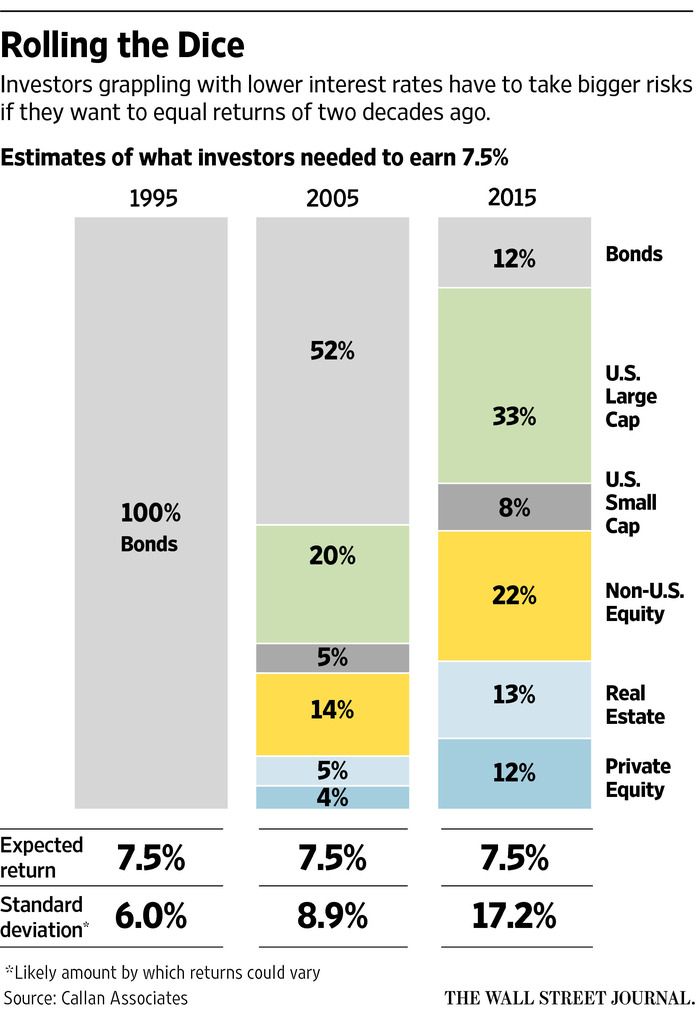

On Tuesday I shared with you my thoughts related to the difficult job facing asset consultants in this market environment. Today I share with you a wonderful chart prepared by Callan Associates and extracted from the WSJ (thanks, Chris) that highlights exactly what I was describing.

As recently as 1995, a pension plan could invest 100% in U.S. Bonds and generate a return that was commensurate with the plan’s return on asset objective, and they could get that return with a very modest 6% standard deviation. In 2005, pension systems could still put significant assets to work within Bonds (52%), but had to diversify into other asset classes in order to achieve the same 7.5% projected return. Although the standard deviation increased, it did so marginally.

By 2015, we had an incredible situation in which a 7.5% forecast return comes with a standard deviation of 17.2%. What does that mean? Well, it means that 68% of the time the return that a plan can expect to receive will be between 7.5% +/- 17.2% or -10.7% to +24.7%. Worse, a plan should expect 95% of the time to have that performance fall between -27.9% and +41.9%. Wow, you could drive a dozen semis through that gap! Furthermore, the fund’s new asset allocation has introduced the plan to greater complexity and transparency issues. Do you think that 2020’s asset allocation needs will be any better than 2015’s? No way! Interest rates continue to decline to historic levels, while equity valuations are stretched creating a challenging combination, and alternative investments are not a panacea either.

As we’ve mentioned many times, one way to reduce the annual standard deviation associated with today’s markets is to cash flow match near-term liabilities through the matching of benefit payments and expenses with the cash flow from a Liability Beta Portfolio (bonds). Adopting this strategy will significantly increase the investing horizon for the non-cash flow matched assets and dramatically reduce the variability that one should expect given a 10-year view, as opposed to managing one year at a time. Furthermore, the bonds that remain in the portfolio will be used solely for their cash flow and NOT as a performance generator, especially difficult given the low rates.

Given what has happened to state and municipal budgets, additional contributions are not on the table as a way to make up for underperformance relative to the 7.2% average ROA for public plans. Worse, they certainly can’t afford to have another 2 standard deviation event that has their total fund down >20%. Think that isn’t likely? Just remember 2001, 2008, Q1 2020, etc. Let’s talk!