There are many deniers within the U.S. retirement system that would have you believe that there isn’t a retirement crisis unfolding. The demise of the defined benefit plan has been most notable within the private sector, but multiemployer and public pension plans are certainly not immune to the problem, and the situation is likely to get worse before too long.

Let’s just take a look at the current environment within the multiemployer landscape:

- 130 multiemployer plans projected to be insolvent over the next 20 years (there are roughly 1,300 plans)

- 200 additional plans in PPA critical status (<65% funded)

- 3.5 million plan participants with pension benefits at risk

- PBGC financial exposure to multiemployer plans at $65 billion as of 2017

- PBGC multiemployer insurance program projected to be insolvent in 2025

- Even with a solvent PBGC their maximum guaranteed benefit still results in major benefit cuts to participants

- Multiemployer Pension Reform Act of 2014 (MPRA) has failed to arrest the multiemployer funding crisis

This situation is deeply concerning, but not impossible to overcome if we act now. As we’ve discussed on many occasions within this blog, Federal legislation (The Butch Lewis Act) is being considered that would provide low-interest loans to “Critical and Declining” status plans that would help protect the promised pension benefits for the millions of plan participants. Our failure to act will create profoundly negative social and economic implications. This legislation needs to be enacted.

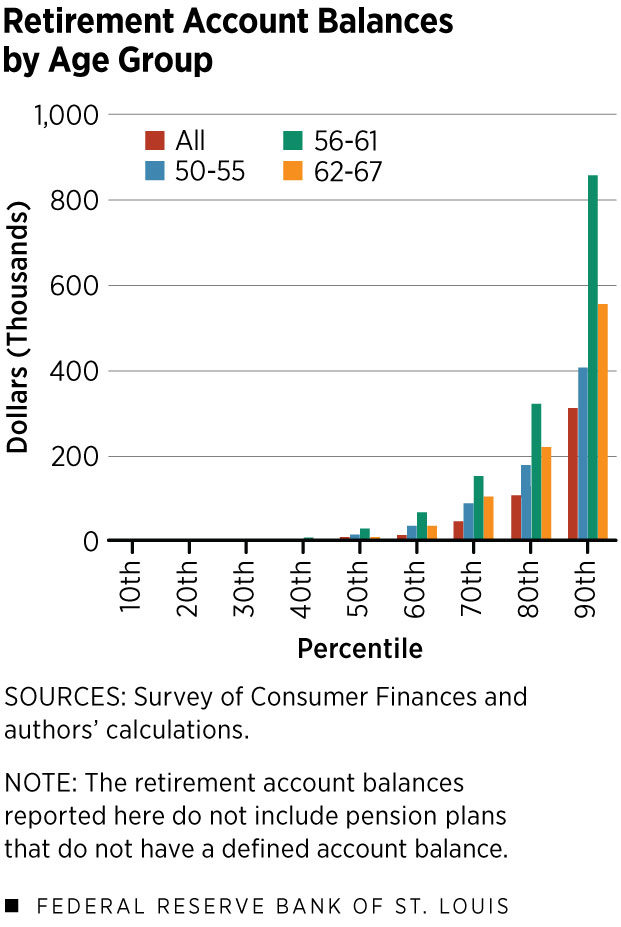

As one can clearly see, no near-retirement income group is in great shape when it comes to funding a retirement account, but the bottom 50% of older income earners are in terrible shape.

As one can clearly see, no near-retirement income group is in great shape when it comes to funding a retirement account, but the bottom 50% of older income earners are in terrible shape.