By: Russ Kamp, Managing Director, Ryan ALM, Inc.

The management of a pension system should be done in similar fashion to how both insurance companies and lottery systems operate. They know what the future value of liabilities are that they are obligated to fund and they manage to that objective. They don’t try to build an investment structure that might achieve an expected/desired return (ROA) some 10-, 20-, or 30-years out.

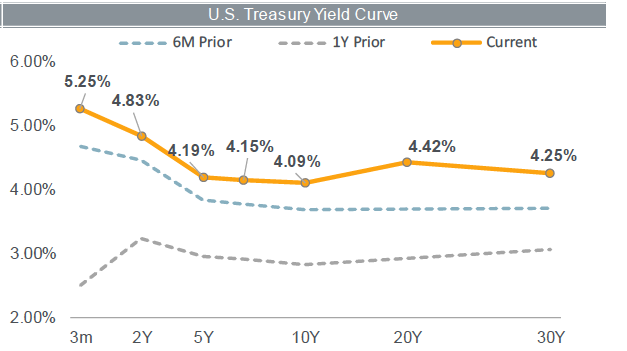

That said, the significant decline in US rates from 1982 to March of 2022 made managing a pension system incredibly challenging, as income from fixed income (bonds) was historically low forcing plans to take on more risk to try and achieve the plan’s ROA objective through more volatile investments. Well, the Fed’s aggressive action to thwart inflation which began in March 2022 and has now led to 11 increases in the Fed Funds Rate may have impacted the capital markets from a return standpoint in 2022, but they are having an incredibly positive impact on the income produced from bonds. As the yield curve below highlights, we’ve seen a massive shift up in rates across the Treasury yield curve, especially in shorter maturities.

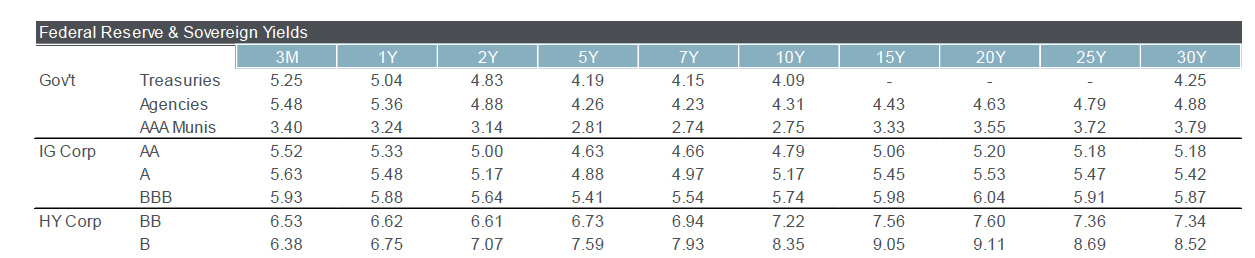

This dramatic shift upward in Treasury yields has also been witnessed in the yields of corporate bonds, both investment-grade (IG) and High Yield (HY), as the chart (thank you, RBC) below highlights. At Ryan ALM, Inc. we believe that the primary objective in managing a defined benefit plan (DB) is to SECURE the promised benefits at a reasonable cost and with prudent risk. Given the significantly higher yields on US bonds, this objective has become much easier. We believe that cash flow matching (CFM) a pension plan’s liabilities (benefits and expenses (B+E)) with asset cash flows (bond interest and principal) a plan can accomplish the objective cost effectively and with prudent risk.

We’ve recently been building defeased (CFM) bond portfolios with yields in the 5.5% to 6% range through our focus on A and BBB bonds (no BBB-). These yields are providing our clients with a significant reduction in the cost to defease future liabilities. Bond math is very straight-forward. The longer the maturity and the higher the yield the greater the funding cost savings. We’ve entered a very attractive time when plan sponsors can effectively secure the promises made to their participants without having to take on substantial risk.

While the defeased bond portfolio is providing the liquidity to meet benefits and expenses chronologically, the non-bond assets (growth/alpha) can grow unencumbered with the goal of paying future B&E. It has been a long time since the bond market has provided such a wonderful opportunity. Given the uncertainty surrounding inflation and the Fed’s reaction to it, bond yields may in fact rise even further as real rates have not been achieved for longer-term maturities versus “core” inflation, which continues to hover around 5%. Don’t hesitate to reach out to us. We’d be happy to model the potential cost reduction that your plan could experience through a cash flow matching implementation.