I’ve been as much a critic of the PBGC’s Interim Final Results (IFR) as anyone. I was disheartened by how the PBGC decided that the Special Financial Assistance (SFA) should be calculated. That said, struggling multiemployer pension systems are still getting new found money that will enhance the funded status. Although the amount of the grant may be less than what was originally expected or intended by Congress through this legislative effort, we at Ryan ALM have determined that this SFA program can achieve success, but it very much depends on how the SFA and legacy assets are invested.

Many folks, including me, have been focused on the disconnect between the discount rate of 5.5% (3rd segment + 200 bps) and the potential yield (roughly 2%) from investment grade bonds within the SFA. This difference does create a funding gap between the cost to fund benefits and expenses for 30-years and the amount received, but it isn’t fatal. Many comments received by the PBGC during the 30-day comment period focused on the appropriateness of mandating a very conservative investment grade bond portfolio while this gap exists. But we believe that securing the SFA assets is paramount, while mirroring the intent of Congress.

A leading actuarial firm with a particular expertise in multiemployer plans provided us with an example of a hypothetical pension fund that would qualify to receive an ARPA grant based on the characteristics of this plan’s profile. In their example, the “client” had $100 million in beginning assets and liabilities of $256.6 million in liabilities discounted at 5.5% for a funding deficit of ($156.6 million). The funded ratio was only 39.0%. Based on the PBGC’s SFA calculation, this plan would be eligible for $180.7 million in Special Financial Assistance, which is forecast to be received in 2024 when the current assets will have declined to $63.4 million. Furthermore, they estimated a 2% return on SFA assets and a 6.75% return on legacy assets. Given these expectations the plan would likely be in a $28.1 million deficit by 2052 supporting the calls for changes to either the legislation or the PBGC’s guidelines or both.

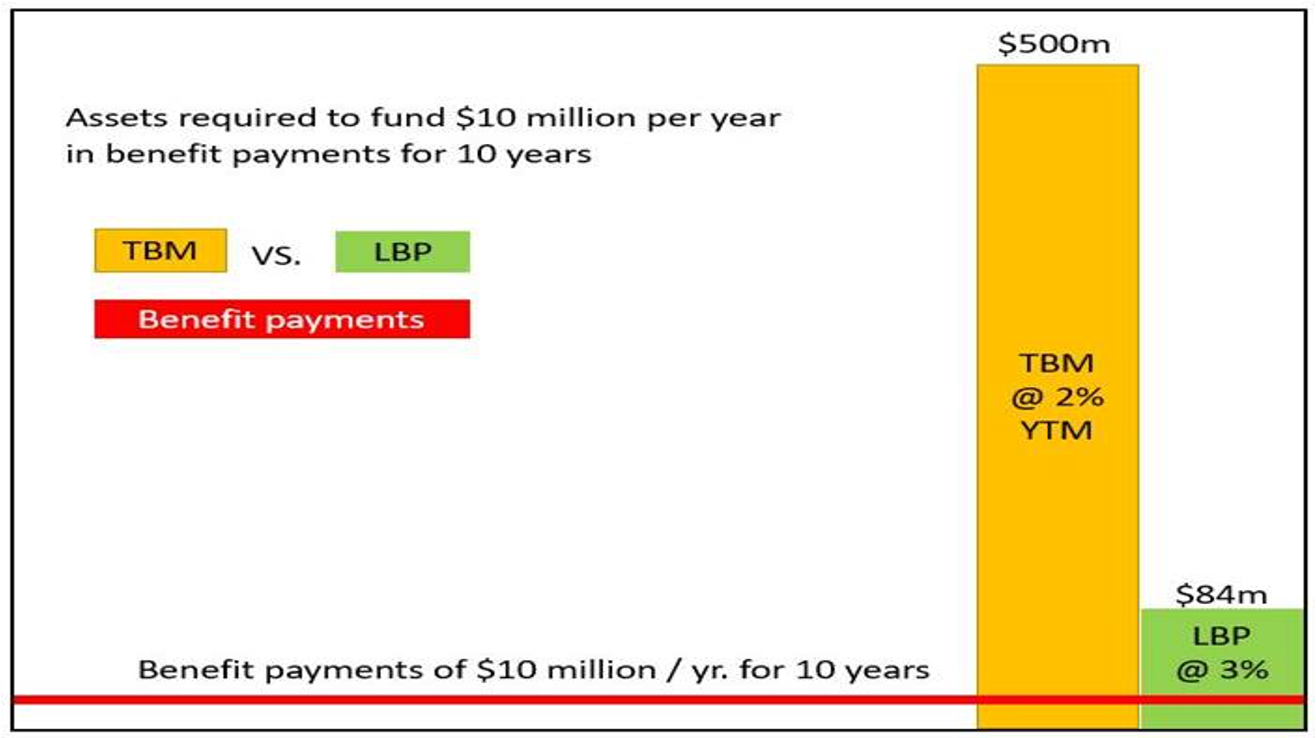

Here’s the good news. Despite the appearance of a funding gap because the discount rate is much greater than the potential return on investment grade bonds, funding of benefits and expenses is a function of the SFA and legacy assets working in harmony. Ryan ALM is proposing that the SFA assets defease as many of the liabilities as possible once the grant is received (2024 in our example). By defeasing the promised benefits and expenses within the SFA bucket until those assets are exhausted, our approach fulfills the goal of Congress to “secure” benefits. Furthermore, the legacy assets and future contributions can now be managed with a slightly more aggressive risk profile as they aren’t needed for cash flow for the eight years from 2024 to 2031 that the SFA assets defease liabilities. Importantly, bonds are no longer needed within the legacy asset allocation. Rotating away from bonds to more equity-like products will increase the potential ROA from the existing legacy portfolio.

We have modeled a number of scenarios by tweaking the actuarial firm’s expected return on the SFA and legacy assets. For instance, an investment grade corporate bond portfolio used to defease the plan’s liabilities will provide a return somewhere in the area of 2.5% to 3% narrowing the gap to the discount rate and not the 2% used in the original scenario. Because we have eliminated bonds from our legacy assets during the 2024-2031 period in which we only use the SFA to pay benefits and expenses, the legacy portfolio should be able to achieve a return greater than the 6.75% used to calculate the SFA. In the scenario that we feel is most reasonable, we used a 2.5% return on the SFA, the 6.75% for the first three years (2021-2024), a 7.5% ROA for the legacy assets from 2024 to 2031, and a very modest 7.15% return from 2032 to 2051.

In this scenario, we are able to fully fund all future benefits and expenses for 30 years, while beginning 2052 with $77.4 million in assets to meet future liabilities. The other scenarios that we modeled used similar inputs and produced results in every case that had 2052 beginning with at least $42.6 million in assets available to meet future liabilities. I think that our inputs are extremely reasonable given the 30-year investing horizon. Furthermore, we have not had to dramatically increase risk in the legacy portfolio or the SFA portfolio to achieve these terrific results. Again, it is unfortunate that the calculation to determine the SFA was so conservative, but at the end of the day the grant money goes a long way to helping secure the promised benefits for plan participants, many who have endured tragic cuts for several years now. How the SFA assets are implemented is crucial to this program’s success. Having the SFA and the legacy assets working in harmony to achieve these positive results is critical. It is imperative that the SFGA assets stay true to their objective of defeasing and funding benefits and expenses for as far out as possible. This requires a cash flow matching strategy with fixed income. To be clear, matching the 5.50% discount rate is NOT the objective of the SFA assets.

Lastly, I read a comment on the PBGC website that claimed that the legacy assets would need to achieve a 12%+ return in order for all the benefits and expenses to be paid. Nonsense! We have shown that a 39% funded plan (prior to getting the SFA) can achieve success even with a 7.5% return on legacy assets combined with only a 2.5% return on SFA assets. We’re happy to share our analysis with you. Don’t hesitate to reach out.