By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Will it be 25 or 50? That is the big question on nearly every investor’s mind this week. Will the Federal Open Market Committee cut rates by 0.25% or 0.5% on Wednesday. Any cut would mark the first such move by the Federal Reserve since 2020. Despite the uncertainty as to the Fed’s potential action, the PBGC was undaunted as they had another busy week implementing the ARPA pension legislation.

There is plenty to highlight from last week’s activity, as three funds received approval of their applications seeking Special Financial Assistance (SFA), one fund repaid a portion of its SFA grant, while another withdrew its initial application. There were no applications filed this past week as the PBGC’s filing portal is temporarily closed. Multiemployer plans seeking SFA may still “request to be placed on the waiting list in accordance with the instructions in PBGC guidance.”

The three funds receiving SFA were Teamsters Local Union No. 469 Pension Plan, Pension Plan Private Sanitation Union, Local 813 I.B. of T., and Local Union No. 226 International Brotherhood of Electrical Workers Open End Pension Trust Fund. These funds were each non-Priority Group members and the applications were the initial filings for each. In total, these pension plans will receive $238.3 million in SFA and interest for just over 6k members.

Local 1783 I.B.E.W. Pension Plan, an Armonk, NY non-Priority Group member, withdrew its initial application. They were seeking $42.2 million in SFA for the 850 plan participants. The Alaska Iron Workers Pension Plan received approval for its application in January 2023. They have just agreed to return $384,111.74 from the $53.5 million received in February 2023, as a result of a census error. This is the fourteenth plan to return a portion of the SFA due to overpayment.

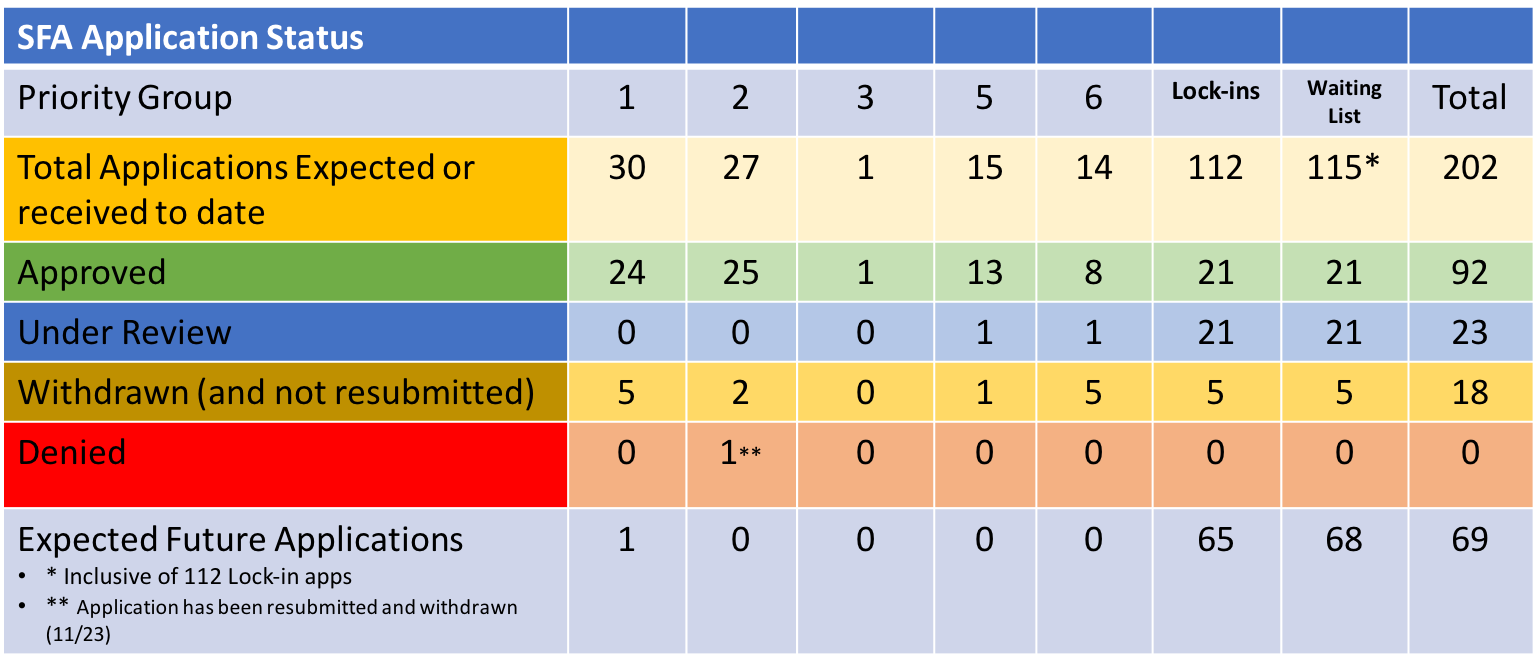

As one can see, the PBGC has approved 92 of a potential 202 applications (45.5%) at this time for a total of $68 billion in SFA, including interest FA loan repayments. As a reminder, plans receiving SFA proceeds must keep those separated from the plan’s current fund (legacy assets). Despite the recent decline in US interest rates, defeasing benefits and expenses as far into the future as the SFA grant will cover is still the proper course of action. I produced a post last Friday on the correct approach to cash flow matching for those considering such a strategy.