The American Rescue Plan Act is wonderful news for plan participants stuck in struggling multiemployer plans, especially in those specific cases where benefits have been cut under MPRA (18 plans in total). It is found money that improves the plan’s funded status. But as I’ve mentioned through various outlets the legislation falls far short in providing the necessary assistance to ensure that the promised benefits are actually paid until 2051. Worse, it appears that many of the roughly 130 plans eligible for this federal assistance will become insolvent prior to then.

We, at Ryan ALM, have been espousing that the Special Financial Assistance (SFA) should be managed with a liability focus that will ensure that benefits and expenses are matched carefully with SFA assets (100% fixed income). We have also been saying that the legacy assets and the SFA should be looked at as a single team of assets for asset allocation purposes. In that scenario, the legacy assets can be managed with a greater exposure to performance assets by removing the allocation to fixed income here since fixed income is 100% of the SFA portfolio. This should enhance the probability of achieving a higher ROA on the legacy assets. The SFA assets are liquidity assets whose mission is to cash flow match (defease) benefits chronologically which will buy time for the performance assets to grow unencumbered.

Since the new SFA assets enhance the funded status, a new adjusted ROA should be calculated for the legacy assets only, so they know the economic hurdle rate to reach a fully funded plan. This new economic ROA is best calculated on a net liability basis including projected contributions. We highly recommend an Asset Exhaustion Test (AET) as the methodology to calculate this new economic ROA hurdle rate. Once this new ROA is calculated, the asset allocation for the legacy assets can now be assessed with a clear knowledge of its return mission.

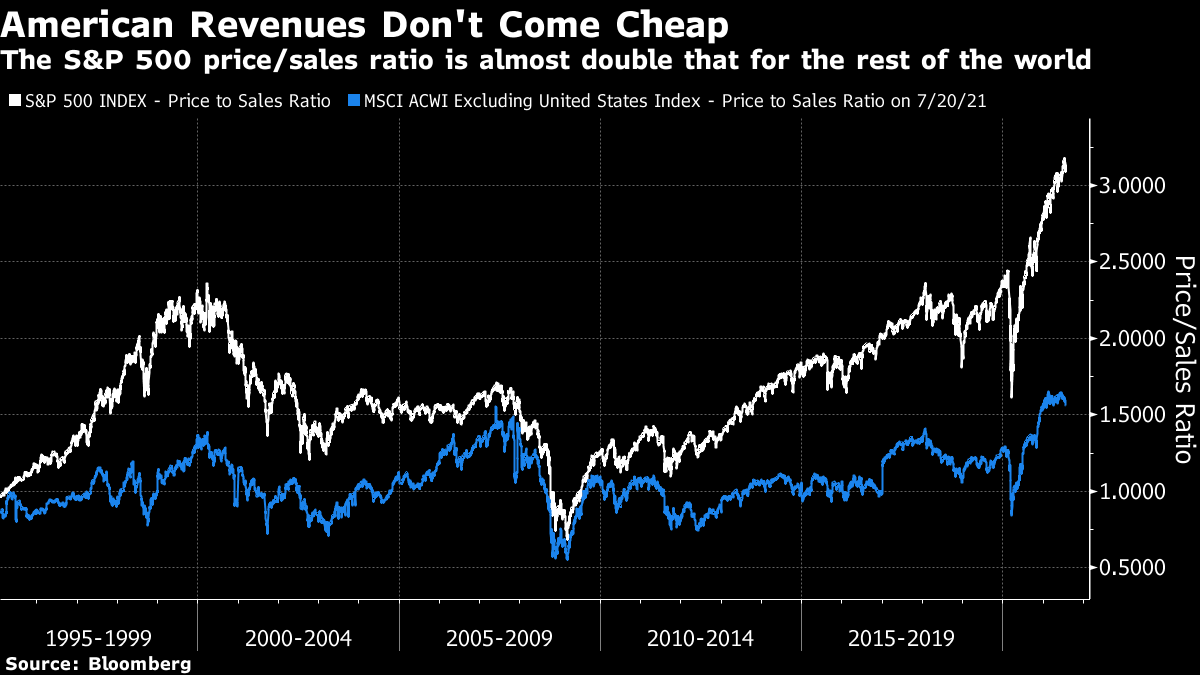

By defeasing liabilities for an extended period of time (8-12 years or more) the asset allocation investing horizon for the legacy assets is dramatically increased allowing for these assets to grow unencumbered as they are no longer a source of liquidity. The S&P 500 has outperformed bonds in 82% of rolling 10-year periods. I like those odds, but the current equity environment may not be a “normal” environment. Two charts produced by Bloomberg provide me with ample angst! The chart titled American Revenues Don’t Come Cheap highlights the US P/S multiple versus the rest of the world and reflects a valuation more than twice as great as the S&P 500/MSCI ACWI. As a point of reference, the US P/S ratio was only 0.9 when the market crashed in October 1987.

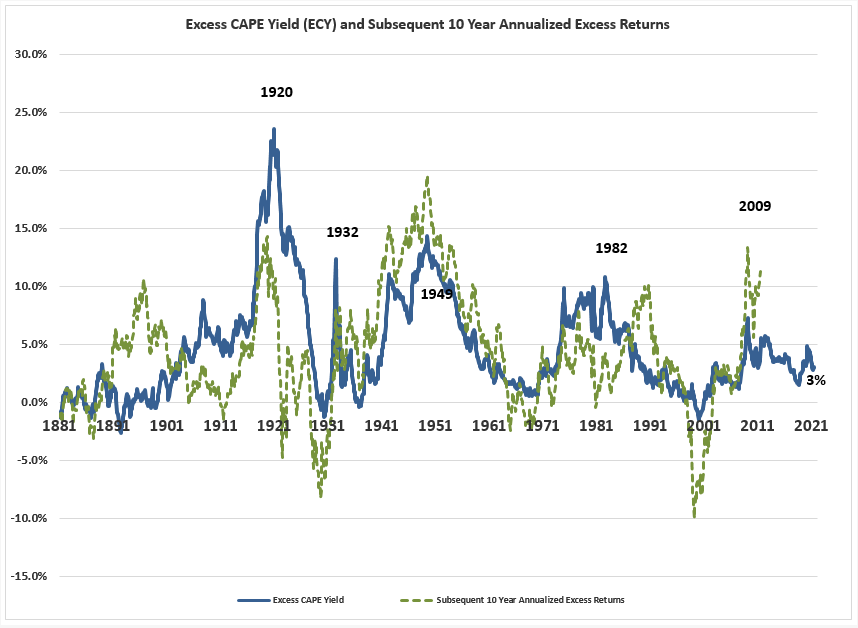

Worse, Robert Shiller’s cyclically adjusted price-earnings multiple, or CAPE, which compares an index’s price to average inflation-adjusted earnings over the previous decade is at a level not seen since 2000, which represented the all-time high. The chart below forecasts the subsequent 10-year return for US equities versus bonds by calculating the excess CAPE yield, or ECY, which is the gap between the CAPE earnings yield (the inverse of the ratio) and the 10-year bond yield. At 3%, the forecasted outperformance of equities to bonds is not nearly enough to get plans to the ROA especially with the 10-year Treasury note currently sitting at a yield of just 1.28%.

Given where equities are at this time, plan sponsors and their consultants will need to get quite creative with their asset allocations for legacy assets in order to create a potentially winning formula in their quest to achieve the new economic ROA. It appears to us that the only certainty of success resides in the SFA bucket if the assets are defeased to the plan’s liabilities and expenses. Time will help this situation, but is 10-years a long enough time horizon given where valuations currently reside? If the markets aren’t going to help mitigate some of the funding shortfall, perhaps we can hope that Congress will once again take up pension reform to provide the necessary resources to ensure that the currently struggling pension systems can remain solvent long after 2051.