By: Russ Kamp, Managing Director, Ryan ALM, Inc.

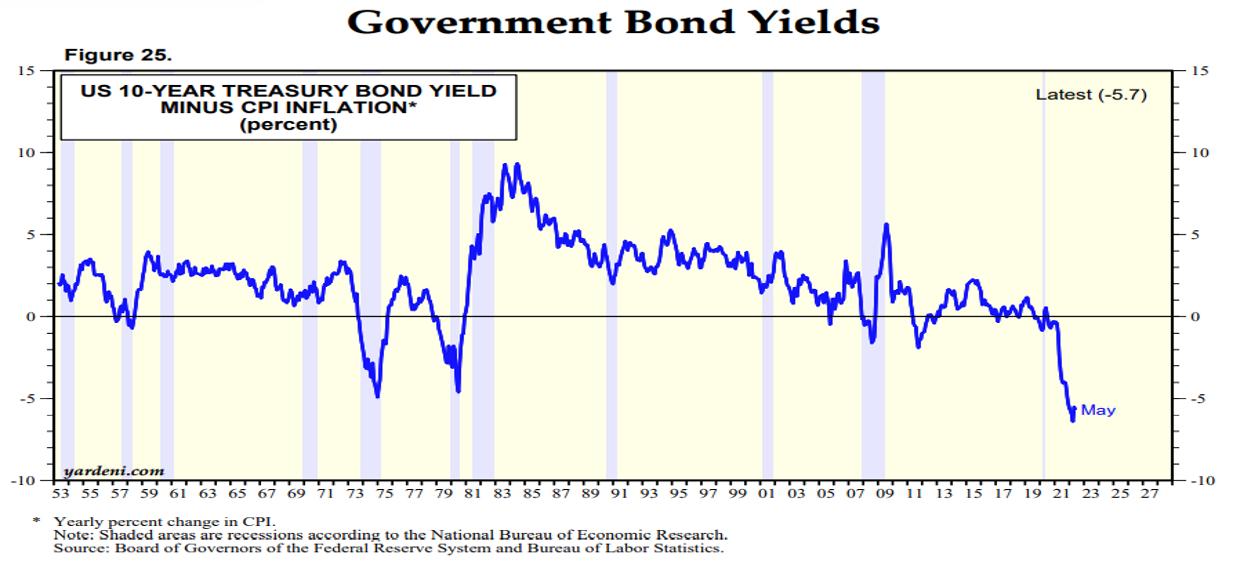

Following the publication of yesterday’s post, I received several good questions including the following: “Have real interest rates (nominal rate minus inflation) ever been below -5%, let alone the current -7%?” It is a terrific question and one that should be on the minds of all investors. The simple and not surprising answer is not since at least 1953. We came close during the turbulent ’70s, but nothing to this extreme. With the most recent rally in Treasuries, the real rate for the US 10-year Treasury Note is – 6.22% as of 8:20 am on August 3, 2022.

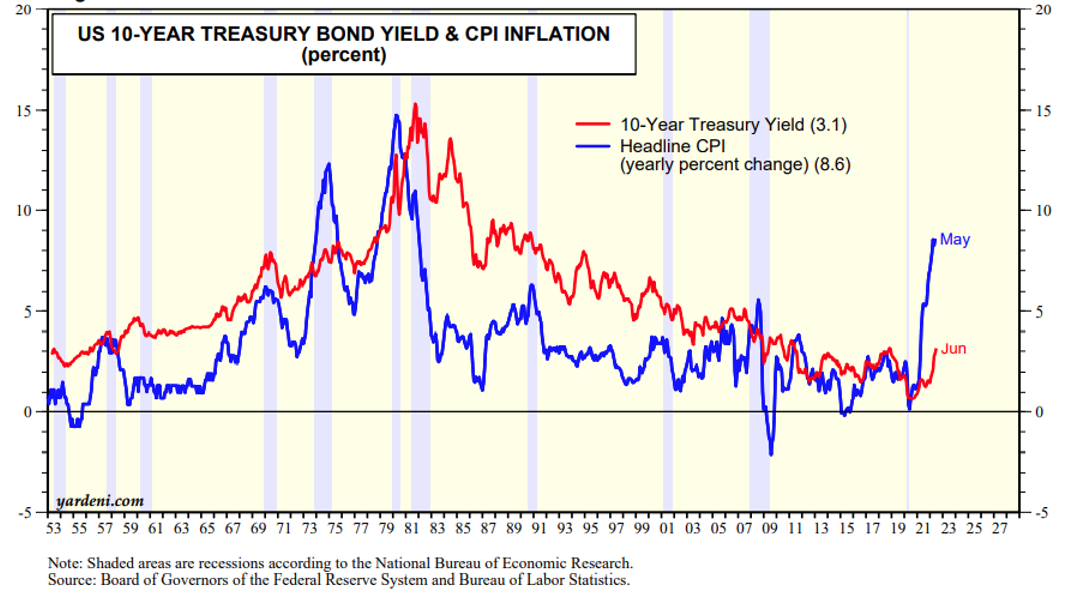

It makes no sense to me and many others why the investment community continues to accept such a ridiculously low return on US government bonds given the inflationary environment that won’t likely collapse as quickly as it rose. Again, my premise is that 4 decades of falling US interest rates that culminated in historically low rates associated with the Covid-19 crisis have clouded our judgment and anchored us to believe that interest rates will remain low forever and ever. All one needs to do is look at the yield on the US 10-year Treasury Note for the 30 years prior to 1982.

One should also note that US rates kept rising into 1982 despite the fact that inflation peaked in 1980. Again, investors thinking that the US Fed has already accomplished its objective in curbing inflation by increasing the Fed Funds Rate to 2.25% – 2.5% are just kidding themselves. These rates remain near historic lows and likely remain stimulative to economic growth. Couple that fact with full employment and strong wage growth and it remains highly unlikely that the investment community will get their Christmas gift of a Fed providing easing early in 2023. As always, we encourage your questions and look forward to engaging with you in the near future.