By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Last week the US Federal Reserve indicated that the discount rate increase of 25 bps was just the beginning of what might be 6 additional increases this year. Given the level of inflation – both consumer and producer – this move by the Federal Reserve was not a shocker. Furthermore, there are several members of the FMOC that have 3.75% in their target. This level would be a game-changer!

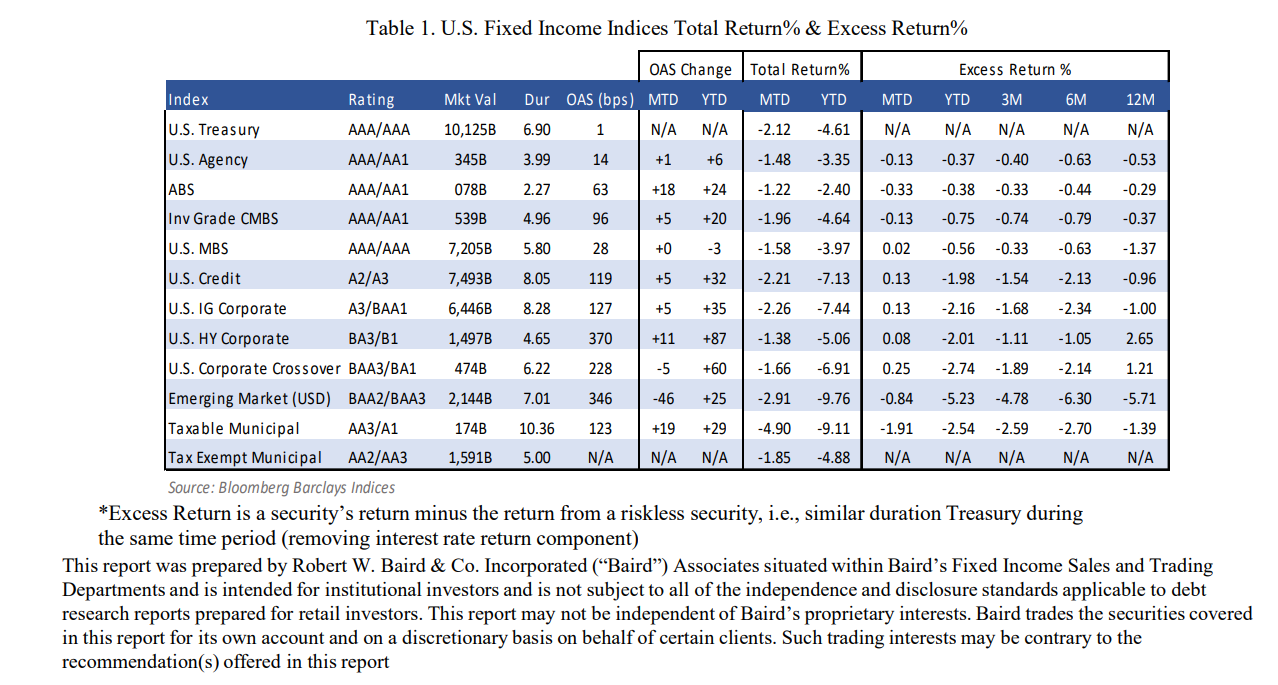

We at Ryan ALM have been suggesting for quite some time that a rising interest rate environment would be quite painful for total return bond programs. Given how early the Fed is in the process, we are a bit surprised by the magnitude of the underperformance by most segments of the US fixed income market year-to-date. The chart below was prepared by Robert W. Baird & Co. It supports our stance that a new day is dawning for US institutional investors who haven’t seen a protracted bear market in fixed income since 1981 and the impact that a lengthy period of sustained interest rate increases would have on fixed income portfolios focused on total return.

We once again implore you to convert your current fixed income from a return-seeking portfolio to one that uses fixed income cash flows (interest and principal) to match liability cash flows. A cash flow matching strategy will ensure that both assets and liabilities move in concert with each other mitigating the most significant bond risk, which is interest rate risk. It also buys time for the pension system’s alpha (growth) portfolio to grow unencumbered as it is no longer a source of liquidity. We’ve enjoyed a wonderful nearly 40-year bull market for bonds. The wind finally looks to have shifted from being at our backs to be blowing right in our face. Don’t let the markets drive your funded status. Take control and it starts now by addressing your fixed-income portfolio. Oh, and by the way, a significant increase in US interest rates will also negatively impact equities and real estate.

If inflation remains above 7%, interest rates on long bonds should increase to 10% if the Fed takes it’s foot off the brake. i.e. “tapers.” With duration above 6, a 5% increase in yield will cause a 30% loss in bond prices.

Yes Sir! It could get ugly real fast! The impact of such an increase will likely cripple real estate and signficantly damage equities, particularly mega cap tech stocks. Please continue your fight to garner dramatic improvement in target date fund asset allocation strategies.

Thanks Russ