By: Russ Kamp, Managing Director, Ryan ALM, Inc.

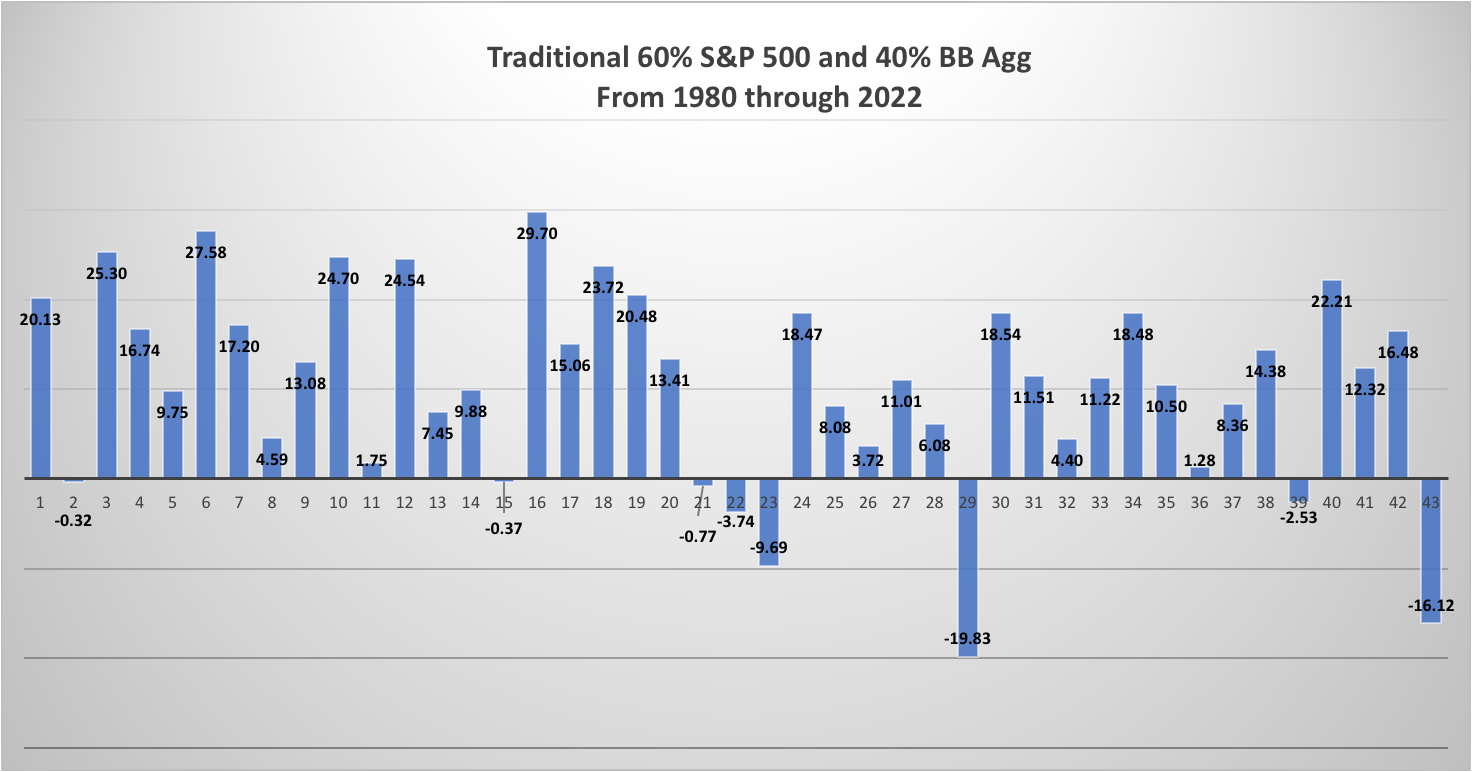

The last 43 years have been an extraordinary time for both bonds and stocks. Including the calendar year 1980, a 60% S&P 500 and 40% BB Aggregate asset allocation produced an incredible 10.44% annualized return, with only 8 down years during that period. This average return far exceeded the average ROA for pension America. The consistency of the equity and fixed income returns is what is most shocking, as there have only been 5 negative calendar years for bonds and 8 negative calendar years for equities. Furthermore, there has only been one year, 2022, in which both indices produced a negative return in the same calendar year. Is it a prelude of things to come or just an anomaly in a continuing extraordinary performance period for US markets?

What was unique about the last four decades that isn’t present today? First and foremost, we had the US 10-year Treasury Note yield finishing in 1980 at 12.4%. It would subsequently climb to 14% during 1981 before beginning its long descent to 0.7% at the end of 2020. At the same time, the Fed Funds Rate would hit 20% in 1980 and rise to 21% by June 1981 before beginning its fall to a zero interest rate policy (ZIRP) by 2021. That amazing interest rate change was done in an environment of 3% core inflation during those 43 years. Clearly, this scenario isn’t repeatable given where US rates are today. We find it somewhat humorous that investors are wringing their collective hands with a 10-year Treasury yield at 3.8% today.

Given our current employment situation (3.7% unemployment), wage growth averaging 6% annual growth, core inflation (PCE) at 5.5%, and a Fed that wants inflation @ 2% with real rates, we don’t see the Fed “pivoting” back to an easy money policy anytime soon. Without the incredible tailwind of falling rates enjoyed by market participants for 40+ years, we don’t expect the next 10 years to produce returns anywhere close to the annualized return of 10.44% produced by a 60%/40% asset allocation. Given this likely scenario, it becomes incredibly important to ensure that adequate liquidity is available to meet benefits and expenses. Adopting a cash flow matching strategy for the fixed income portion of the assets ensures liquidity while also “buying time” for the growth (alpha) assets to grow unencumbered. Given that 40 years of easy Fed policy is off the table, adopting a different approach, one that has worked for decades, should be considered before markets get even more challenging should a recession unfold.