By: Russ Kamp, Managing Director, Ryan ALM, Inc.

We are pleased to be able to provide you with this ARPA update through April 14, 2023. I am able to provide these summaries of the week’s activity for you thanks to the PBGC which continues to provide its weekly update. As we’ve recently reported, the general level of activity has slowed. To that point, there were no new applications accepted by the PBGC in the latest week. In addition, there were no applications for SFA (initial or supplemental) that were approved, denied, or paid out.

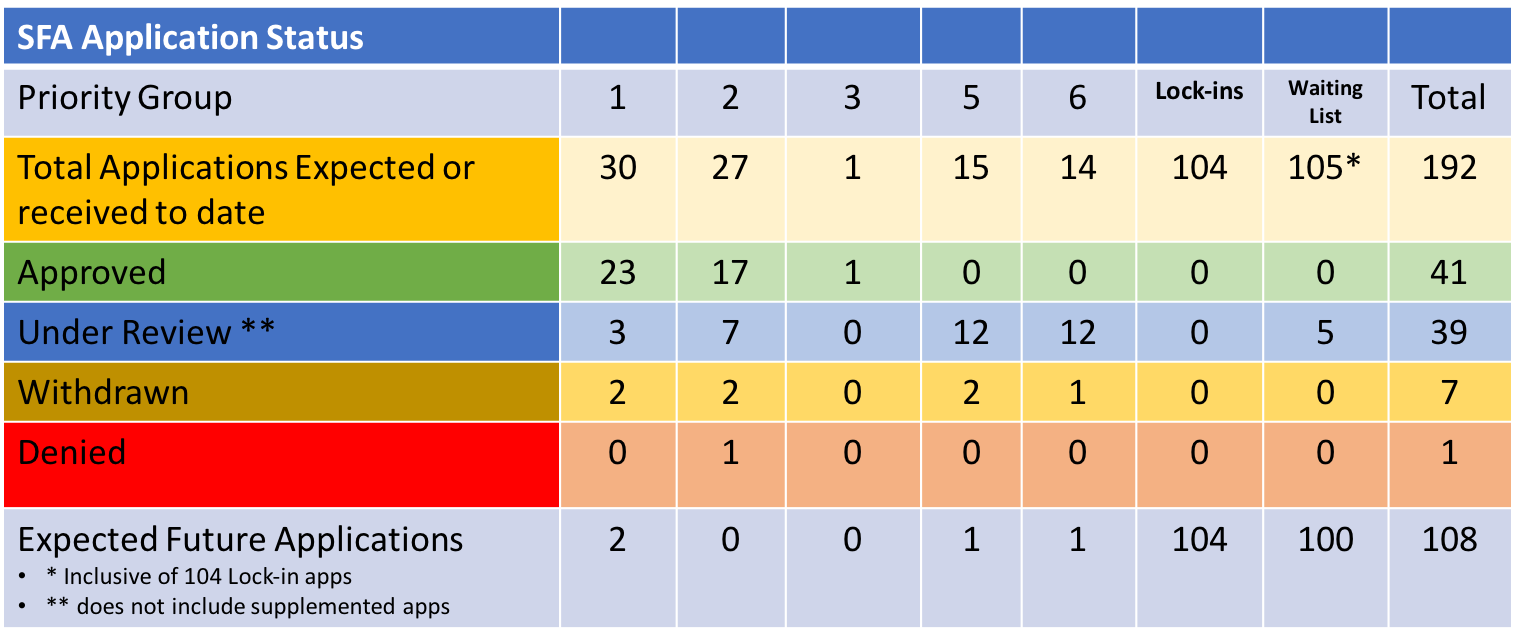

There was, however, one pension fund, the International Association of Bridge, Structural, Ornamental & Reinforcing Ironworkers L.U. No. 79 Pension Fund, which was placed on the waiting list. There are 105 non-priority plans (Groups 1-6) that made it to the waiting list. Of those 105, five applications are currently being reviewed by the PBGC. They’ve indicated that they will open the e-filing portal at a pace that allows for an orderly review to be completed on each application within the legislation’s 120-day window.

It will be interesting to see if the pace of activity can be increased given that more than 140 applications are left to review before other pension funds are possibly added to the waitlist. Remember, it was estimated by the PBGC that as many as 218 non-priority plans could potentially file. We’ve seen fewer than half of those get placed on the waiting list at this time. Lastly, of all the plans that have locked in a valuation date, there remains only one with a January 31, 2023 date. All of the others have chosen 12/31/22.