By: Russ Kamp, Managing Director, Ryan ALM, Inc.

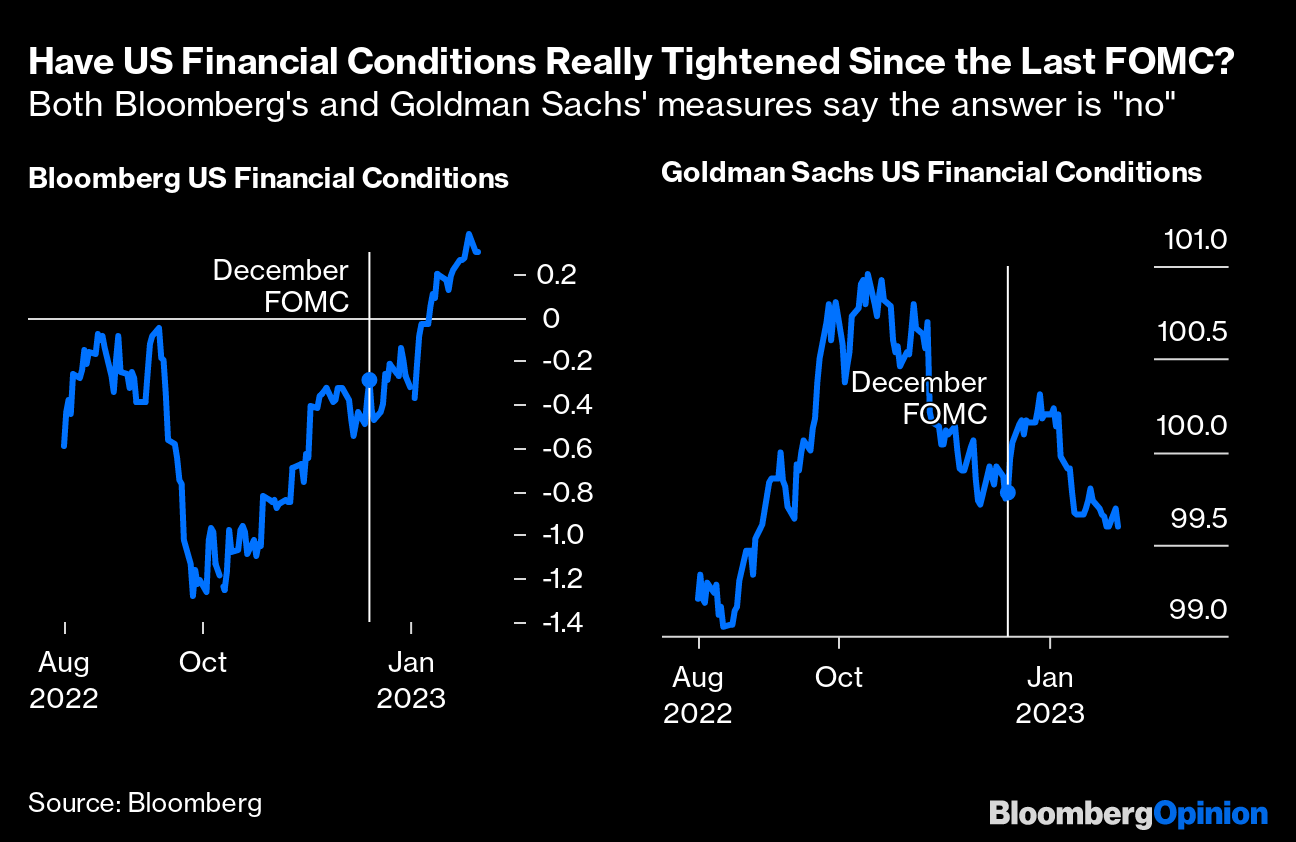

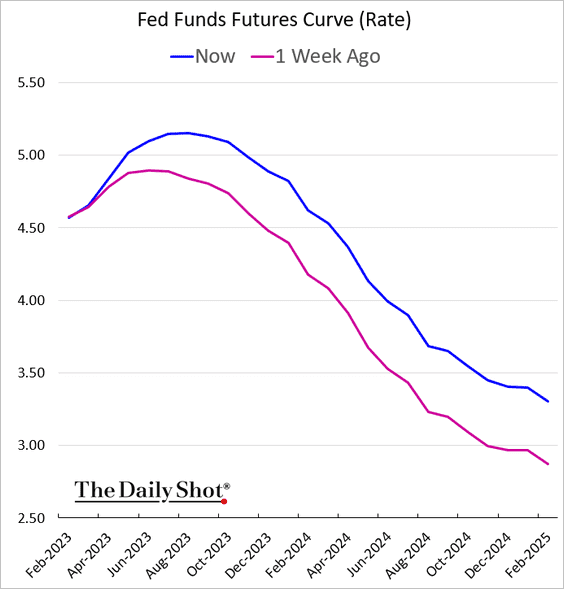

Could it be that the investing community is finally waking up to the fact that the US Federal Reserve is serious about combating inflation by raising the Fed Funds Rate well above the recent consensus? (see graph below) How many times do we need to hear Fed Governors mention that a great pivot is NOT about to happen in 2023? I’ve heard members of the FOMC indicate that the target FFR is 5.4% or higher. Why hasn’t that resonated with investors? I read just today that some members are even talking about 6% on the FFR. What a shock that must be to those investors that have just been hitting snooze on their alarm clock in anticipation that a little more sleep will help them get through their nightmare. Well, it is time to stop hitting snooze and wake up to the fact that inflation will not be eradicated anytime soon. The Fed mantra remains higher for longer.

Don’t panic plan sponsors of pension plans. Rising US interest rates are a positive development for your plans in terms of both liabilities and assets! With regard to your liabilities (promised benefits), rising rates reduce the present value (PV) of those future value (FV) benefit payments (and expenses). Those operating in the private sector certainly appreciate that fact as they are obligated to use market rates (ASC 715 discount rates) to value a plan’s liabilities. Unfortunately, the public pension ignores market rates and uses the ROA as its discount rate which is always a fairly steady positive growth rate.

With regard to the impact on the asset side, 2022 was a challenging year for most pension plans. But with rates rising, corporate bond portfolios are producing yields in excess of 5%-5.5%, which gets a plan fairly close to the target ROA with much less volatility than a traditional asset allocation. Furthermore, bonds are not a performance instrument in a rising rate environment, but they are a great source of cash flow (liquidity) to fund required benefits and expenses (liabilities). Use bonds to create a cash flow matching portfolio that defeases benefits and expenses chronologically from next month as far out as your bond allocation can go. The benefits are enormous. We explain all of them in various blog posts and research (White Papers) that can be found at Ryanalm.com. We are here to answer any of your questions. Please don’t hesitate to reach out to us.