There recently appeared an article in FundFire that suggested that plan sponsors, particularly corporate sponsors, were using their allocation to fixed income inefficiently. We absolutely agree! However, we find that the suggested implementation cited in that article to be just wrong. The article stated that corporate pension plans had roughly 40% in fixed income, which a consultant from a leading firm said was too much. Again, we agree. This consultant went on to say that plans should use US Treasury STRIPS in lieu of coupon bonds, which would allow them to put far fewer $s to work. This is incorrect math and needs to be tested. The pension objective is all about cash flows… asset cash flows versus liability cash flows.

US Treasury STRIPS are highly volatile and expensive. They performed well during the bond market’s lengthy bull market (since 1982), because they have longer durations than coupon bonds. Since we are near historic lows in interest rates now a trend toward higher interest rates (which most economists predict) would produce an opposite effect. Moreover, STRIPS do not secure benefit payments, as they have been stripped of their income component and they certainly are not low risk.

Does it really make sense to use STRIPS now? We would also suggest that the true pension plan objective is too “secure” the promised benefits in a cost efficient manner with prudent risk. This is best accomplished through cash flow matching liabilities with coupon bonds. The difference in cost versus STRIPS could be close to 1% per year of liabilities (a 25-year benefit payment schedule = 25% cost savings). The higher the funded ratio the more the plan sponsor should allocate to defeasance through fixed income securities. We recommend that Retired Lives should be defeased as much as possible since they are the most certain, imminent, and important liabilities.

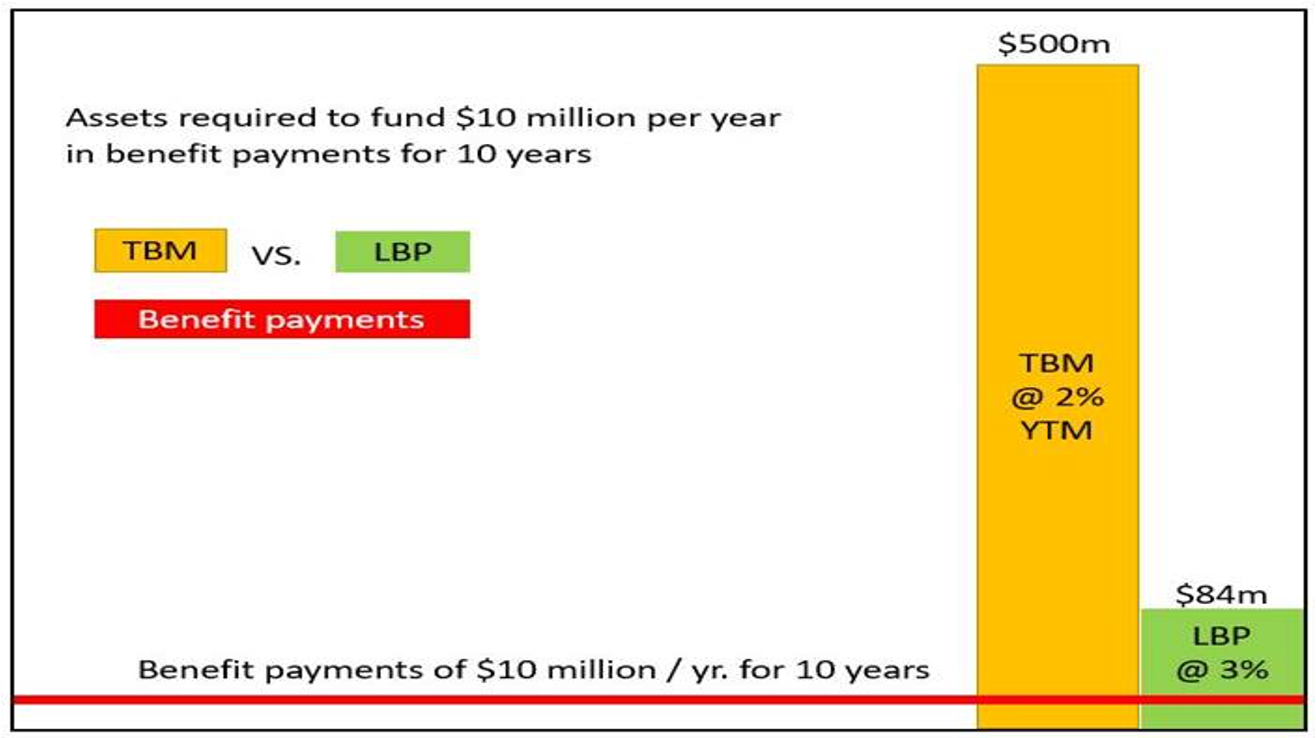

Do you want to improve the efficiency of your asset allocation? Would you like to put fewer assets into fixed income in this low-interest-rate environment? Adopting a cash flow driven investing (CDI) approach will accomplish your objectives. As the example below reflects, traditional bond management (TBM) requires an allocation of $500 million to fund $10 million in annual benefit payments in this 2% interest rate environment. This is very inefficient. By adopting a CDI approach, the fund can accomplish the objective of funding $10 million in benefit payments with ONLY $84 million. The additional $416 million can now be used in other asset classes to support alpha generation.

The allocation to fixed income is now 83.2% less than using a traditional bond manager. In a CDI implementation the $10 million in benefits is achieved through the use of principal, income, and reinvested income. In addition, bond math suggests that the longer the maturity and the higher the yield the lower the cost. Our cash flow matching process is a cost optimization model that will take advantage of both of these mathematical principles by biasing our portfolio to longer maturities. Thereby we can partially fund the next nine years of benefit payments with the income from a 10-year maturity at 3% yield versus a 1-year Bill providing the investor with 7 basis points and lower yields for the 1-9 year benefit payments.

A CDI strategy is the most cost efficient implementation in accomplishing the primary objective of securing the pension system’s promised benefits. Only an insurance company annuity can provide the same certainty of securing benefits, but at a much higher cost (@ 4% premium). We agree that pension plans should get smarter about the asset allocation that they adopt. It needs to be driven by the funded status and not the return on assets assumption. If plans were to start doing this, I don’t believe that there would be any debate as to how plans would approach their fixed income allocation.

My question is that are the investments that the Treasury insists the SFA money is invested too conservative? 2nd Why don’t they converse with people like your selves for investment advice?

Good morning, Joe. I hope that you are well today. If the intent of Congress was to have the benefit payments and the expenses secured, then the insistence on investment grade bonds as the investment of choice is not inappropriate. I, like everyone else, was focused on the disconnect between the return from IGBs and the discount rate, but the whole portfolio, including the legacy assets, must be taken into consideration when determining whether or not this program will work. The Ryan ALM team is confident that we can make this program work, but it depends on the implementation. WIth regard to your second question, they have access to everyone and only have to ask. I suspect that the motivating factor for this legislation was based on the size of the program – now estimaated to be $94 billion.

Pingback: It’s all about Pension Math… and it Doesn’t Lie! – Ryan ALM Blog