By: Russ Kamp, Managing Director, Ryan ALM, Inc.

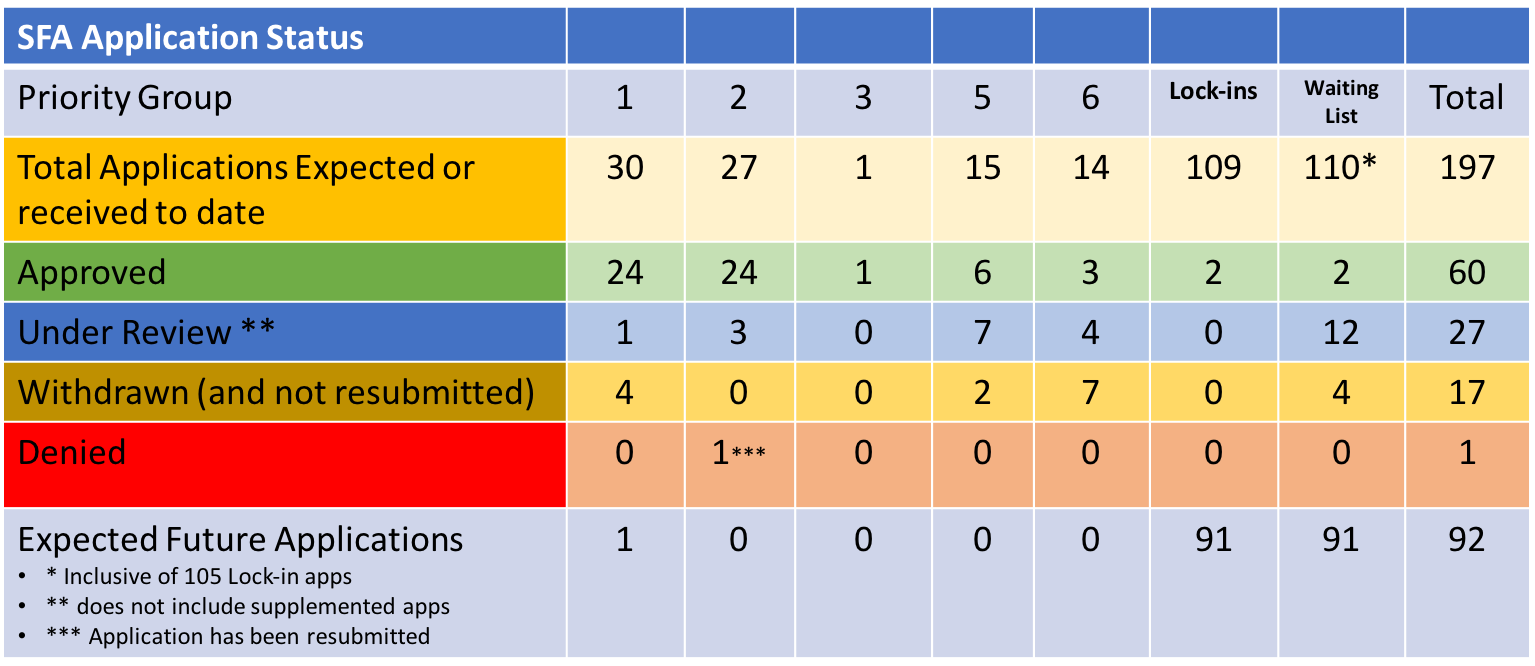

For us in the Northeast, the start of September marks the beginning of another school year for our K-12 students. We hope that your summer has been wonderful. For the PBGC, the beginning of September just marks another month of focus on ARPA and the approval and distribution of Special Financial Assistance (SFA) for eligible multiemployer plans. They have now been active with ARPA since July 2021. To date, 60 plans have received SFA, with some getting additional funding through supplemental organizations.

During the last week of August, the PBGC approved the SFA for one plan – Ironworkers Local Union No. 16 Pension Plan – which will receive $75.8 million, including interest. This Priority Group 2 plan needed to submit a revised application before getting approval. In other news from last week, Teamsters Local 11 Pension Plan, a plan without a priority designation, submitted its revised application. They are seeking $28.9 million in SFA for their 2,012 plan participants. The week witnessed no applications being either withdrawn or denied and no new plans were placed on the waiting list.

In a post from earlier today, I reminded folks about the need to protect and preserve the SFA, as required by the legislation, especially given the rising rate environment and the potential significant losses that rising rates will cause to a bond’s principal. Who knows whether or not the Fed is done with tightening? But, if they remain data dependent, the current environment suggests to us that they have NOT accomplished their objective (controlling inflation) at this time.