By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Managing a pension plan is not an easy task, but it doesn’t have to be as challenging as it currently seems to be. Why? For one thing, pension plans need to understand that they only exist to fund a promise that has been made to the plan participants. That promise – future benefit payments – needs to be measured, monitored, managed to, and then SECURED. But, without a means to do that on a frequent basis (daily, weekly, monthly, and/or quarterly) how does one actually accomplish the objective?

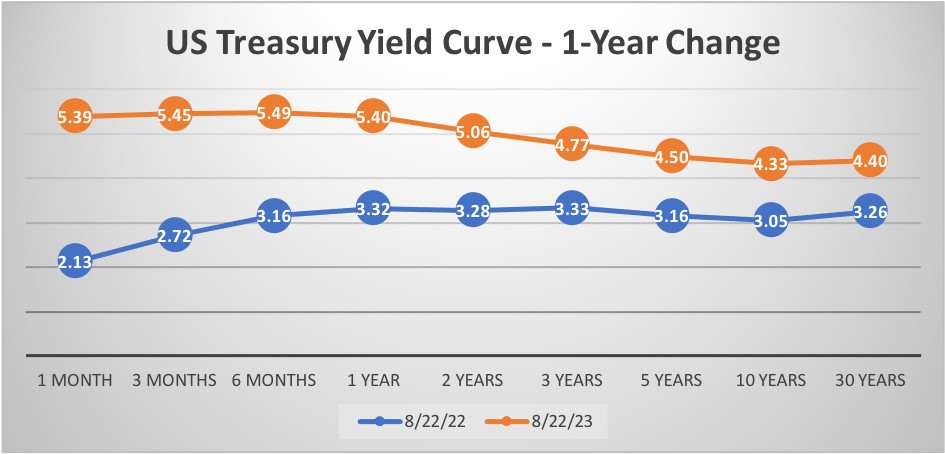

Importantly, a fund’s asset allocation should reflect the current funded status of the plan and not be driven by some return on asset (ROA) objective, that in many cases is a feel good number driven by the ability to manage contributions. Does it really make sense that two plans with very different funded ratios – say 60% and 90% – should have the same ROA objective? Absolutely not! Yet, we see that all the time. Furthermore, benefit payments are future values (FV) and plan assets are in present value (PV) terms, since we don’t know what value those assets will have in the future, except for bonds.

In order to successfully measure, monitor, and manage liabilities, let alone secure them, a plan sponsor needs a Custom Liability Index (CLI) on a frequent basis since each plan’s liabilities are going to be unique to that sponsoring entity. No generic index can ever truly replicate a pension’s liabilities. Importantly, those FV liabilities will be converted into a PV figure monthly providing the plan sponsor with a more accurate and frequent interpretation of the plan’s funded status. In this higher rate environment, the PV of liabilities will be much smaller than previously thought allowing sponsors to take more risk out of the current asset allocation framework.

Ron Ryan, Ryan ALM’s CEO, created the first CLI back in the early 1990s. We believe that every plan should install a CLI in order to do a more effective job of managing a plan’s assets to their liabilities. The CLI is a big part of our turnkey Asset/Liability Management (ALM) capability. Don’t hesitate to reach out to us if you’d like to have a CLI built for you. The first one is on us. We’re confident that you’ll quickly see the benefit in having one produced regularly.