Most of us have read numerous articles discussing the “excessive” cost of maintaining a state or municipal pension system, and there are certainly examples of states that are seeing a fairly significant percentage of their annual budgets going to support these entities, such as KY, NJ, and IL to name just a few. However, the majority of states and municipalities are just fine! Sure, funded status will have taken a hit and contribution expenses are likely to rise as a result of Covid-19’s economic toll, but for a significant majority of public pension systems, the hit won’t dramatically alter their ability to meet pension obligations well into the future.

Importantly, these funds are engines to economic growth. Recent studies, as reported by the National Association of State Retirement Administrators (NASRA) highlight the fact that in 2018, state and local government retirement systems in the U.S. distributed $173 billion more in benefits than they received in taxpayer-funded contributions. Incredibly, there is more income produced from these retirement systems than that which is received from the nation’s farming, fishing, logging, and hotel/lodging industries combined!

Another study by the National Institute on Retirement Security (NIRS) found that “retiree spending of pension benefits in 2016 generated $1.2 trillion in total economic output, supporting some 7.5 million jobs across the U.S. Pension spending also added a total of $202.6 billion to government coffers, as taxes were paid at federal, state and local levels on retirees’ pension benefits and their spending in 2016.”

Of greatest importance to me is the fact that these systems are professionally managed lessening the responsibility of individuals to fund, manage, and then disburse a retirement benefit. As we know, a majority of Americans don’t have the discretionary income to fund a plan, nor the expertise to manage one, and lastly a crystal ball to know how to adequately disburse their principal. That’s a lot for even the pros to handle.

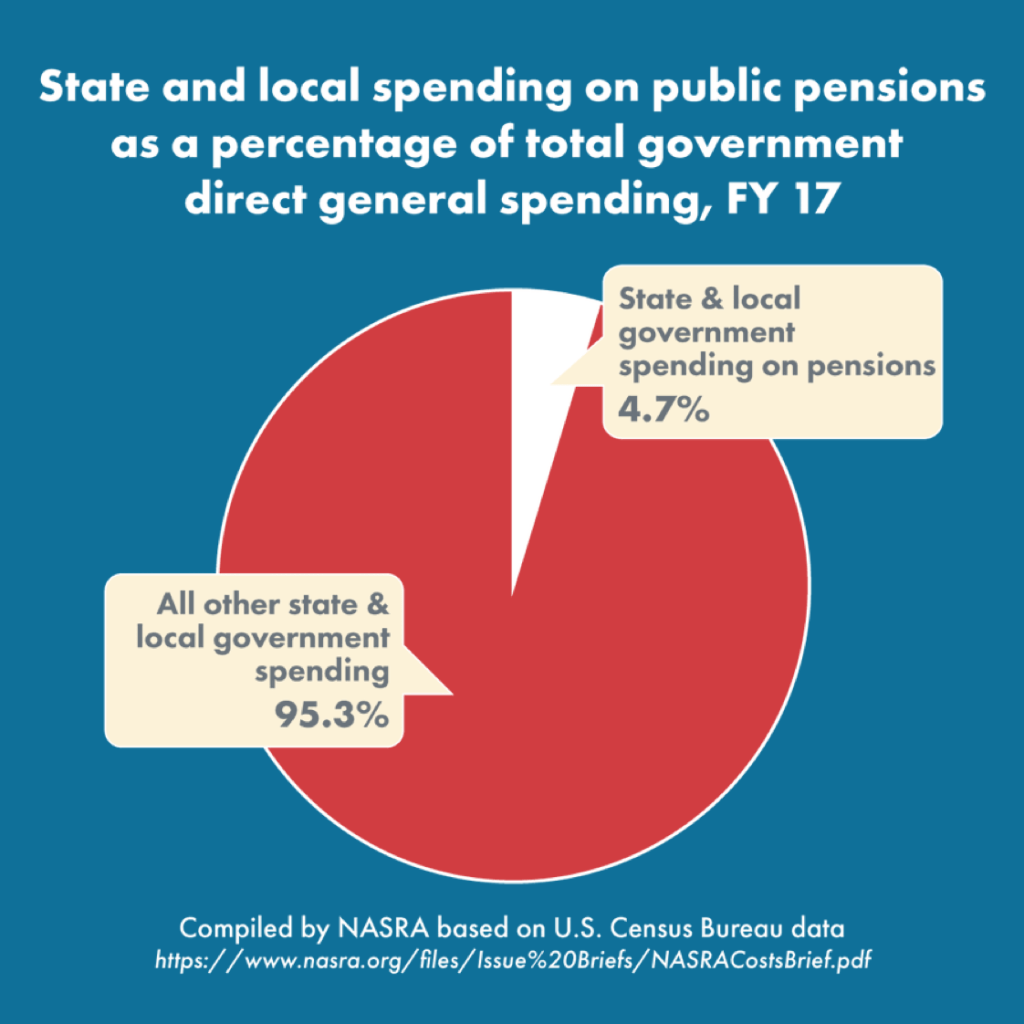

My support for defined benefit plans doesn’t mean that there aren’t issues that need to be addressed, such as making sure that an appropriate ROA is used and required annual contributions paid in full. But, DB pensions, with their monthly annuity payout are superior to the glorified savings accounts that are 401(k)s, 403(b)s, etc. Next time you read about how much of the social safety net is being chewed up by state and local pension systems, please refer to the chart above. It tells a much different story.