By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Another day of jobs data and another sell-off in the market by participants hoping for some sign that the US Federal Reserve will be forced to pivot away from its crusade to thwart decades-high inflation. Guess what? It isn’t going to happen – sorry. Once again, we’ve had an employment report that came in at roughly forecasted expectations (263k vs. 275k). In the process, the unemployment rate fell from 3.7% to 3.5%. Earlier this week I produced a post titled, “What Has the Fed Accomplished?”, in which I questioned what had changed from last week, month, quarter, or year-to-date, that would have had equity and bond markets rallying significantly to begin this week.

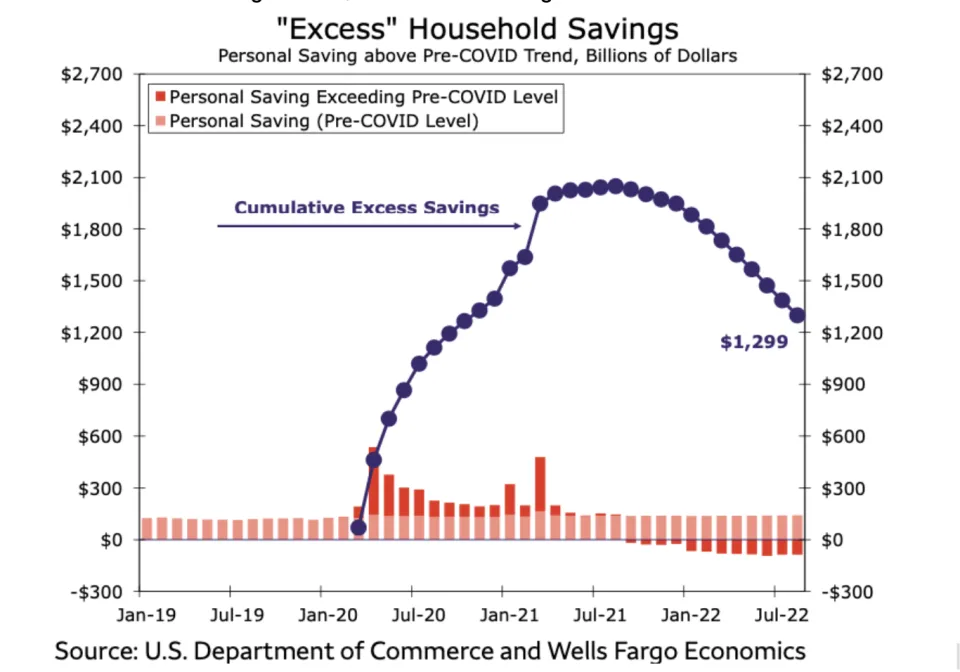

We continue to see a historically strong employment picture in which wages are growing, albeit by a lesser amount than inflation. Furthermore, there is still “excess” savings (estimated at $1.2 trillion) as a result of the incredible stimulus provided during the peak of the Covid-19 pandemic. Many US consumers are flush despite the inflationary impact. We will continue to witness strong demand until the employment picture is significantly altered. That clearly hasn’t happened yet. Yes, initial jobless claims were higher than last week and job openings fell relative to previous releases, but in neither case were they substantial enough to change the minds of Fed governors, who continue to sing from the same hymnal.

If 4.625% is the target for the Fed Fund’s Rate at some point in 2023, there is a lot more pain to be realized in traditional fixed income and equity allocations. Sitting back and letting this scenario unfold is not prudent. Yes, we’ve seen markets come back from the depths before, but in every case during the last four decades, we had an accommodative Fed to help prop up risk assets. They aren’t in a position to do that this time. Convert your current fixed income exposure from a return-seeking mandate to a cash flow matching strategy that will fund promised benefits, improve liquidity, and mitigate interest rate risk for that portion of the account, while buying time for equities and other alpha-generating assets to grow unencumbered. Plan sponsors and their advisors can continue to hope that the Fed was only kidding, or they can act to limit the damage already inflicted in 2022 before it gets much worse as we move into 2023.