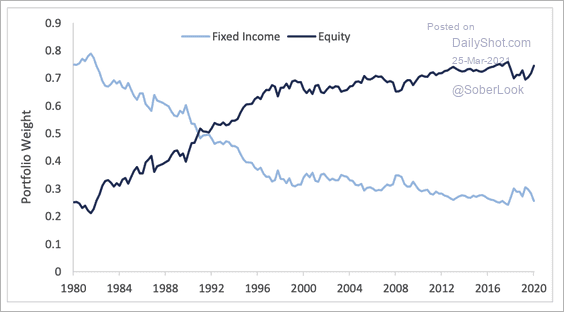

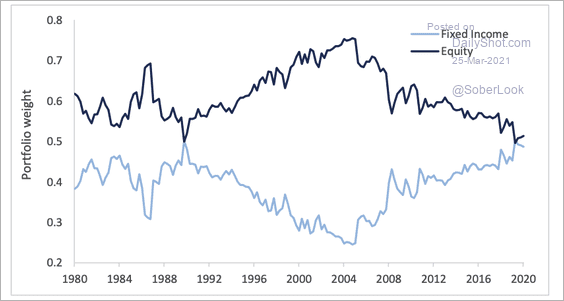

We know that the accounting rules differ quite significantly in the treatment of discount rates for public (GASB) and private pension plans (FASB). Do the differences manifest in asset allocation? According to the following two charts, the answer is yes, and it is quite significant!

Chart 1 (thanks, Deutsche Bank) highlights the change in exposure to fixed income within public pension plans during the last 4 decades. While the second chart reflects the allocation to fixed income by private pensions. After a brief reduction to fixed income during the go go ’90s, private pension plans ramped up their exposure to fixed income and today sit at roughly a 50%/50% mix. But are these differences just the result of the accounting rules? We’d say, no!

Regrettably, private pension plans have been hell-bent on eliminating DB pensions ever since the advent of defined contribution plans (DC) and 1986 Tax Reform. This has driven plans to reduce risk, as they establish glide paths toward full funding and the possible transfer of pension liabilities to insurance companies. But every private plan has certainly not frozen, terminated, and/or transferred their pension liabilities. For those that haven’t, the market valuation pension rules under FASB have created an environment in which the average private pension plan is much better funded than the average public pension system.

With regard to public pension systems, there is the perception that these entities are perpetual. But is that perception reality? We’ve seen examples of DB plans being frozen and new employees being thrust into DC or hybrid offerings. I wrote a blog post several years ago in which I stated that perpetual doesn’t mean sustainable. I fear that we could be entering a time when we could see more examples of public pension systems seeking alternatives to traditional DB plans. A trend that will certainly not be favorable to future public employees. It is likely that burgeoning contributions will make some of these systems unsustainable. We’ve witnessed tremendous growth in contribution expenses throughout pension America since the 2000-2002 recession. This growth is becoming a significant burden for some to handle, as it takes a bigger slice each year from the social safety net. Some pension systems have made the full contribution, while others have not, further pressuring an already tenuous situation.

Given the perception that public pension systems are perpetual, they have embraced the idea that they can become much more aggressive in the allocation of assets to equity and equity-like products. But is that decision sound? The volatility that comes with a much more aggressive allocation has subjected these plans to massive swings as we’ve had to endure three significant market corrections in just the last 20 years. Given the 70+% return in the markets during the last 12-months, is there really that much more to gain before we finally see a pause or correction?

At Ryan ALM, we think that asset allocation should be driven by the plan’s funded status and not the accounting rules. Public pension systems can have a higher exposure to alpha assets (non-bonds), but they need to ensure that near-term liabilities are secured before ramping up the risk. With a greater focus on near-term liabilities through a cash-flow matching strategy, the pension fund has now bought time for the alpha assets to grow unencumbered. Furthermore, they are no longer a source of liquidity removing the possibility of being forced to sell assets at inappropriate times. We are huge supporters of DB plans, but there needs to be a change in how they are managed, or we may see their demise far sooner than expected.