By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Buying the dip is always a challenging objective. Given the current inflationary environment and the goal of the Federal Reserve to conquer inflation, buying this dip may be premature.

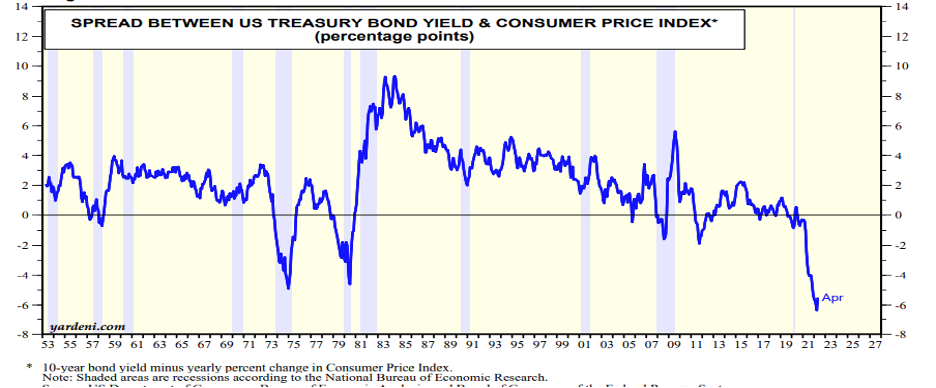

As the graph above depicts, the spread between the US 10-year Treasury bond yield and the consumer price index (CPI) has been significantly positive (i.e. inflation premium) throughout history with a few exceptions. As of April 30, 2022, the negative real return from owing the 10-year Treasury was the greatest in history. May’s inflation # of 8.6% certainly didn’t reduce this unusual relationship. Yet, recent market activity seems to suggest that the Fed’s recent 75 bps increase in the Fed Fund’s Rate may have already started the US economy on a slippery slope to recession. I think that is a bit premature.

Fed Governor Bowman was quoted in the WSJ yesterday stating that “since inflation is unacceptably high, it doesn’t make sense to have the nominal federal-funds rate below near-term inflation expectations”. She continued, “I am therefore committed to a policy that will bring the real federal-funds rate back into positive territory.” Can her message be any clearer? Given that the 10-year Treasury yield’s real rate is -5.5% today, it seems obvious to me that the Fed is nowhere close to slowing down its forecasted rate increases, even if you assume some magical collapse in the inflationary environment to roughly 4% by year-end.

There have always been short-term rallies throughout the history of market corrections, but they often don’t signal the bottom of the markets. Given the drivers of inflation and the primary objective of the Fed to curtail said inflation, buying this dip may be premature. You might have to wait until you can buy the canyon! Stagflation or recession? Neither is good for stocks and rising rates are a killer for total return-focused bond programs. Bifurcate your assets into two buckets – liquidity and growth. Use bond cash flows to meet liability cash flows… liquidity assets. This strategy will enhance your fund’s liquidity while buying time for those growth assets to grow unencumbered. You won’t have to guess when you’ve hit the bottom of a cycle.

That’s the right question Russ: How high can we go? When interest rates are not manipulated long term bonds have yielded 3% above the rate of inflation, so the “natural” rate in an 8.5% inflationary environment is 11.5%.

Although Fed rate hikes grab headlines, that’s just for show because the Fed needs to appear to be in control. Tapering is the important action. As the Fed takes its foot off the interest rate brake, the small interest rate increases we’ve seen so far will escalate.

Stay tuned. Many believe the Fed will be pressured to re-apply the brakes. If they do, they’ll fuel the inflation fire by printing more money. It’s ugly!!

Thanks for your thoughts, Ron. Why investors are willing to accept this significant negative real yield is beyond me.