The most significant cause of the current pension crisis is the failure to contribute enough to these plans! As a result, too much emphasis has been placed on generating out-sized returns, which have failed to materialize. Oh, we’ve had brief moments of glory (decade of the ’90s), but far too often we’ve had these riskier portfolios subjected to significant market corrections (’00-’02, ’07-’09, Q4’18, 2/20-3/20). When will we finally choose another course?

Federal Reserve policy decisions that have lead to rapidly falling US rates have proven incredibly harmful to Pension America and savers in general. But, instead of ponying up more cash in the form of contributions, we tried to game the system by juicing up possible returns. We got the volatility, but not returns! The chart below tells an amazing story.

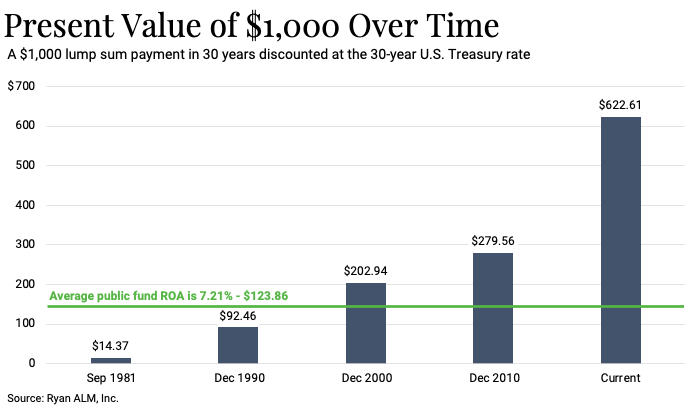

The chart above highlights the cost to secure a $1,000 benefit payment 30-years out, and at various points in time throughout my career. The green line is representative of the average ROA for the 50 US states. When we discuss the impact that the Federal Reserve policy decisions have had on Pension America, this is exactly to which we are referring.

In 1981, when I first entered this industry, you could secure a $1,000 pension benefit payment 30-years out with just $14.37. Incredible! The US 30-year Treasury bond yield was 14.8% at that time. The power of compounding (is it the eighth “wonder of the world”?) provided you with an amazing opportunity that we are likely never to see again in the US. Given this environment, one has to wonder why Pension America didn’t immunize and defease every pension system and secure the victory for decades to come?

Interestingly, pension systems that had an “average” ROA (they were higher in the early ’80s than what we are depicting) were paying more into the system than they needed to in 1981, as the discounting mechanism for liabilities was lower than the prevailing 30-year yield. In our example, plan sponsors were contributing $109.49 more than they needed to if they actually achieved the projected ROA. They continued to contribute more into their systems through the early 1990s, but as interest rates began to plummet, those contributions fell further and further behind.

In fact, today we have a situation in which that same $1,000 would cost you $622.61 in present value $s. Regrettably, because pension systems are using an inflated discounting mechanism of 7.21% (the ROA), they are under contributing to these systems by about 5X. Instead of funding that $1,000 at $623, they are only putting into their systems $123.86. Again, this forces pension systems to try to spike returns, and as a result, we get this constant roller-coaster effect to ruin. Remember what Hurricane Sandy did to the NJ shore communities.

Enough is enough. As we discussed in our most recent blog, most state and municipal pension systems are not going to invest their way to improved funding, as the hole that has been dug is just too deep. Plan sponsors need to find additional resources to enhance contributions. Without addressing the need for greater contributions plan assets will continue to be whipsawed by market action, and the sustainability of these systems will once again be called into question.