By: Russ Kamp, Managing Director, Ryan ALM, Inc.

I’ve had the great pleasure of speaking at a number of industry events so far in 2023. I usually begin my portion of the talk or panel discussion by asking a very simple question: Was 2022 a good or bad year for pensions? That question often generates a response from the audience that makes it appear that I have 3 eyes and have suddenly turned green. I say that because most people in the US pension industry, especially among public and multiemployer plans, focus almost exclusively on the asset side of the pension equation since the return on asset (ROA) assumption is their primary objective. They understand that rising US rates led to declining valuations for both stocks and bonds, and likely many if not all alternative investments, but since those don’t get marked-to-market one never really knows. They’ve seen that the S&P 500 was down -18%, while Bloomberg Barclays declined an unprecedented -13% for the year.

What they failed to understand is the impact of rising rates on the present value of the pension plan’s liabilities, which are bond-like in nature. In a rapidly rising rate environment, long-duration pension liabilities’ present values fell rather dramatically. In fact, the decline in the present value of those liabilities dwarfed the decline in assets. This relationship is more obvious in pension accounting for corporations, but it is still true for public and multiemployer pension plans despite the GASB accounting standards that permit the ROA to be used as a liability discounting mechanism.

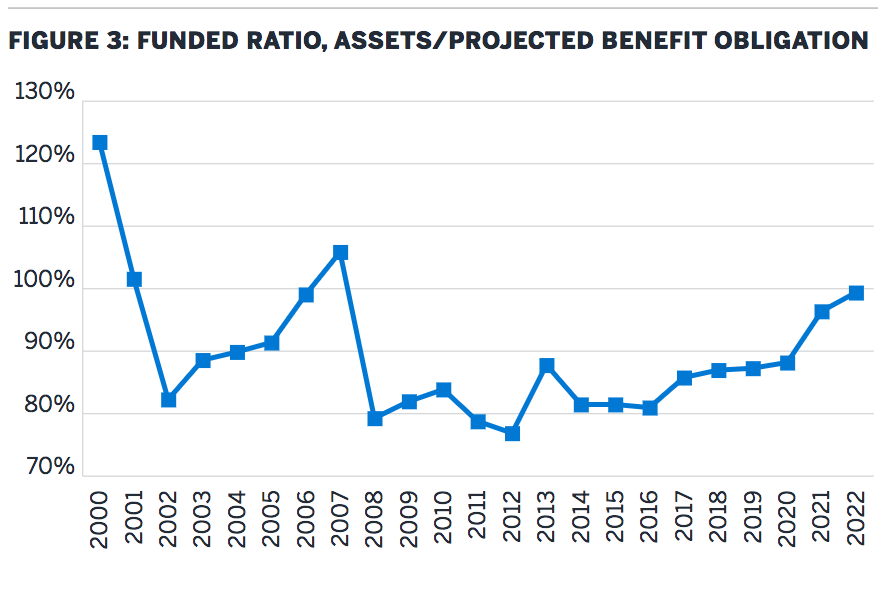

So how good was 2022 for Corporate America? According to the Milliman study (thanks to Zorast and team) “the funded ratio of the Milliman 100 pension plans increased during FY2022 to 99.3% from 96.3% at the end of FY2021.” Furthermore, “the 245 basis point increase in liability discount rates was sufficient to overcome the plans’ average -18.6% investment return, allowing the private single-employer DB plans of the Milliman 100 companies to reduce the multibillion-dollar pension deficits for the second straight year, falling just short of full funding in 2022.”

Corporate pension funding has only been in better shape twice before going back to 1999. Regrettably, Pension America failed in both cases to secure the promised benefits through a defeasement strategy preferring a gambler’s mentality of “let it ride”! Well, we know what followed previous funding peaks in 2000 and 2007. No one should be comfortable leaving chips on the table at this time. The current US interest rate environment is enabling Ryan ALM to produce investment-grade bond portfolios with a YTW of >5.5%. The present value of assets is able to secure substantial future value benefits and expenses. Our objective in managing pension assets has never been a return focus. It is our goal to SECURE the promised benefits at a reasonable cost and with prudent risk. Let us help you secure the promises that you’ve made to your employees. They will certainly appreciate your effort.