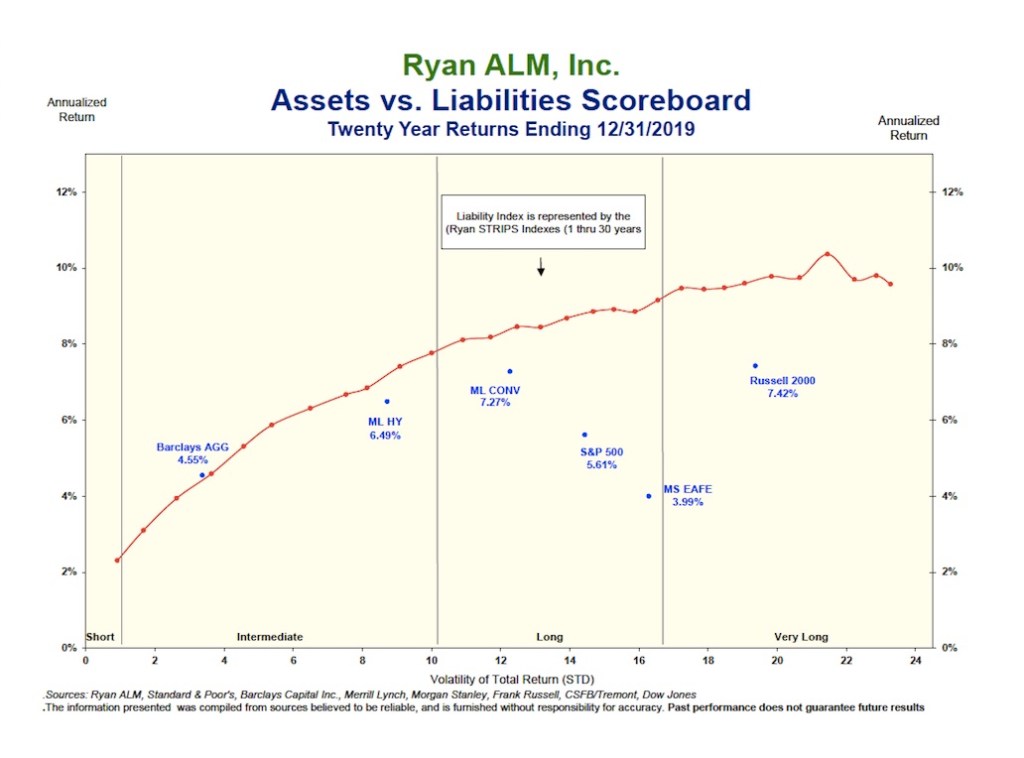

Everyone knows that first quarter performance results were ugly. It will not come as any surprise then that funded status and contribution expenses were significantly negatively impacted. But, even before Covid-19 struck, assets were struggling to keep up with the growth in pension liabilities, as the chart above reflects (data through December 31, 2019).

Different accounting rules (IASB, FASB, GASB) permit different discount rates to be used to measure pension liabilities, but the only TRUE measure of pension liabilities is a risk-free rate. The liability index above (red line) uses the Ryan ALM STRIPS index (maturities 1-30 years). The performance of the STRIPS index for the 20-years ending 12/31/19 dwarfs the risk-adjusted returns for many of the major indexes that would represent exposure to the assets in most pension systems.

I mention this because most non-corporate plans continue to focus nearly exclusively on the return on asset (ROA) assumption, and as a result, fail to include liabilities in the analysis when it comes to determining an appropriate asset allocation and investment structure. Clearly, paying heed to plan liabilities would NOT have negatively impacted America’s pensions during the 20-years ending December 19. Furthermore, understanding and managing to pension liabilities would absolutely not have hurt during the first quarter of 2020.

When will out industry wake up to the fact that you can’t manage a pension plan without understanding the promise that you made to the plan’s participants? Can you imagine playing a football game and not knowing what the score was as you entered the fourth quarter? In that case, you wouldn’t know what offense or defense to run. It is the same thing in managing a pension system. The only way to know the “score” is to measure, monitor, and manage to the plan’s liabilities.