Since the first use of Pension Obligation Bonds (POB) in 1985 (Oakland, CA), results have been checkered at best. Boston College Center for Retirement Research (CRR) has produced two studies related to POBs and neither shines a great light on the use of POBs to improve funding for public pension systems. Furthermore, the Government Finance Officers Association (GFOA) has come out strongly against the use of POBs “regardless of the economic cycle”, which I guess is a reference to the current environment of historically low-interest rates in the US. But are they thinking about the use of POBs in the right light?

As we know, states and municipalities have issued these securities “hoping” to capture the arbitrage between the ROA (plan’s asset return forecast plus the discount rate) and the interest payment on the bond. For most cases from 1992-2009, the bonds were issued and invested at the wrong time in the cycle leading to underperformance and an increase in the plan’s liabilities. In the 2014 study, CRR found that bonds issued in 2009 and later had shown improved results once again highlighting that timing is an important factor, and we all know how difficult it is to time the market, especially when the POB assets are injected into the plan’s traditional asset allocation, with all the gyrations that markets can create.

All that said, there is a strategy that can be used that can dramatically increase the probability of success. Sure, taking advantage of low interest rates is still an important consideration, but this prudent strategy significantly reduces the “timing” element of when the assets are invested. I think that the GFOA would appreciate a strategy that bifurcates a plan’s assets into two buckets – beta and alpha. The beta assets would use some of the POB’s proceeds to defease the plan’s retired lives liability chronologically for the next 10-years or so. This provides the remainder of the POB proceeds and the current plan assets to be managed more aggressively since they now have a longer investment horizon of 10 or greater years.

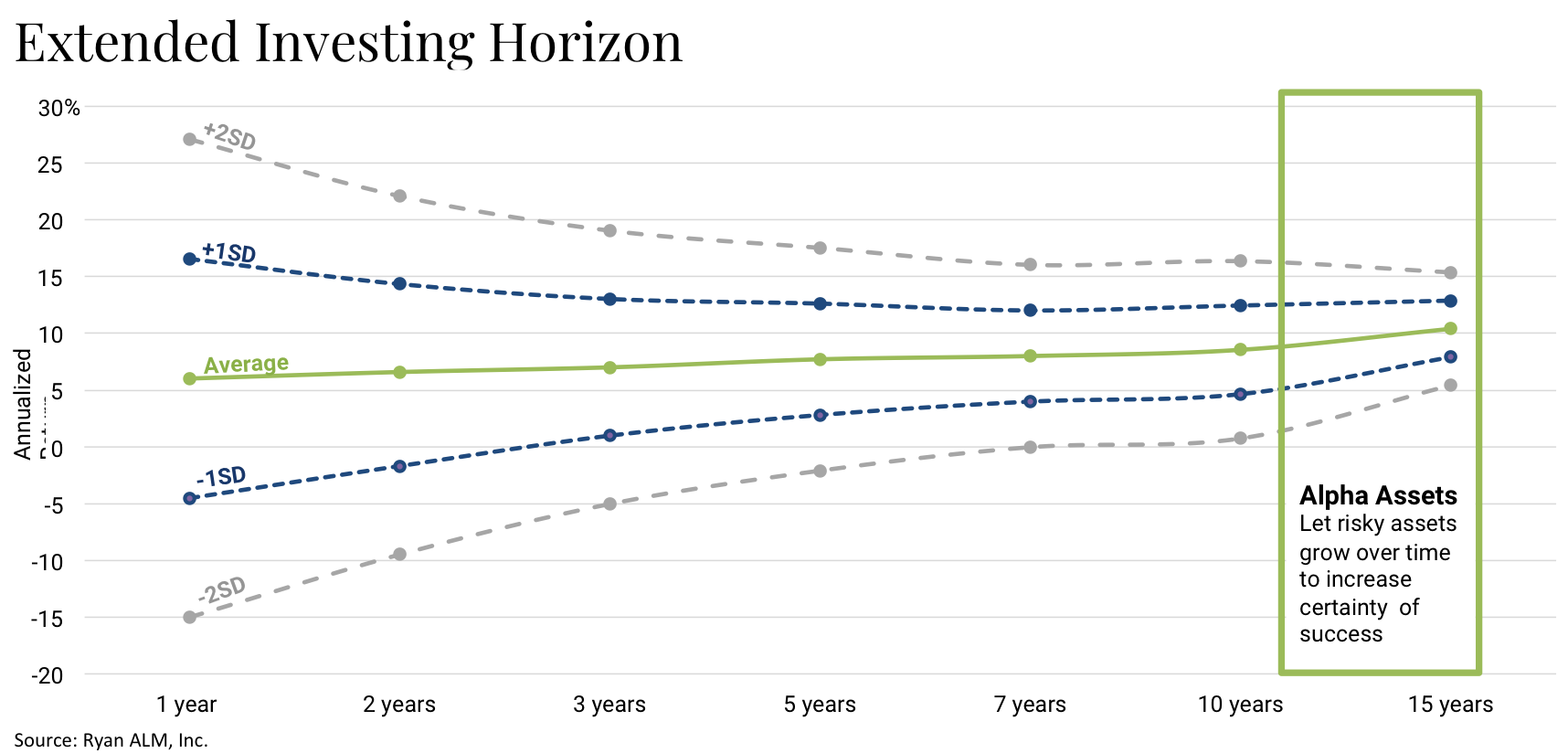

As the chart above reflects, a traditional asset allocation with a one-year investment horizon has a tremendous amount of volatility associated with it. By providing the portfolio with a 10-year investment horizon, the standard deviation declines dramatically increasing the probability of achieving one’s return objective. Furthermore, by defeasing the plan’s near-term liabilities, liquidity to meet benefit payments and expenses is enhanced allowing the alpha assets to grow unencumbered. Importantly this change in asset allocation converts fixed income from a performance-seeking investment to a cash-flow-producing investment, which is the true value in bonds, especially in this current environment.

But the proof is in the pudding. A recent analysis that we did for a struggling public pension plan showed that with the injection of a POB and the adoption of this implementation we could dramatically improve the Funded Ratio, freeze contributions at the current level (saving the plan >$10 billion in future contributions), reduce funding costs by >20%, and cover the debt-service while determining that the fund could accomplish all of this with a ROA that was 80 bps lower than their current objective. You may be thinking that this just seems too good to be true, but we would be glad to take you through both our process and this analysis. Call us, especially if you are affiliated with the GFOA.