It isn’t rocket science to understand why defined contribution plans are inferior to defined benefit plans for the simple reason that most American workers do not have the discretionary income to fund one’s retirement account, if they even have access to one. In a well-publicized report, the National Institute on Retirement Security (NIRS) has estimated that 59% of working-age Americans has not saved a single penny for retirement and regrettably they also don’t have access to a DB plan.

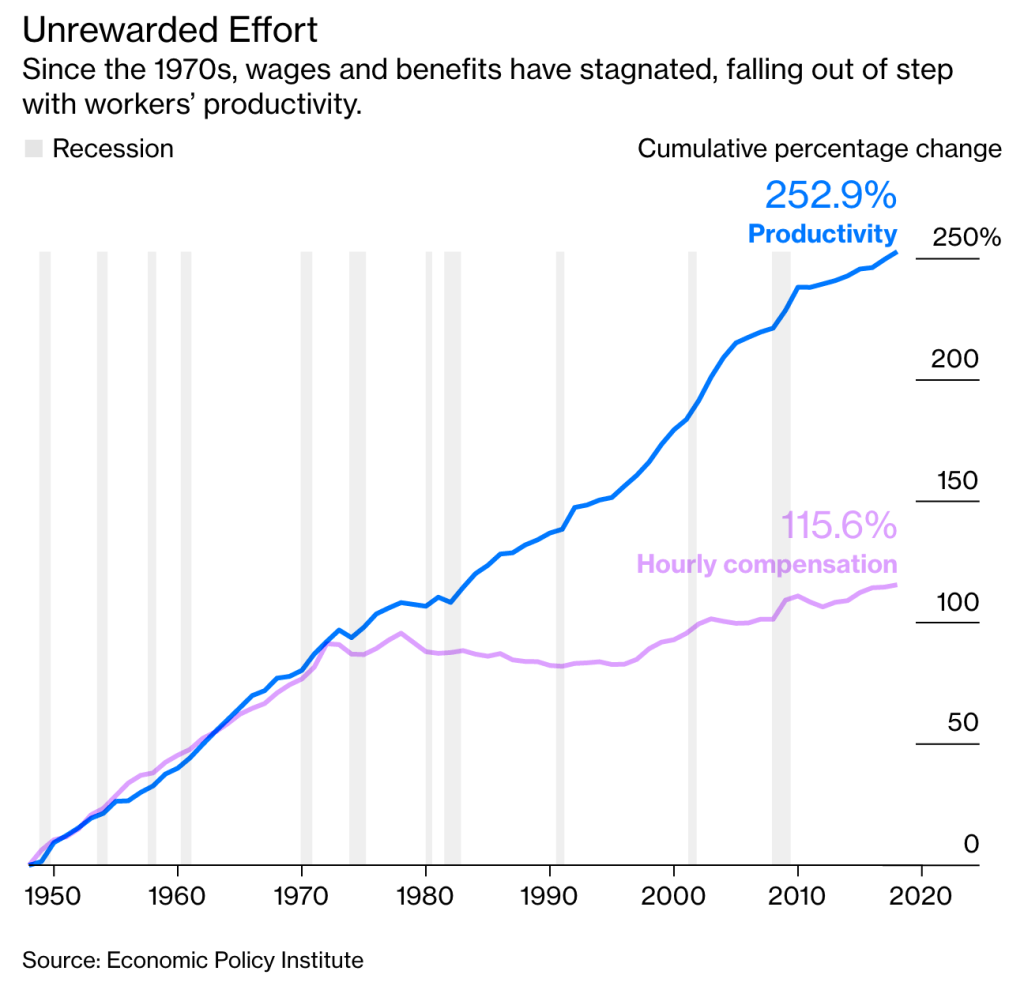

In another recent article published on Bloomberg’s site, “How The American Worker Got Fleeced”, it was highlighted how wage growth has been stagnant, traditional benefits cut, and workers’ rights revoked during the last several decades. As the graph below reflects, there once existed a fairly steady relationship between wages and productivity, but that relationship suffered a nasty divorce in the early 1970s. As a result, most Americans are being dramatically underpaid for the output that they are producing.

It should also be noted that these lower wages have been compounded by the impact of greater inflation for many household expenditures, including housing, healthcare, and education. In addition, the federal minimum wage, stuck at $7.25 since 2009, is worth roughly 70% of what it was in 1968, and about a third of what it would be had it kept pace with productivity. In fact, the bottom 90% of wage earners (those making <$120,000) has seen only a very modest increase in their incomes during last two decades. For workers receiving the minimum wage, they are making less today than in 1998, when inflation adjusted.

Couple these trends with the fact that benefits for healthcare and retirement have been scaled back and you have a formula for financial disaster, which is exactly what is transpiring today. The loss of union membership has left the private sector without a voice in salary and benefit negotiations. The movement to more of an on-call labor force has also compounded these trends. These sub-contracted workers allow companies to significantly reduce the liabilities that normally come with a full-time employee.

I’ve just ordered the book Supreme Inequality, which is a look at the US Supreme Court decisions of the last 50-years that has created a more unjust America for the American worker. I’ll have to report back on Adam Cohen’s work in a future blog post. In the meantime, we need to do everything we can to protect and preserve DB plans for the masses, as the above mentioned trends are doing everything to reduce the likelihood that today’s American worker will ever retire, let alone retire with dignity. I find this development to be shameful.