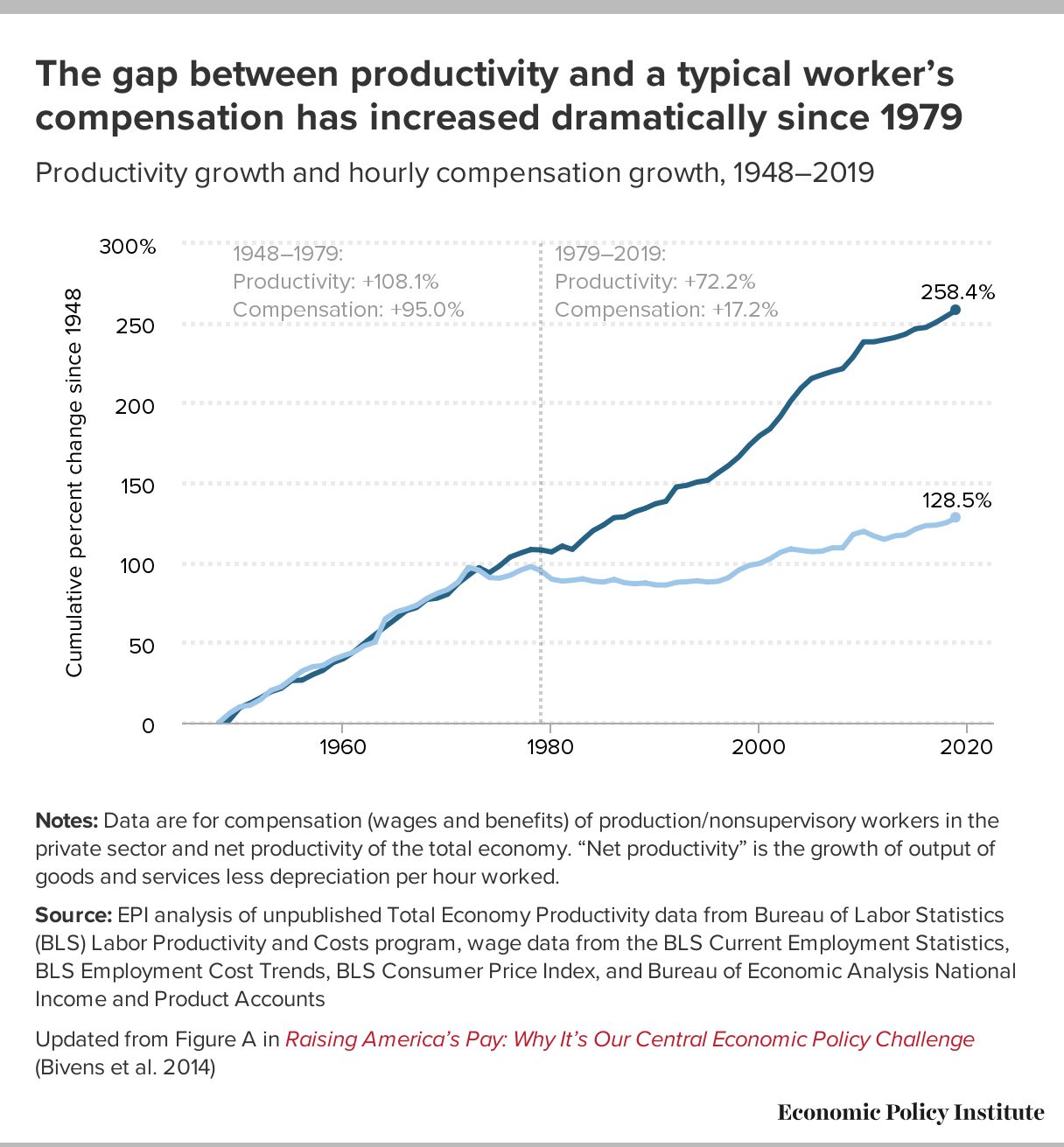

At roughly the same time that traditional DB plans were starting to fade from use in the private sector and workers were being asked to primarily fund their own retirements through a DC option, wage growth diverged unexpectedly and significantly from productivity growth.

The lack of wage growth not only coincided with the loss of a pension for many Americans, but it also came at the same time of rapidly rising costs for housing, education, healthcare, etc. Should we really be surprised that Americans are falling behind in saving for retirement? I’ve often stated that there is a basic level of income needed for the average American to live. Regrettably, for many Americans their current wage falls far below that basic level.

The folks at MIT have created a “Living Wage” calculator that helps to determine the necessary minimum wage based on local cost of living expenses. For instance, a single mother with two children living in Newark, NJ needs to earn $42.33/hour to meet her basic living expenses. Unfortunately, the minimum wage currently in NJ is $11.10/hour or roughly 1/4 of what she actually needs. If you are living in Mobile, AL, that single mother of two children requires an hourly compensation of $28.42 or roughly 2/3s what is needed in Newark. Regrettably, the minimum wage in Mobile is $7.25: again, roughly 1/4 of what is needed.

For our Newark resident who works 40 hours per week and 52 weeks per year, the annual compensation that she would need in order to meet her basic living expenses would be $88,046. As of 2018, the median family income in Newark, NJ was a shockingly low $37,642, or roughly 42.8% of what that family of three needs. Is there any wonder why she may not be funding her 401(k), if she even has access to one? It drives me crazy when I read about various generations being excessive consumers. You know, the latte, avocado toast people who would rather consume than spend wisely by investing in their future. I find it hard to believe that mom and her kids are spending much money, if any, on lattes.

We absolutely need to address the ever growing wage disparity that weighs heavily on a significant portion of our population. In a previous blog post I highlighted output from a study that found that the lowest quartile of workers by wages had seen a >30% loss of jobs during the Covid-19 crisis. These individuals have very little in financial resources to weather any loss of a job/wages, let alone continue to fund a retirement benefit. It is critically important to our workers and to our economy that we preserve DB plans for the masses so that older members of our society can remain active participants in our economy demanding goods and services. DC plans should continue to be supplemental to true retirement funds, as they were initially considered. Anything short of this will result in failure.