By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Is bigger better? Do firms that have huge research staffs perform better than investment shops that don’t have the same internal resources? How do you know? Where do experience and expertise get factored in? Shouldn’t the firm with the greatest experience and expertise be favored… quality vs. quantity? Have you actually evaluated their security selection relative to a generic universe?

I ask these questions because we’ve had a number of meetings recently in which leading consulting firms have implied that Ryan ALM’s size (four senior asset managers with 168 years of combined experience) is an impediment to our ability to achieve the goals and objectives of a Cash Flow Matching mandate. With only one product (cash flow matching) Ryan ALM has a truly dedicated staff with a wealth of experience. We are asset liability management specialists as our name implies. When you need surgery, we assume you want a specialist to operate on your heart and not a general practitioner.

In one case we conducted a “lunch and learn” for a major consulting organization that asked us to present cash flow matching as they hadn’t been using the strategy since they favored duration matching. We were very pleased to present to roughly three dozen members of their team. Here is a bit of the feedback following our 1-hour meeting. “We appreciate you coming in person to teach and remind us about cash flow matching. A few of us agreed that the cash flow matching approach can be used to mitigate volatility in today’s environment”. However, “for now we are focusing on larger managers where we already have client assets.” My response was, why didn’t those larger managers take the time to remind you about the benefits of cash flow matching instead of doing what everyone else was espousing in terms of using duration matching?

In another meeting, we were told that Cash Flow Matching models are like commodities. That the real value add is in credit research. Really? Have you spent the time to examine the models? Did you ask to see the software that supports each optimization process? I would suggest that you present each of your manager candidates with the same set of liabilities (benefits and expenses) and ask that they produce a portfolio based on that information. I guarantee that there will be differences that might just prove to be substantial. The firm producing the greatest difference in cost between the future value (FV) of the benefits and expenses relative to the present value (PV) cost has the most efficient model. These systems are not commodities! If that were the case, every fixed-income shop would be claiming to have this capability, especially in this market environment in which total return fixed-income products have produced significant negative performance, and will continue to be under pressure as the Fed further tightens rates.

With regard to internal credit research, how valuable is that firm’s investment in internal talent when investment-grade bonds have experienced minimal credit risk during the last four 4 decades? Unlike total return-oriented bond portfolios, duration matching and cash flow matching should be concerned about solvency since you can hold the bonds for a long horizon… maybe maturity. Ryan ALM has had no defaults under our proprietary credit filtering system since our inception in 2005. Have you asked those firms with big internal research departments to provide the value-added achieved from their “greater” security selection? It would be very simple to ask for the performance of their bond universe and then ask for the performance of the subset that was used to construct the client’s portfolio. My guess is that the “value-added” will be quite insignificant. It would likely be insignificant relative to what a firm using the output from the credit agencies, Bloomberg, and other readily available quantitative and qualitative inputs could achieve. Furthermore, human beings possess 23 behavioral traits, many of which work against us as “investors”. It takes a contrarian view to make money yet being a contrarian is very challenging, and has been described as being as painful as chewing off one’s left arm!

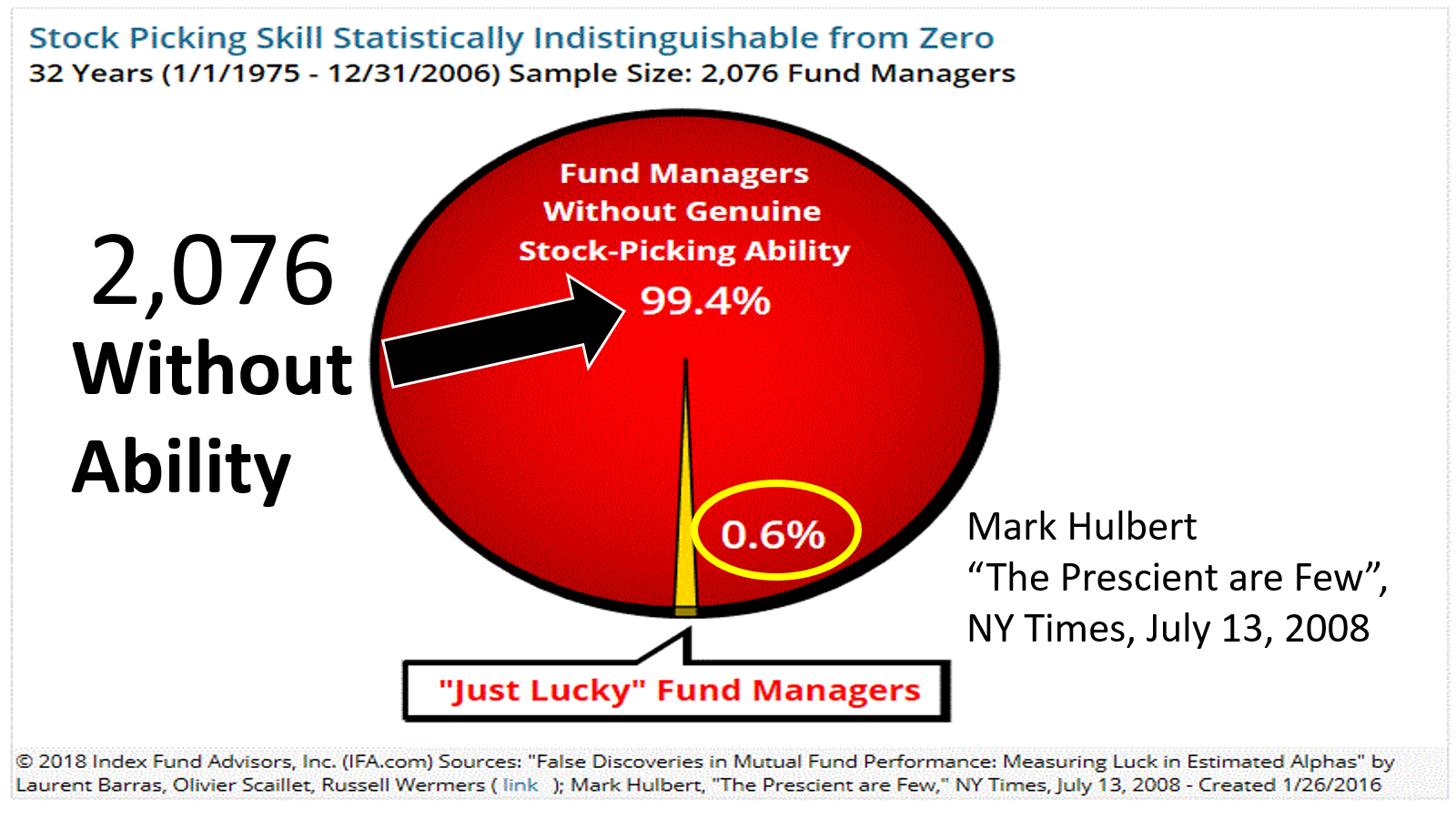

As the chart below suggests, there are very few individuals who truly possess the ability to add value through security selection. In this example, we are highlighting the inefficiencies of stock pickers. Do you think that bond managers/analysts have greater skills? I would suggest that the much smaller standard deviation among like bonds makes the task that much more challenging.

In my 41 years in this business, I’ve come to appreciate that there is a natural capacity associated with every investment strategy. Many of the larger firms in our industry have far eclipsed that capacity and as a result, they ultimately arbitrage away the potential value added from their insights. What they’ve proven to be is mostly effective sales organizations. In today’s challenging market environment, we need real solutions provided by true specialists. Size doesn’t matter, but capability and execution do!

I would certainly look into your company as a portfolio manager if I were heading up a pension fund.

Thank you!

Russ this article is a keeper – which I will do. Best C

Thank you, Chuck. I hope that all is well with you. Have a great day.