By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Maybe things have changed during the last 40 years (my hair color certainly has), but there seems to be a major disconnect between the market’s (Fed’s) reaction to the early 1980s inflationary environment compared to the one that we are currently experiencing. Perhaps it is 40 years of falling rates and accommodative Fed policy that have created an expectation that rates will remain low forever, and that the Fed’s only responsibility is to prop up markets at the first sign of trouble. It may be challenging for those engaged in the investment community today that weren’t working in the industry 40 years ago to truly appreciate the actions taken by Paul Volcker and his team to combat historic inflation.

| Economic Indicators | 1981 | 2022 |

| CPI | 8.9 | 7.7 |

| Unemployment Rate | 8.5 | 3.7 |

| GDP | 2.5 | 2.9 |

As the data above suggests, inflation today is not too dissimilar to that which we were experiencing in 1981. Sure, inflation has begun to fall from higher levels this past Summer, but it was substantially higher in 1980, too. GDP growth in 1981 compared to today was quite similar. The biggest difference has to do with the current labor market versus 1981, and this is what today’s Fed is focused on. We are near full employment and wages are growing at around 5% annually. The Fed doesn’t believe that inflation can be tamed to any great extent unless we begin to see weakness within the US labor force. Despite aggressive (?) Fed action throughout 2022, unemployment remains stubbornly low. What gives?

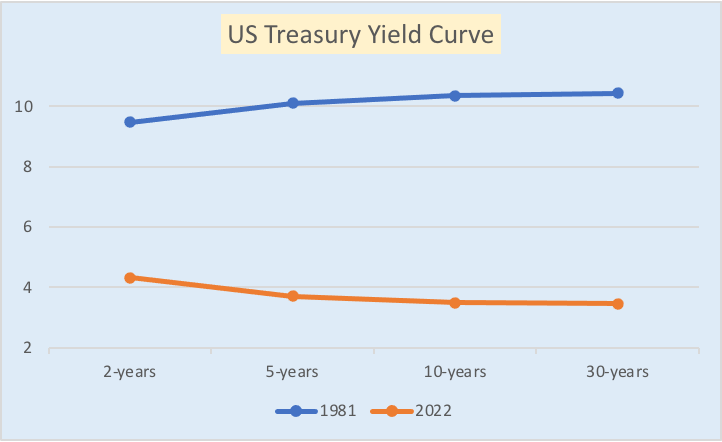

The graph above highlights the US Treasury yield curve for 1981 and 2022. Given similar inflation and GDP data, one would think that US interest rates would be occupying similar levels. But that is far from the case. Market participants today feel that rates have peaked given that inflation appears to be moderating. However, that doesn’t mean that the Fed won’t continue to raise rates in order to achieve a level of “real” rates, which is exactly what Volcker did in the early ’80s. It wasn’t until US interest rates were elevated to a level substantially above the prevailing inflation rate that inflation was finally tamed. Given today’s CPI of 7.7% applying a historic inflation premium (real rate) of 3.1% would push rates above 10% and place them very close to where they were at the end of 1981. Even if inflation fell to 3%, real rates should be at 5% to 6% with an inflation premium of 2% to 3%.

I don’t understand why investors today feel that rates are high. On a relative basis, US Treasuries are well below the long-term average and substantially below inflation. If fighting inflation is the Fed’s primary focus, then they have much work ahead of them. Increasing the Fed Fund’s rate by 50 bps instead of 75 bps is still an increase. Do that another 5-6 times and you’ll finally get rates to a level commensurate with today’s inflation. The Fed pivot doesn’t seem to reflect reality. We can all hope, but hope has never been a successful investment strategy.