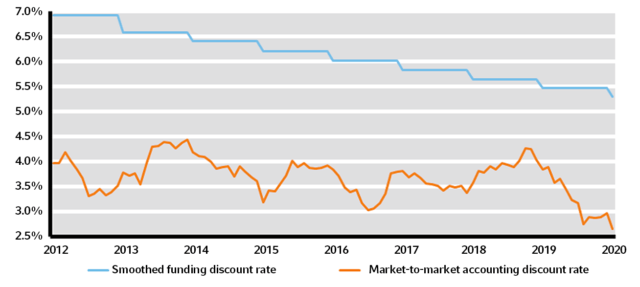

Corporate America continues to use different discount rate methodologies to measure and fund their pension plan’s liabilities. According to Russell Investments, the use of smoothing techniques (90%/110% corridor and 25 years) would create a discount rate of roughly 5.5% today, while a true marked-to-market discount rate would be about 2.5%. Plans claiming to be “fully funded” using smoothing are likely much worse off. The folks at Russell estimated that a plan claiming to be fully funded when using smoothing, would actually be only about 76% if the plan had a duration of about 12 years. A plan at 90% funded with an average duration of liabilities at 16 years might be truly funded at only 64%. Wow!

This certainly has implications for future contributions, PBGC premiums, the ability to engage in risk transfers, and other pension matters. Oh, and by the way, according to Russell “barring future changes to pension law, sponsors ought to be mindful of the coming phase-out of funding relief. With the ongoing decline in the 25-year average determined by the IRS, and the 90%/110% corridor expanding from 2021, the effects of funding relief will increasingly wear away. Contribution requirements will increase for many plans, bringing marked-to-market liabilities into economic reality.”