By: Russ Kamp, Managing Director, Ryan ALM, Inc.

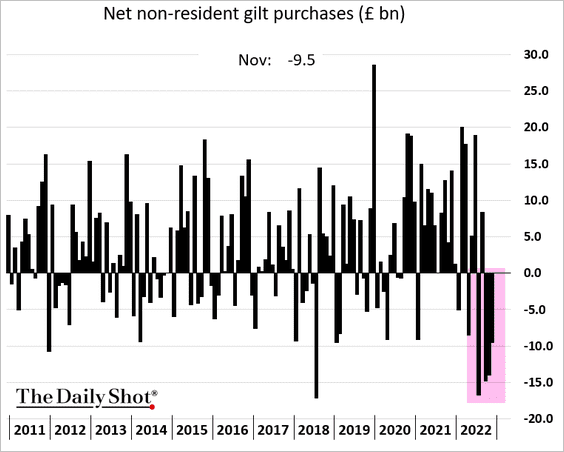

September’s wild ride within the UK pension market has been replaced by relatively calm seas since. But is that situation an illusion? The following chart highlights some major concerns, as UK Gilts are being sold at record levels by foreign investors.

As a reminder, failed policy decisions by the former UK Prime Minister led to a vicious cycle of rising UK interest rates and Gilts sales. Those actions combined to nearly cripple the UK pension system as levered, and in some cases HIGHLY levered, duration strategies utilizing derivatives forced plan sponsors to seek liquidity to meet nearly daily margin calls. The collateral for the most part was Gilts, and the forced selling was only stopped when the UK’s Bank of England stepped into the fray by buying multiple billions of Gilts. That action certainly worked in the short term, but where are we today?

The continuing selling of Gilts (estimated at 38 billion Pounds for the three months from September through November) represents the greatest monthly average sum since the BOE started keeping records of such transactions in 1982. Foreign investors own nearly 30% of the UK debt. This selling pressure comes at a challenging time, as the UK Treasury is facing one of its largest Gilts funding needs in the next financial year at nearly $300 billion, while the BOE simultaneously tries to unwind more than 40 billion Pounds in Gilts under its October QE program. I’m not yet sure how this impacts the UK pension system. Have they sufficiently unwound highly levered LDI duration strategies utilizing derivatives or are they continuing to sit with those positions? Perhaps one or more of our readers could share some insights with us based on specific knowledge of the current UK pension market.

In any case, 2023 may be another challenging year for UK markets and the pension systems that operate within them. Clearly, there is much more to the story, and we will bring it to you as it unfolds. Stay tuned!