By: Russ Kamp, Managing Director, Ryan ALM, Inc.

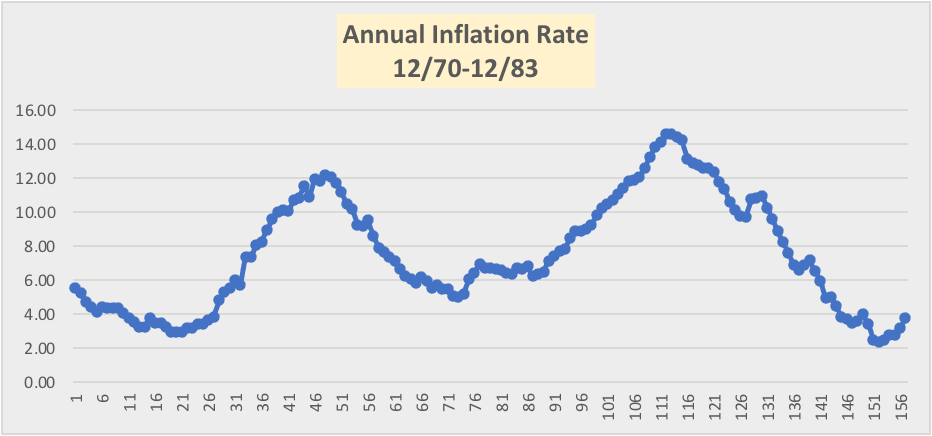

Ryan ALM’s Head Trader, Steve Devito, shared some extraordinary figures with the team last week. Thanks, Steve! We’ve been saying all along that the US Federal Reserve needs to tighten interest rates to a significantly greater extent in order to finally control inflation. We’ve produced blog post after blog post highlighting what we believe to be the reality of our current situation despite market action during the last month or so that would counter our observations. Let’s take a look at some of the numbers from the last period in which we observed inflation in excess of 8% (the latest CPI # posted was 8.5%). In February 1982 the CPI for the month was 0.3% and the annualized inflation # stood at 8.3%.

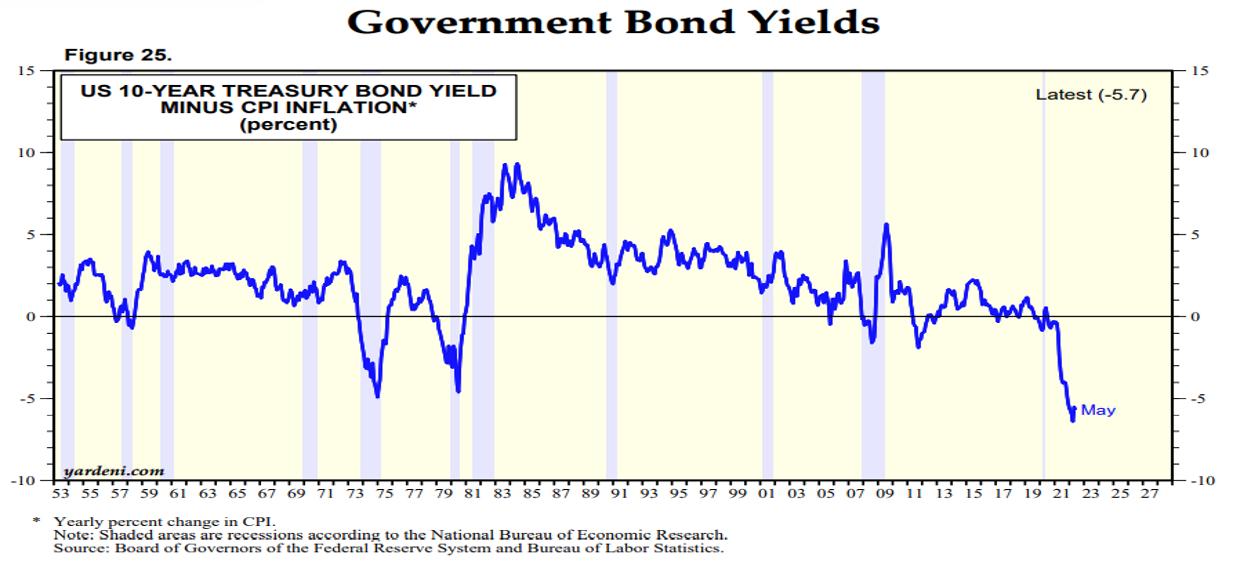

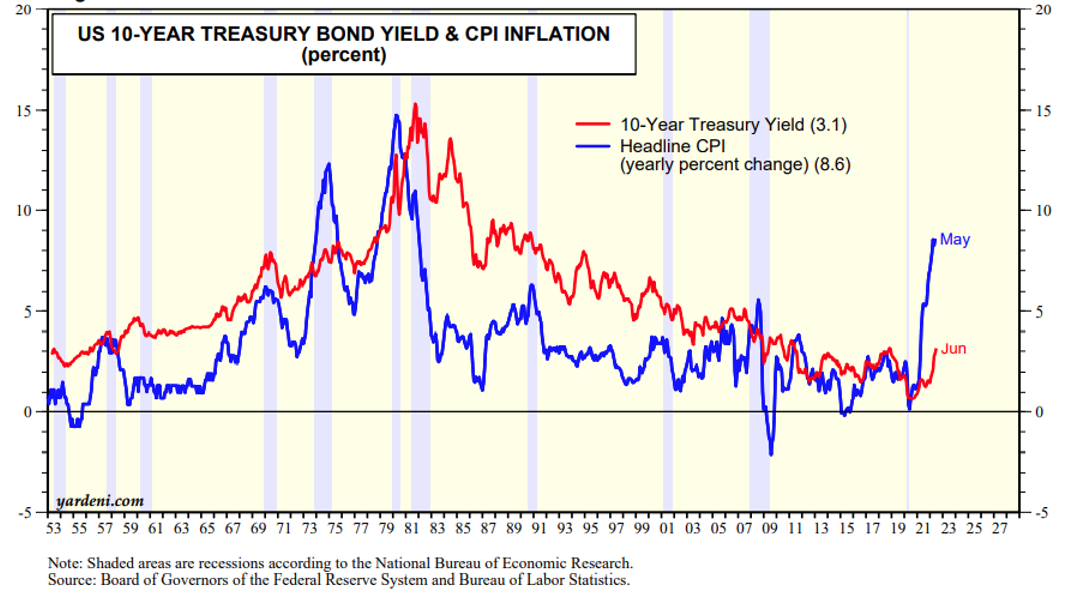

However, unlike today’s environment in which the Fed Funds Rate (FFR) stands at 2.25%-2.50%, the FFR during that month was a robust 14.8% representing a 6.5% premium to inflation. Not the -6% “premium” that exists in today’s environment. Furthermore, the 2-year Treasury Note was trading at a yield of 14.45% far outpacing today’s 3.17% yield. It seems extraordinary that today’s “investors” would actually believe that a 2.25% FFR would tamp down our significant inflation. Furthermore, why are they willing to hold bonds at such negative real rates? Skeptical that I may have cherry-picked a bond that was an outlier? For further proof of just how unbelievable today’s environment is, the 10-year US Treasury Note was yielding 14.03% in February 1982, which was -0.77% relative to the FFR, but a whopping +5.7% real rate when compared to inflation.

The 30-year Treasury Bond also showed similar results, as its yield was 13.8% for a real yield of 5.5%. Again, we ask, do you really believe that the Fed has accomplished its objective? How much economic activity do you really believe will be constrained by these incredibly modest levels of interest rates? Could it be that we have 2 generations of investors who have not experienced excessive inflation leading to significantly rising rates? Despite the double-digit FFR in 1982 (14.8%), inflation didn’t fall below 3% until July 1983 and it never touched 2% – the current Fed target – before rising again to 3.4% by year-end 1983.

With today’s robust employment and wage growth, is the average consumer more concerned about inflation or borrowing at slightly higher rates? My money is on inflation, as is the Feds. How many more times do we need to hear from a Fed Governor that inflation needs to be contained until rates can be stabilized? They’ve stated that they haven’t been dissuaded from raising the FFR based on newly released information. Not only are equity and bond investors giddy about inflation’s path, but they actually believe that the Fed may ease in the near term. However, Thomas Barkin, Fed Governor from the Richmond Fed, said on TV last weekend that the Fed needs to see real positive rates. Why the disconnect?

We aren’t suggesting that the Fed will raise the FFR to 14.8% in this environment, but 2.25%-2.5% seems like a small down payment on where rates will eventually need to go in order for this august governing body to have achieved its ultimate objective. Hoping that rates have peaked likely sets our markets up for massive disappointment leading to further declines. The greater the current euphoria the likely the bigger disappointment. Pension America has seen some nice recovery in markets. Let’s hope that they take some steps to reduce risk before everyone realizes that the Fed has much more to do. Securing benefits through enhanced liquidity and the buying of time – Ryan ALM specialties – may just be the necessary prescription for what lies ahead.