Anyone who knows Ryan ALM and who has followed our blog posts for years knows that we are big supporters of DB plans as the primary retirement vehicle for the masses. We’ve discussed our rationale for this stance numerous times. That said, recent market action and economic activity have put public pension systems once again in the spotlight. The battle to control the outbreak of Covid-19 has impacted many state budgets from both a revenue (income and sales taxes, lotteries, fees, etc.) and expenses standpoint (Covid-19 emergency responders, PPE, etc.), and the likelihood of escalating contributions into state pension systems may be too much for some states to handle. What can be done?

Unfortunately, there aren’t an infinite number of actions that will improve plan funding, and in the cases of states like NJ, IL, and others, dramatically improve their systems’ funded status. In fact, there are really only five actions that would lead to improved pension funding, including; 1) assets outperform the ROA target, 2) the present value of future liabilities fall, 3) both actions 1 and 2 occur, 4) borrow additional resources (POB), and 5) renege on a portion of the promised benefits.

With regard to action 1, plans have been relying on asset performance for years to make up for contribution shortfalls. In most cases this goal has been met with enhanced volatility, but little reward. As we pointed out in a previous blog, the Bloomberg Barclays Aggregate Index bested the S&P 500 for the 20-years ending March 31, 2020, despite a greater than 10-year bull market for equities, little improvement in funded status occurred.

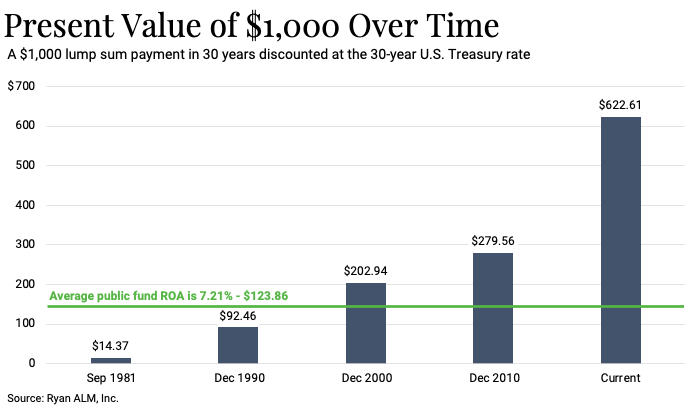

We have been in a protracted bull market for bonds since I entered the industry in 1981. The impact on pension systems from falling interest rates (action 2) has been devastating (I will have more on this issue in a subsequent blog post). How likely are rates to rise from here? Most participants in our industry have felt that rates would “normalize” for years, only to see one event after another drive rates further lower. Action by the US Federal Reserve has damaged (permanently?) pensions and retirees, who need income to sustain quality retirements. The movement of rates lower has correlated with plans and pensioners taking on more risk to try to create additional income. It has also proven to be a disaster.

Ideally, we would enter a protracted period of asset appreciation and rising interest rates that would lead to a fairly quick recovery in pension funding. For instance, at such low market interest rates, a 30 bps increase in rates would create negative liability growth for the plan. Given that dynamic, a Funded Ratio of 60% could improve significantly to 89.4% if in the next 5 years average asset growth was just 4% and average liability growth was -4%. The improvement is even more dramatic if during the next 5 years assets grew by 5%. In this case, the funded ratio would improve to 94.0% if liability growth proved to be negative 4% during this period. But given that our economy is just opening up now, how much economic growth, inflation, and rising rates can we expect in the near-term?

Action 5, the trimming of promised benefits, (yes, I jumped over my fourth “opportunity”) is a last resort action, and in many cases individual state laws prohibit such an action. Since the Great Financial Crisis (GFC), a majority of public pension systems have altered benefit formulas directed at new employees, but that does little to tackle the current under-funding. Furthermore, these plan participants have invested both years of time and their own contributions into a system with the expectation that they would receive the promised benefits. Anything less is truly an affront.

With regard to action 4 and the borrowing of funds, I believe that for states such as NJ, IL, KY, CT, etc. the issuance of a pension obligation bond (POB) is the only way for these systems to climb out from the huge hole that was dug by years of habitually under-funding their plans. POBs have been tried many times before and with mixed results, but I believe that the investment of the bond proceeds was implemented inappropriately, which ultimately lead to the failure of the action.

Historically, a pension plan would take the proceeds from the bond and invest those assets in a traditional asset allocation. As a result, the proceeds are subjected to the whims of the markets. In many cases these assets have been injected at an inappropriate (market peaks) time leading to losses. The plan is then on the hook for the original interest payment on the POB and the loss suffered on the “investment”. To mitigate this risk, any proceeds from the POB MUST be used to defease the plan’s retired lives liability. The current assets in the plan and any future annual contributions would then be used to meet future liabilities. Given the magnitude of the funding crisis, HOPING that assets will dramatically outperform, while interest rates rapidly rise is a lot to ask for. Cutting benefits is a non-starter. Issuing a POB and injecting significant assets into the system to SECURE pension promises seems to me to be the most viable alternative.

Let us know what you think.