Every once in a while you come across an article that just strikes a chord with you. I’m pleased to know Ron Surz, who is as passionate about trying to help our retirement industry as I am. The following article has been produced by Ron who has been elevating his concerns for years regarding traditional target-date funds. Given the fact that most of us only have access to a DC plan, coupled with current market levels, there is an urgency in his message that should be heeded. I hope that you find Ron’s insights compelling.

Most assets suffered losses at the start of the year 2022. Only commodities were spared as inflation, and inflation fears drove up their prices. Consequently, your 401(k) investments lost value. Target date funds of all vintages declined but — no surprise — safer TDFs defended. The “TO – THROUGH” TDF label is a distinction without a difference. “SAFE or RISKY” is much more meaningful. Defined benefit plans also suffered losses like 2040 TDFs since these roughly match DB allocations.

Legend has it that January performance predicts the performance for the year. There’s reason to believe that there’s more to come in 2022.

There is more to come

We enter 2022 with a host of economic threats:

- COVID

- Inflation

- Stock market bubble

- Bond price manipulation (ZIRP)

- Unprecedented money printing

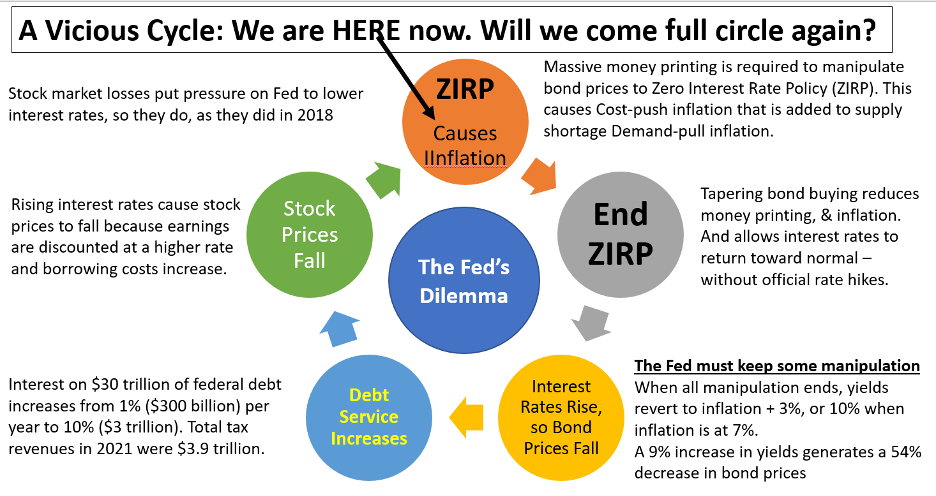

The Federal Reserve has tried to calm the investing public with a promise to control inflation, but this will not be easy. The Fed is caught in a cycle that will be hard to break. If it raises interest rates, stock and bond prices will fall. In a repeat of 2018, the Fed will be pressured to reverse course and try to jam interest rates back toward zero.

But 2022 is not like 2018 because we have serious inflation in 2022 at 7% and threatening to go higher. This time implementing a zero interest rate policy (ZIRP) will fuel the current inflation fire because it requires massive money printing. The Fed can’t have it both ways. It cannot control inflation and continue to buoy up stock and bond prices.

Current inflation is a combination of demand-pull due to supply shortages and cost-push due to $13 trillion in money printing, which is more than our 10 most expensive wars. It is not transitory.

A prediction

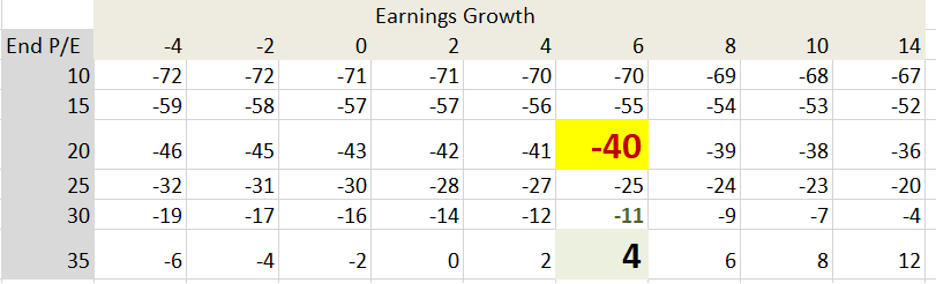

There’s a formula that explains stock returns

Return = Dividend Yield + (1 + Earnings Growth) X (1 + P/E expansion/contraction) – 1

The following table shows where we are now and highlights where we will be if P/Es revert to normal.

Stock return in 2022 mostly hinges on Price/Earnings (P/E) expansion or contraction. If multiples return to their historic average of 20, the stock market will decline by 40%. If multiples do not decline and remain at the current very elevated level of 35, the market will return 4%.

Investor psychology sets P/E. Investors are currently willing to pay a handsome premium for earnings. It’s a bubble., although it has not yet burst so it’s not yet official. Market swings of 2% up and down on a daily basis signal investor trepidation. Investors are scared, and they should be.

Protecting against losses

The usual move to defend is into cash, but current inflation threats change the game. The move to safety needs to be into inflation-protected assets like Treasury Inflation-Protected Securities (TIPs), commodities, real assets like real estate, and even cryptocurrencies. This unprecedented situation requires unprecedented reactions.

Defined benefit plan sponsors could match assets to liabilities so both would decline in tandem, maintaining funded status. Alternatively, sponsors could move to safety while the Fed is doing whatever it needs to, with the intention to match (diminished) liabilities when it’s all over. It’s complicated. Thanks, Ron!