There are multiple examples throughout time when the price of an “investible” item has gotten tremendously out of whack from the underlying fundamentals. There are examples of prices rising well beyond what the underlying story would justify and examples of when prices have collapsed in anticipation of a changing fundamental landscape. We likely have a couple of such stories developing today – perhaps Bitcoin and some of our technology stocks on the upside and many value stocks that have been pummeled representing attractive opportunities to explore on the downside.

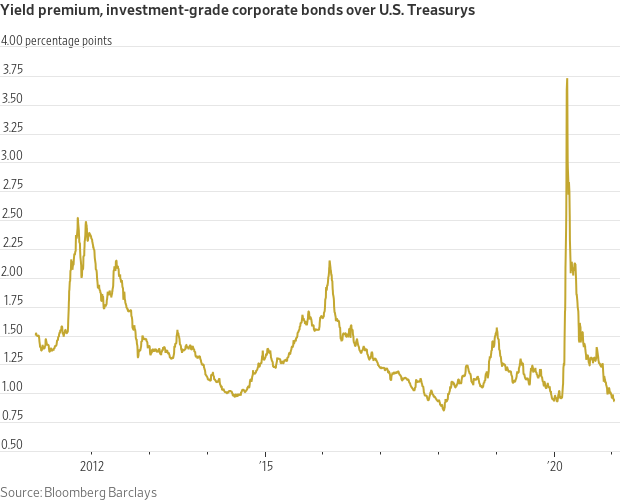

One opportunity that presented itself early in 2020 reversed course so quickly that one would have to have been in the positions already and hung on or an investor would have to have been so agile to move quickly to take advantage of the opportunity. For most U.S. pension systems that dynamic capability just doesn’t exist. As the chart below indicates, yield spreads for U.S. corporate bonds blew out versus comparable maturity U.S. Treasuries in March of 2020. The sell-off in those bonds and the subsequent widening of yield spreads occurred nearly overnight. However, the rally and tightening of yield spreads has been nearly as rapid.

Investment grade corporate yields currently sit at just under 100 bps of spread versus Treasuries. This is about as tight as they’ve been in the past decade or so. However, that yield advantage still provides a very nice cushion should a rare default occur. In addition, that premium yield compounds each year of any bond’s existence. As you may recall, Ryan ALM uses corporate bonds almost exclusively in implementing our cash flow matched portfolios of assets versus pension liabilities. We were recently retained by a corporate plan to provide a cash flow matching portfolio for a vertical slice of the plan’s liabilities (about 12% of projected liabilities over 80 years). Because of our yield advantage we were able to create an incredible 30%+ funding cost savings on the future value of the plan’s liabilities.

The U.S. investment-grade corporate bond market has changed dramatically over the years. Long gone are the days of multiple AAA rated securities. Today we have nearly 70% of new issuance being BBB, and that has led to an investment-grade universe with more than 50% in BBBs at this time. Fortunately, defaults remain rare, but that doesn’t mean that strong credit research isn’t imperative – it absolutely is. Given that bond yields in general are near historic lows, bonds should not be viewed as performance generating instruments in this environment. They should be used for the cash flow that they generate through coupon, reinvestment of the coupon, and maturity. Now’s the time to adjust your asset allocation to reflect this reality and use cash flow matching with investment grade bonds as the liquidity core portfolio. Call us – we’ll help you think through an appropriate strategy.