treasury | 22.8 years | 1.81% | -5.70% | -11.40% |

| 30-yr A Corporate | 19.9 years | 2.87% | -4.98% | -9.95% |

Historically, US real interest rates have provided at least 1%-2% premium versus inflation. In today’s 7% inflation environment, real rates are trading at a negative 5% real return (30-year is at 2.12%). For how long will bond investors tolerate this situation? Given the lack of experience in managing through a bond bear market, it will be interesting to see the strategies that are adopted. One proven approach is to manage assets versus liabilities through a cash flow matching (CDI) strategy. Because asset cash flows are matched against liability cash flows, which are future values, interest rate risk has been eliminated. There is no more important risk to manage in bond land than interest rate risk. We’d be happy to share our insights with you. We’ve all enjoyed this incredible bull market, but after 39 great years, I believe that the party is over. The hangover that we experience may need more than a couple of Advil to cure!

The Ryan ALM Q4’21 Newsletter

We are pleased to share with you the Ryan ALM Q4’21 Newsletter. This newsletter highlights the relationship of pension assets to liabilities, which we believe is the most important metric. As you will read, calendar year 2021 was a strong year for Pension America as assets dramatically outperformed liability growth. Now what? Will you rethink the traditional approach to asset allocation or will the whims of the markets impact your plan’s funded status and contribution expenses. Will pension plans respond to their improved funded status and de-risk some of the assets? We believe that the primary objective in managing a pension plan is to secure the promised benefits at a reasonable cost and with prudent risk. Are your promised benefits secure? We’d welcome the opportunity to share our thoughts and expertise with you.

Pension America – What a Year!

Great year – what now? Are we just going to allow the markets to whipsaw funded status and contribution expenses?

Should You Buy Downside Protection?

At the time of writing, equity markets seemed to have stabilized a bit today following a rough start to 2022. It isn’t surprising that markets have been soft to start the year given current market valuations following a nearly unprecedented run-up in stock prices. That said, are we looking at a brief pause in the upward trajectory of stocks or perhaps something more sinister that was witnessed twice during the ’00s and many times before? A reasonable question for investors is whether they should “insure” against downside risk in equity markets. However, current option prices suggest that such insurance strategies are quite expensive, especially relative to history. Why? One of the factors influencing the pricing of insurance is the plethora of macro events such as interest rates, economic growth, Covid-19, geopolitical risk (Russia/China), etc.

If buying traditional equity market insurance is too expensive, there is another way to protect your flank that might just minimize risk on a couple of fronts – liquidity and interest rates – if not the equity markets themselves. I am referring to the use of a cash flow matching strategy (CDI) that would be used in lieu of a traditional fixed income total return approach. If US rates continue to rise, not only will they likely destabilize equity markets, but total return-oriented fixed income portfolios will likely produce negative returns for the foreseeable future. We’d suggest using bonds for their cash flows carefully matched against the plan’s specific liabilities that will eliminate interest rate risk, as we will be matching future values that are not interest-rate sensitive, while dramatically improving the plan’s liquidity profile.

So where does the downside risk for stocks come in? Well, if we deconstruct the current approach to asset allocation that uses all the assets focused on a return on asset assumption (ROA) to one that uses a bifurcated approach separating liquidity (beta) and growth (alpha) assets we can provide a unique form of downside protection at a minimal cost. The beta assets are the cash flow matching bonds carefully allocated to maximize the cash flows (principal, income, and reinvested income) to meet benefits and expenses, while the alpha assets are the plan’s growth assets that will eventually meet future liabilities. In this construct, the alpha assets can grow unencumbered as they are no longer a source of liquidity. We’ve now bought time for these assets to recover should markets get hit. Furthermore, the reinvestment of dividend income is critical to the long-term growth of equities. One study, in particular, suggests that 48% of the return of the S&P 500 over rolling 10-year periods is attributable to the reinvestment of dividends. Extending that analysis to rolling 20-year periods finds an incredible 60% of the total return comes from dividends reinvested.

With the Ryan ALM approach, plan sponsors won’t need or be tempted to take dividend income to use for benefit payments. It isn’t necessary now that the CDI portfolio is responsible for funding the promised benefits and expenses. Traditional downside risk protection can be complicated and expensive. Adopting our approach is just common sense.